What is a balloon payment? The complete guide (definition, calculation and your options)

A balloon payment is a large lump sum due at the end of a loan term, following smaller regular instalments that do not fully repay the principal. Balloon payments appear most commonly in PCP car finance agreements and certain mortgage structures. Borrowers can pay, return, refinance, or sell, with distinct cost and credit implications. Failing to plan risks default; act three to six months ahead.

What is a balloon payment?

A balloon payment is a loan feature that defers part of the total cost to one final lump sum. Regular monthly payments cover interest or depreciation only, not the full purchase price. The balloon payment meaning is consistent across PCP car finance, mortgage structures, and business asset loans: a large final payment you must address when the term ends.

Balloon payment meaning in simple terms

In a Personal Contract Purchase (PCP) car finance deal, monthly payments cover only the car's predicted depreciation over the contract. The car's residual value stays unpaid throughout the agreement term. Negative equity becomes a concern only if the car loses value faster than predicted. In plain terms, a PCP balloon payment is the unpaid residual value you face at term end.

How does a balloon payment work?

Balloon payment finance agreements follow five stages:

- The creditor and debtor agree a balloon payment amount at loan start.

- The debtor makes regular payments covering interest or depreciation.

- The debt balance remains largely intact throughout the term.

- The balloon payment falls due as a lump sum on the final date.

- The debtor pays, refinances, sells, or returns the asset.

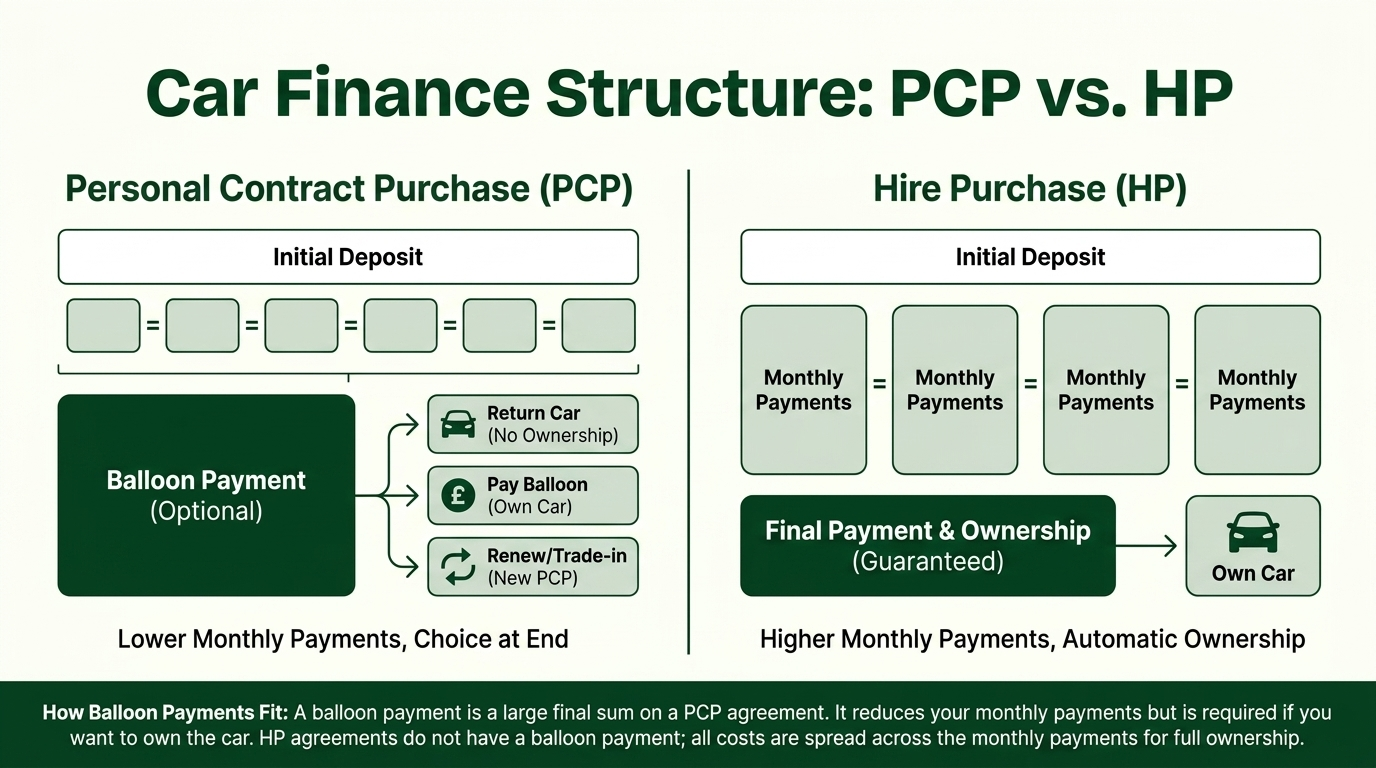

Car finance balloon payment explained in contrast: a Hire Purchase (HP) agreement amortises the entire purchase price across monthly payments with no balloon. Balloon payment car finance keeps costs lower month to month but leaves a larger obligation at term end.

"A common misconception is that monthly PCP payments are gradually buying the car — they aren't. They're covering the depreciation only. The car's residual value sits untouched as the balloon throughout the agreement. That's the structural point most borrowers miss, and it's exactly why the final sum comes as a shock when it shouldn't."

Roman Danaev, Car Finance Expert

How is a balloon payment calculated?

The lender sets the balloon payment based on the asset's projected residual value. For you, the result is: purchase price minus deposit (down payment) minus total monthly payments equals the balloon. A larger down payment reduces the financed amount; lenders set the balloon using depreciation models that estimate the asset's future value. PCP and mortgage contexts apply the formula differently; Finance & Leasing Association (FLA) data shows motor finance providers supported almost 2.1 million consumer car purchases in 2025, with PCP the largest share.

Balloon payment calculation in car finance (PCP)

PCP lenders set the balloon payment using the Guaranteed Minimum Future Value (GMFV). The GMFV determines what a balloon payment on a car will be at contract end. Four factors shape the GMFV:

- Car make and model

- Contract length (typically two to four years)

- Expected annual mileage

- Projected condition at return

A worked PCP balloon payment calculator example:

The interest rate applies to both the financed portion and the balloon. Rates start from 9.9% APR. Interest accrues on the outstanding balance, which includes the GMFV portion, throughout the term. A lower rate reduces both the monthly instalment and the total amount payable.

Representative example: cash price £25,000, deposit £5,000, amount of credit £20,000, 36 monthly payments of £520, optional final payment (GMFV) £12,000, total amount payable £35,720, Representative 23.9% APR. Your rate depends on credit profile, income, and chosen lender. You can model scenarios using the car finance calculator. The representative example assumes the balloon is paid in full at term end.

Car finance with balloon payment structures means the lender absorbs the residual risk if the car's market value drops below the GMFV. Negative equity does not affect you when returning under PCP terms, because the GMFV guarantee protects you.

Balloon payment calculation in mortgages

A mortgage balloon payment follows a different structure from PCP. A balloon mortgage compresses a long-term loan into a shorter payment window, typically five to seven years. The balloon payment equals the remaining principal when the shorter term ends.

A fixed-rate mortgage may hold a constant interest rate without fully amortising the loan. Repossession is the consequence of default on a mortgage balloon. Before 2008, many borrowers assumed refinance options would always be available to discharge the balloon payment.

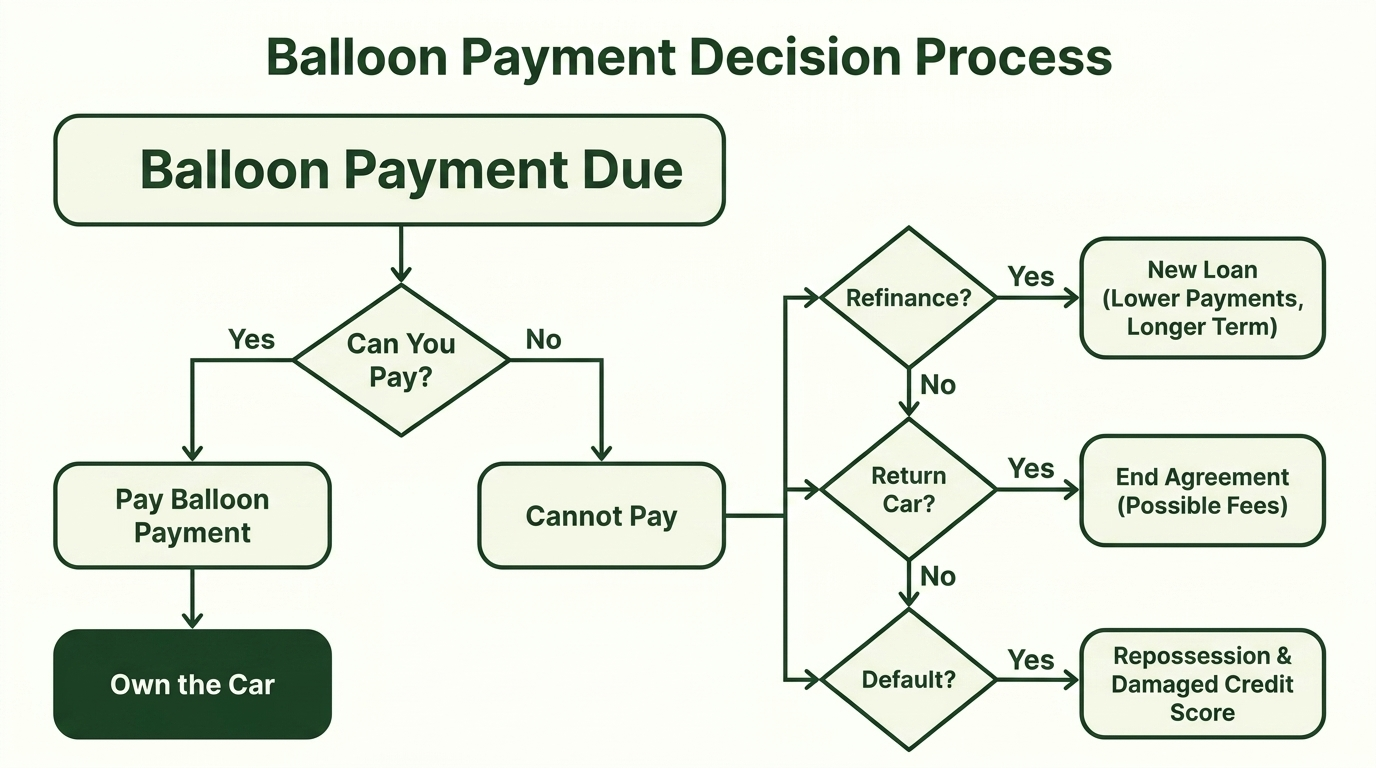

What are your options when a balloon payment is due?

Check your eligibility - no impact on your credit score

Leave a request and our experts will contact you shortly to discuss the details.

End-of-term is a planned decision point. When a PCP balloon payment falls due on your car, four paths exist:

- Pay in full. Ownership of the balloon payment car transfers immediately. Best suited when the car is worth more than the balloon amount.

- Return the car. Under Personal Contract Purchase terms, hand the car back if mileage and condition meet limits. If the car depreciated below the GMFV, the lender absorbs the negative equity shortfall, not you.

- Refinance the balloon. A new loan (personal loan, HP agreement, or specialist refinance product) replaces the balloon with monthly payments. Your credit score determines the rate and eligibility.

- Sell or part-exchange. If the car's market value exceeds the balloon, surplus becomes equity toward the next vehicle.

Default is the consequence of inaction. Not acting before the car finance agreement ends damages your credit score and can trigger repossession. Start exploring well before the final month.

| Option | How it works | Pros | Cons | Credit impact |

|---|---|---|---|---|

| Pay in full | Clear the balloon as a lump sum; ownership transfers immediately | Full ownership, no further payments | Requires large cash outlay | Positive: loan closed |

| Return the car | Hand car back under PCP terms; lender absorbs any negative equity shortfall | No further obligation if mileage and condition terms met | No car and no equity retained | Neutral: agreement fulfilled |

| Refinance | A new loan (personal loan, HP, or specialist product) replaces the balloon with monthly payments | Keeps the car without a lump sum | Interest adds to total cost; requires qualifying credit score | Depends on new terms |

| Sell or part-exchange | Sell the car privately or through a dealer; proceeds clear the balloon | Potential equity surplus toward next vehicle | Market value may fall short of balloon amount | Positive: loan settled |

"Returning the vehicle is the option I see applicants overlook most often, and it's frequently the most financially rational one. If the car has depreciated faster than the GMFV predicted, returning it transfers that shortfall risk back to the lender — not the borrower. That protection is built into the PCP agreement; it simply needs to be used."

Roman Danaev, Car Finance Expert

Can you refinance a balloon payment?

"The critical mistake I see is borrowers waiting until the final month to explore refinancing. By that point, options are limited and negotiating leverage is gone. Starting the process three to six months before the term ends means the credit assessment happens on current circumstances — with enough time to address issues before the balloon falls due."

Roman Danaev, Car Finance Expert

Yes, you can refinance a balloon payment. Refinancing replaces the balloon with a new loan (personal loan, HP agreement, or specialist refinance product) structured as monthly payments. The interest rate on the refinanced agreement depends on your credit score at application, not the rate from the original deal. Lenders assess current income, existing debt, and payment history before approving a balloon payment refinance. Acting several months before maturity preserves negotiating room. Waiting until the last month narrows options and increases default risk.

How to refinance a PCP balloon payment

Refinancing a PCP balloon payment follows seven steps:

- Check the balloon amount in your Personal Contract Purchase agreement three to six months before term end.

- Check your credit score using a free tool such as Experian or ClearScore.

- Obtain the car's current market value and compare to the GMFV.

- Approach the existing car finance lender first to request refinance balloon payment options.

- Compare offers from other lenders: personal loans, HP agreements, specialist refinance products.

- Calculate total interest rate costs using a refinance balloon payment calculator. A lower monthly payment over a longer loan term may cost more in total.

- Confirm the new agreement before the PCP term lapses.

Refinancing a balloon payment on a car with bad credit

Refinancing a balloon payment with a poor credit score is possible but more expensive. Sub-prime car finance lenders charge a weighted average interest rate of 33% APR (FCA, 2025). Some set rates as high as 46% APR.

Lenders generally prefer to refinance a balloon payment rather than pursue repossession. Repossession is costly for the finance company. That preference gives borrowers room to negotiate, even with a damaged credit score.

High-APR specialist lenders can accelerate default rather than prevent it. Before accepting any refinance offer above 40% APR, seek free guidance from Citizens Advice or StepChange.

Advantages and disadvantages of balloon payments

Balloon payment car finance suits some borrowers and creates risk for others. The balloon payment options table above details each end-of-term path. The deferred loan structure improves monthly cash flow during the term but creates risk at maturity, as the comparison below shows.

| Factor | Advantage | Disadvantage |

|---|---|---|

| Monthly payments | Lower than a standard loan (you finance depreciation only) | Large lump sum remains at term end |

| Flexibility | Pay, return, or refinance at term end | Refinancing requires a good credit score at application |

| Negative equity | GMFV protects if car value drops below the balloon | Keeping the car may cost more than market value |

| Credit impact | On-time payments build credit history | Default leads to repossession and lasting credit damage |

Balloon payment vs. other finance options

The right car finance product depends on your goal. Personal Contract Purchase balloon payment finance offers lower monthly payments but includes a balloon. Hire Purchase (HP) costs more per month but transfers ownership automatically.

A lease (Personal Contract Hire) avoids balloon and ownership entirely. PCP's lower payments often mask higher total cost when interest on the balloon is included. Credit eligibility varies by product. See the infographic below.

Can I get car finance without a balloon payment?

Yes. Car finance without a balloon payment is available through three routes:

- Hire Purchase (HP) spreads the full loan across instalments with ownership at the end. HP car finance costs more monthly than PCP but less overall.

- Personal Contract Hire (PCH) is a lease with no balloon payment.

- Personal loan. A bank loan covers the full car price. Your credit score determines eligibility.

HP is the most direct balloon-free car finance option for buyers who want ownership.

Most popular questions

We've collected the most popular questions about car loans from our customers

What is a balloon payment on a car loan?

A balloon payment on a car loan is a lump sum due at the end of a PCP agreement. The lender sets the amount at contract start based on the car's GMFV. Paying the balloon transfers ownership. Returning the car or refinancing into new monthly payments are alternatives.

How is a balloon payment calculated?

Lenders calculate the balloon payment by estimating the car's residual value at term end. The formula: purchase price minus deposit minus total monthly payments. Factors include car make, mileage allowance, contract length, and expected condition. The balloon figure is fixed from the first day of the agreement.

Can a balloon payment be refinanced?

Yes. A new loan replaces the balloon payment with monthly instalments. Credit score and income determine eligibility at the time of application. Start exploring options several months before the PCP term ends. Compare offers from multiple lenders to refinance a balloon payment at the lowest total cost.

What happens if a balloon payment cannot be met?

Failing to pay a balloon payment by the due date risks default. Default damages your credit score and may lead to vehicle repossession. Contact your lender before the deadline to discuss refinancing. You can also return the car under PCP terms. Free advice is available from Citizens Advice and StepChange.

Is balloon payment finance a good idea?

Balloon payment finance suits borrowers wanting lower monthly payments who plan to return or change cars every two to four years. Less suitable if you want to own the car outright and cannot pay the lump sum. Consider HP if predictable payments with guaranteed ownership is the priority.

Check your eligibility — no impact on your credit score

Leave a request and our experts will contact you shortly to discuss the details.

Author

Roman Danaev is a UK car finance specialist with over a decade in the motor finance industry. He has helped thousands of customers find the right finance deal — from standard HP and PCP agreements to bad credit and no-guarantor options. Roman writes practical, jargon-free guides to help UK drivers make informed borrowing decisions.