How to improve your credit score: 15 proven steps that actually work (UK guide)

You can raise your UK credit score with four high-impact actions. Check your credit report for errors. Register on the electoral roll. Keep your credit utilisation below 30%. Pay every bill on time. Three credit reference agencies calculate your score: Experian, Equifax, and TransUnion. Each agency holds slightly different data, so no single universal score exists in the UK.

Quick wins can lift your score within 30 to 60 days. Correcting an error or joining the electoral roll works fast. Rebuilding after a default or County Court Judgment takes longer. These marks stay on your file for six years. This guide sets out 15 steps, ordered by speed of impact. Each claim below links to an official UK source you can check.

What is a credit score and why does it matter?

A credit score is a number that predicts how likely you are to repay borrowing. Your score decides whether a lender approves you. It also shapes the interest rate and credit limit you receive. A higher score means lower risk, so you gain wider choice and cheaper rates. The UK has no single score. Experian, Equifax, and TransUnion each calculate their own version from lender data.

Each agency uses a different scale, so one person sees three numbers. Experian began rolling out a new 0 to 1250 scale in late 2025, completing the transition by January 2026. It replaced the old 0 to 999 range. Equifax scores run from 0 to 1000. TransUnion runs from 0 to 710. Your score band matters more than the exact figure. Lenders map your band to their own lending criteria.

Your credit score sits on top of your credit report. The credit report is the detailed file each agency holds on your borrowing. A strong credit card or loan history pushes your score up. Missed payments pull it down. The table below shows the current bands each agency publishes.

| Agency | Scale | "Good" band | "Excellent" band |

|---|---|---|---|

| Experian | 0 to 1250 | 861 to 1000 | 1121 to 1250 |

| Equifax | 0 to 1000 | 531 to 670 | 811 to 1000 |

| TransUnion | 0 to 710 | 604 to 627 | 628 to 710 |

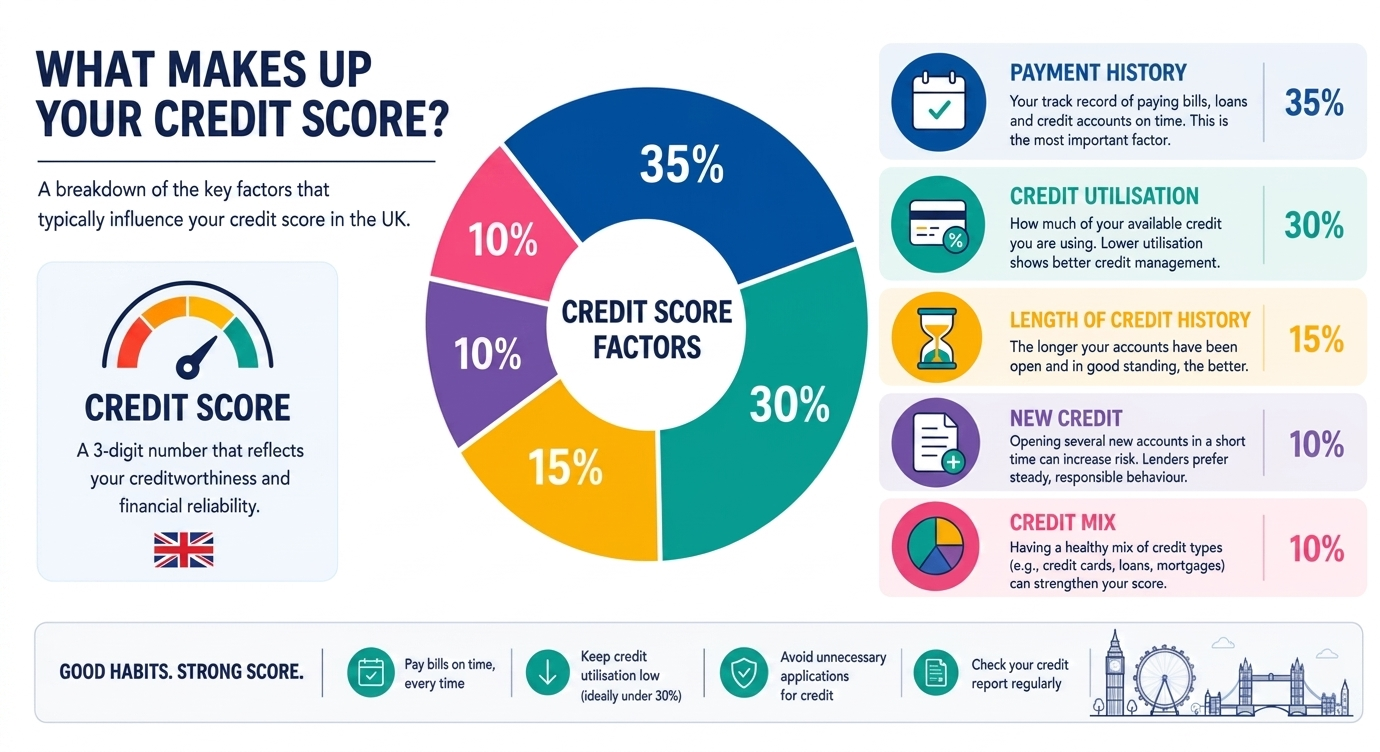

How credit scores are calculated and what affects your credit score

Lenders calculate your score from three inputs: your credit report, your application form, and records they already hold. Payment history carries the most weight, because it shows whether you repay on time. Credit utilisation is the share of your limit you use. It is the second most influential factor.

The percentages below come from the US FICO model. They illustrate relative importance. UK agencies use their own undisclosed formulas, but the ranking holds.

| Factor | Illustrative weight (FICO model) | What it measures |

|---|---|---|

| Payment history | 35% | On-time versus missed payments |

| Credit utilisation | 30% | Balance used against your limit |

| Length of credit history | 15% | Average age of your accounts |

| New credit | 10% | Recent applications and hard searches |

| Credit mix | 10% | Variety of credit types held |

What credit reference agencies in the UK actually track, and what they don't

Credit reference agencies record your accounts, payment history, electoral roll status, defaults, and County Court Judgments. They do not hold your salary, savings balance, or criminal record. Many readers feel relieved that their bank balance stays invisible to lenders. Your credit report does carry serious negative marks, so accuracy matters.

The credit report includes:

- Credit accounts such as loans, credit cards, and mobile contracts, with payment records

- Electoral roll registration confirming your name and address

- Defaults, which stay on file for six years from the default date

- County Court Judgments, which also remain for six years

Credit scoring predicts future behaviour, not past punishment

A credit score predicts how you will manage credit next. It is not a moral verdict on your past. People with little history are often called credit invisibles. They score poorly because lenders have no data to assess. A thin credit file creates the same barrier as a damaged one. Building positive evidence on your credit report raises your score. Overseas credit history does not transfer to a UK file. New arrivals start from zero here.

Lenders also want profitable customers, not just safe ones

Lenders weigh profit alongside risk when they assess your score. Card issuers often favour "revolvers," who carry a balance and pay interest. They earn less from "transactors," who clear the balance each month. The interest rate is where the issuer profits. A flawless payer is not always their ideal customer. Never carry debt deliberately to please a lender. Interest costs outweigh any scoring benefit.

Your credit report sets the rate you get, not just approval

Your credit report decides whether you are approved and at what rate. Two applicants for the same card can receive different rates. The lender prices each applicant for risk. The representative APR is the rate at least 51% of accepted applicants receive. Your personal rate may be higher. This rate-for-risk principle applies to mortgages and personal loans too.

Why is my credit score low? Common causes explained

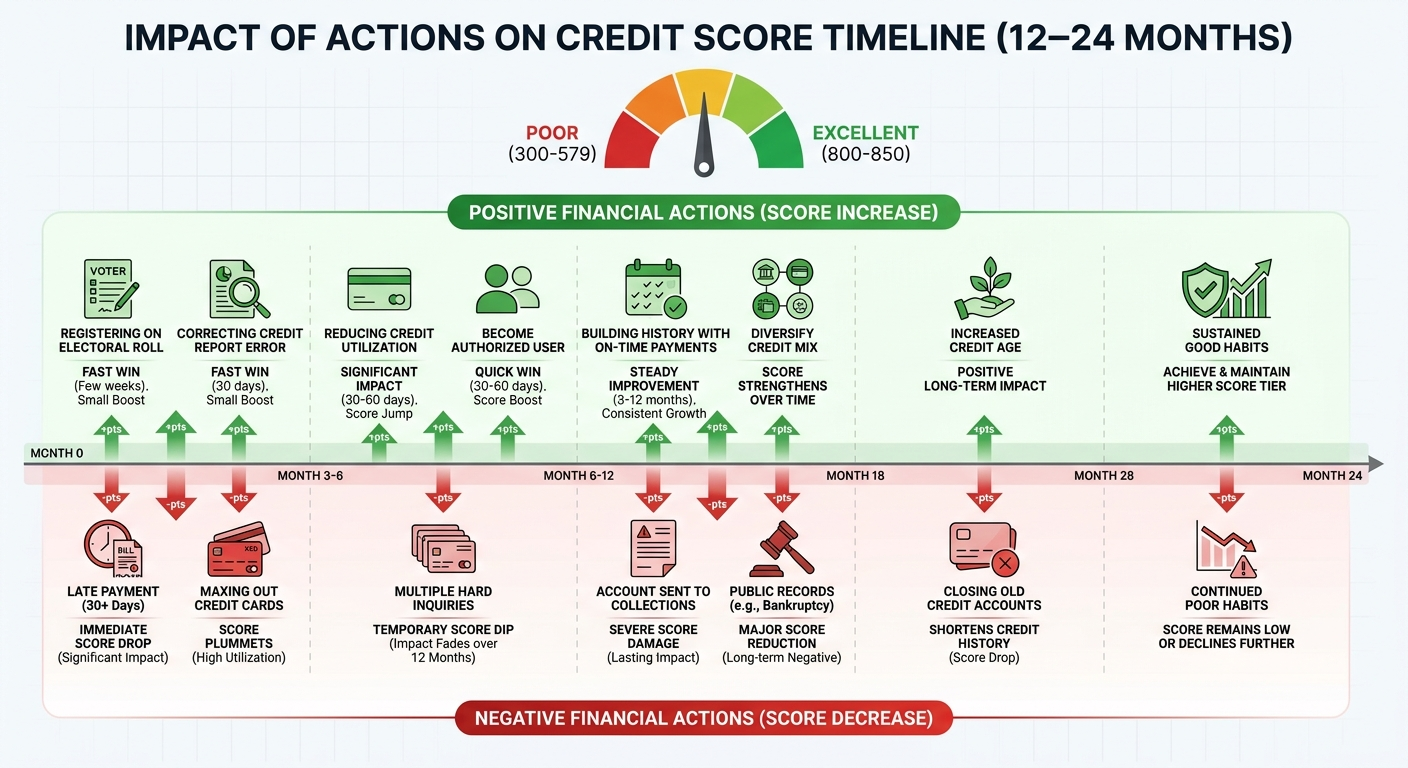

Your credit score is usually low for one of four reasons. Missed payments, high credit utilisation, a default, or a County Court Judgment all pull it down. Missed and late payments are the most common cause. A default or CCJ does serious damage, yet both fade over their six-year life. High credit utilisation is the most fixable cause, because you can reduce a balance this month. A thin file can score as poorly as a negative one.

What affects your credit score the most, ranked by impact

The most damaging marks follow a clear order of severity. Recent marks weigh more than older ones. Most drop off after six years.

- Bankruptcy and County Court Judgments cause the most severe damage

- Defaults registered by a lender follow close behind

- Missed or late payments lower payment history

- High credit utilisation signals reliance on credit

- A thin credit history gives lenders too little to assess

A CCJ paid in full within one month is removed from the register. Pay later, and it stays for six years marked as "satisfied."

Don't panic if your credit score drops, fluctuations are normal

Small credit score movements are normal and rarely signal trouble. Your score shifts with billing-cycle timing and balance reporting dates. Focus on your credit report, not the number on any single day. Checking your own report is a soft search, so it never lowers your score. That common fear is a myth worth dismissing.

How to improve your credit score: 15 proven steps

These 15 expert steps are ordered by speed of impact. They run from immediate wins to longer-term strategy.

Step 1: check your credit report for errors immediately

Checking your credit report across all three agencies is the fastest potential win. Errors drag your score down. A wrong address, a settled debt shown as owed, or an unknown account all count. You can view each report free, and checking it is a soft search. Correcting one error can lift a score quickly.

Step 2: register on the electoral roll

Registering on the electoral roll is one of the simplest high-impact steps. Electoral roll data lets lenders confirm your identity and address. Register free at GOV.UK, and the update usually appears within weeks. The open or full register makes no difference to your score.

Step 3: keep your credit utilisation below 30%

Credit utilisation is the share of your credit limit you use. It is one of the highest-impact factors you control. Keep utilisation below 30%, and ideally around 25%. On a £3,000 limit, that means holding the balance under £900. Lower the ratio by repaying, or by requesting a higher limit without spending more. Pay before the statement close date, because that balance is what gets reported.

Step 4: pay on time, every time

On-time payment is the foundation of a strong credit history. It is the most heavily weighted factor in your score. A single missed payment damages payment history. A run of on-time payments rebuilds it. Set up a Direct Debit for at least the minimum payment. If you have already missed one, pay it now and ask for a goodwill amendment. This is a long-term habit, not an overnight fix.

Step 5: reduce outstanding debt using savings where possible

Reducing debt with savings improves your utilisation and cuts interest costs. For example, savings earning around 4% rarely beat credit card debt at around 24% APR. Clearing the balance usually wins financially. Lower balances reduce utilisation, which lifts your score. Keep a small emergency fund before you empty your savings.

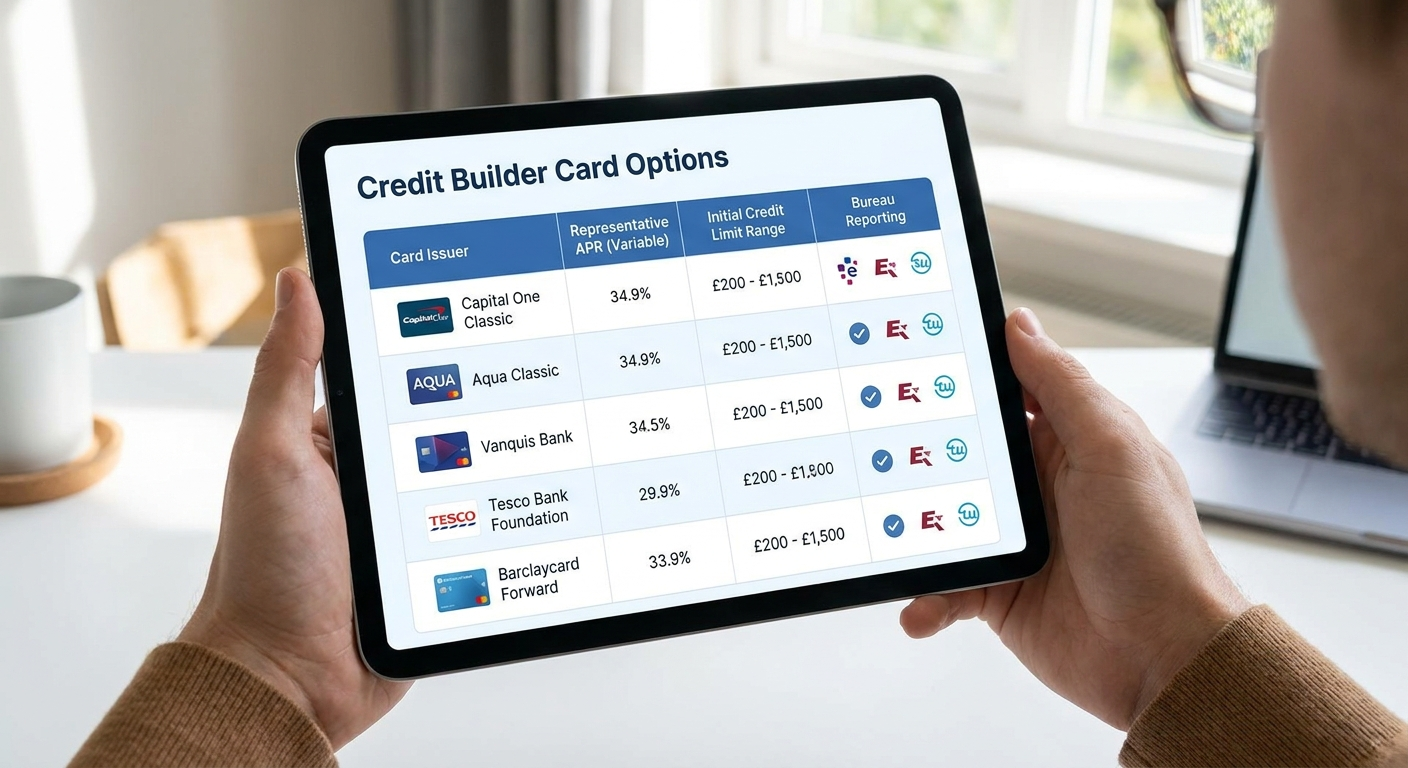

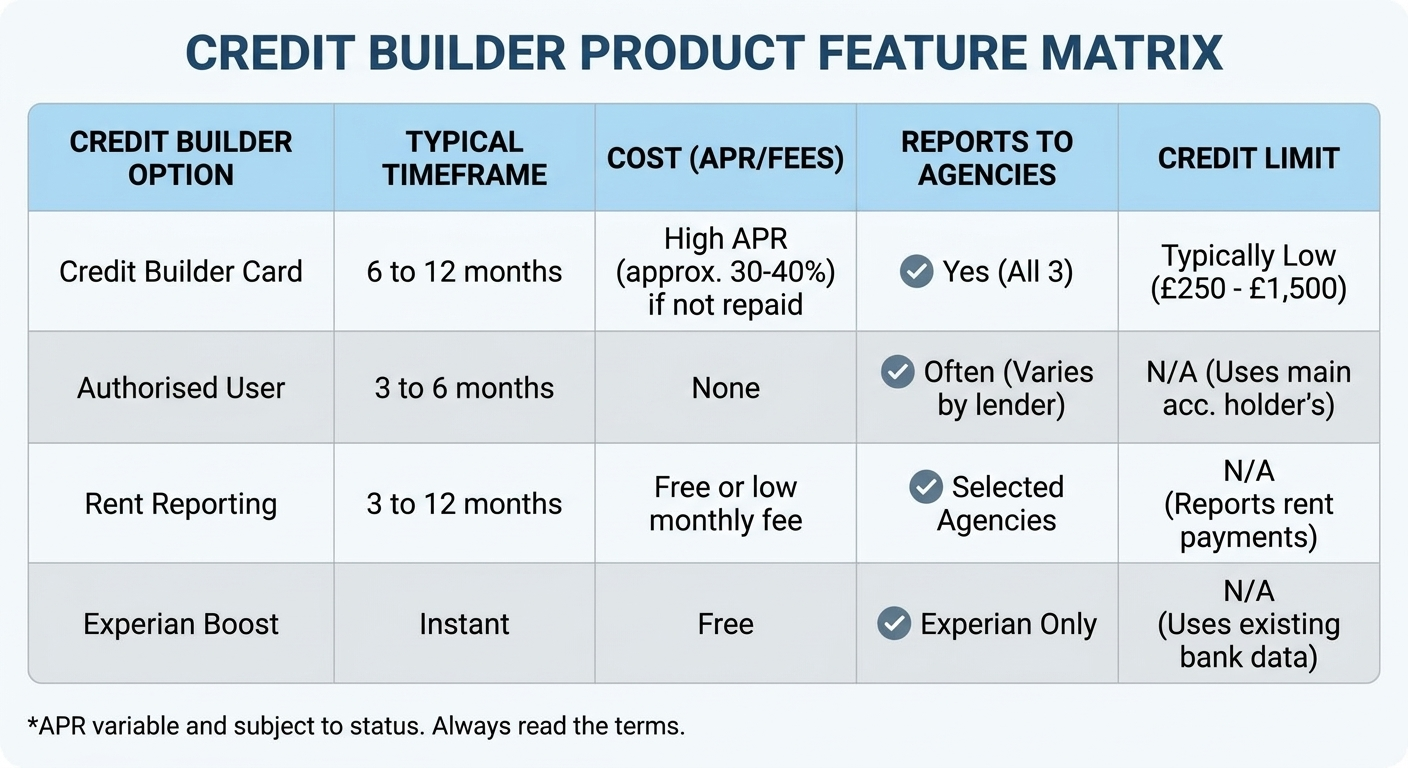

Step 6: use a credit builder card strategically

A credit builder card is a card designed to build or repair a thin credit history. Used correctly, it reports responsible behaviour to the credit reference agencies. It grows your record over 6 to 12 months. The formula is simple: one small recurring purchase, repaid in full by Direct Debit, with no cash withdrawals. Credit builder cards typically carry high representative APRs, often around 30% to 40% as of 2026. Repaying in full each month is therefore essential. The table compares the main credit-building methods.

Step 7: become an authorised user on someone else's account

Becoming an authorised user on a trusted person's card can pass positive history to your file. The account holder needs a clean credit history. Their record influences how the account reads. Mismanagement by either party can damage both scores, so trust matters. This differs from a joint account, which creates a formal financial association.

Step 8: report rent payments to credit agencies

Rent reporting turns your largest monthly payment into a positive entry. Services such as Credit Ladder, Canopy, and Wollit report rent to credit reference agencies. Experian now includes rental data in its score. Late rent could be reported negatively, so pay on time. Not every lender weighs rent data equally, but the upside is free.

Step 9: minimise hard credit searches by using eligibility checkers

A hard search is recorded on your credit report and visible to lenders. A soft search stays invisible to them. Several hard searches in a short window signal risk and can lower your score. Eligibility checkers use soft searches, so you can test your odds first. Paying insurance monthly by instalments can trigger a hard search, which surprises many applicants.

| Search type | Visible to lenders | Affects score |

|---|---|---|

| Soft search | No | No |

| Hard search | Yes | Yes, temporarily |

Step 10: manage financial associations carefully

A financial association forms when you share a joint product. A joint mortgage, loan, or bank account all create one. The associated person's credit report can affect your application, even after a relationship ends. A former partner's CCJ has caused strong applicants to be declined for a mortgage. File a Notice of Disassociation once the link has genuinely ended.

Step 11: think carefully before closing old credit accounts

Closing an old credit card can lower your score. Closure cuts your available credit and shortens your history. Less available credit raises your utilisation ratio. Losing an old account reduces the average age of your history. Cutting up a card is not the same as closing the account. Leaving a dormant card open often helps more, though weigh any annual fee.

Step 12: avoid cash withdrawals on credit cards

A cash withdrawal on a credit card charges interest immediately, with no grace period. The transaction appears on your credit report. It can read as poor cash flow to lenders. Use a debit card for cash instead. The exception is essential overseas travel, where a specialist card may be safer.

Step 13: time your credit applications strategically

Timing a major application around recent negative marks improves your odds and your rate. A default or CCJ drops off after six years. Waiting for it to age off before a mortgage can change the outcome. If a CCJ clears in three months, delay a mortgage application by three months. Avoid applying during a life change such as maternity leave, when income looks unstable.

Step 14: use Experian Boost and rent-reporting tools

Experian Boost is a free Open Banking tool. It reports regular payments like Netflix, council tax, and savings to your Experian score. It can raise your Experian score instantly. It only affects Experian, and not every lender adopts it. Experian is one of three FCA-regulated UK credit reference agencies. Boost uses Open Banking without storing your bank login. It pairs well with the rent-reporting tools in Step 8.

Step 15: dispute unfair defaults and fight for corrections

You have a legal right to dispute an inaccurate default or CCJ. The dispute process is straightforward when you follow it in order:

- Gather evidence such as statements, letters, and payment proof

- Contact the credit reference agency and the original lender at the same time

- Escalate to the Financial Ombudsman Service if the lender rejects a valid claim

- Add a Notice of Correction of up to 200 words if the dispute stays unresolved

Your right to accurate data is protected under UK data protection law. When you settle a default, ask the lender to mark it "satisfied." A satisfied default reads better to future lenders.

Stability counts, use consistent details and avoid overchurning

Consistent personal details protect you from fraud-scoring declines. Different address formats, employer names, or phone numbers can trigger fraud systems such as National Hunter. These can cause an automatic decline. Treat each application like a CV, with the same details every time. Overchurning, or rapid back-to-back applications, reads as desperation and lowers your score.

Be careful with buy now, pay later (BNPL)

Some buy now, pay later providers already report payments to credit reference agencies. The FCA regulates BNPL from 15 July 2026, after which BNPL agreements are treated as regulated credit. Missed BNPL payments can damage your score where providers report to agencies. Treat BNPL exactly like a credit card and pay on time.

Payday loans: why they can harm your credit even when repaid on time

A payday loan can mark you as financially stressed to certain lenders, even when repaid on time. Some mortgage lenders decline or downgrade applicants who used payday loans recently. If you need finance without turning to payday lenders, bad credit car finance offers a structured alternative. It builds your credit file through regular repayments, without the mortgage-application penalty.

Check your eligibility - no impact on your credit score

Leave a request and our experts will contact you shortly to discuss the details.

How long does it take to improve your credit score?

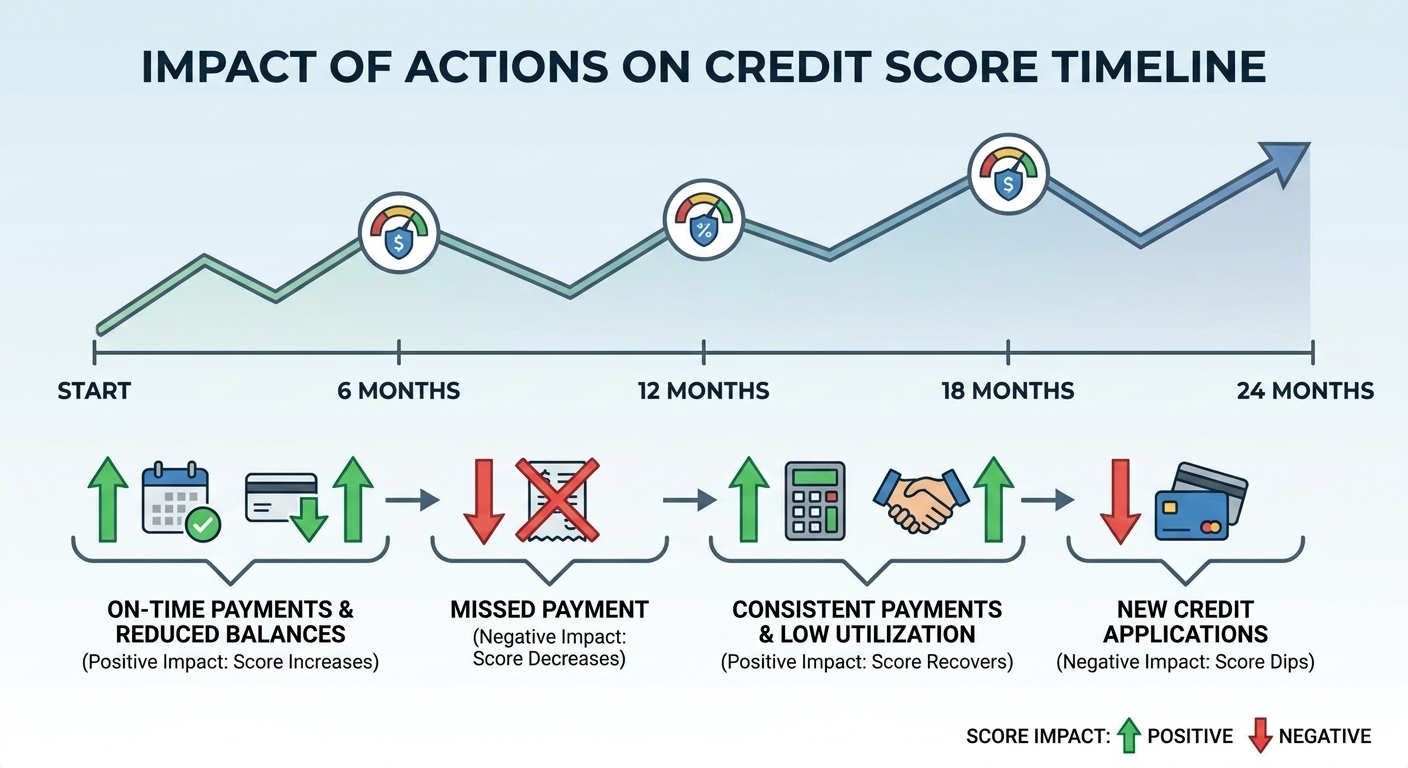

Improving your credit score takes from 30 days to several years. Your starting point sets the pace. Fast wins like electoral roll registration and error correction show within 30 to 60 days. Lower credit utilisation works in the same window. Building credit history through on-time payments takes 3 to 12 months. Recovering from a default or CCJ takes the longest, because both stay on file for six years. Their impact fades each year. Recent positive behaviour outweighs older negative history. Credit improvement is not a single moment, it is a direction.

What a fair credit score means and when to seek help

A fair credit score sits in the middle band of each agency. With Experian, that is 641 to 860. At a fair or poor score you can still access products. You often pay higher rates and get lower limits. Some specialist brokers set no minimum credit score and assess on affordability instead. Some specialist platforms, including Car-Finance.co.uk, set no minimum credit score threshold. They assess applications on affordability rather than score band alone. You can also explore car finance with fair credit or car finance with a CCJ. When a low score reflects genuine hardship, free help is the right next step.

When to seek professional debt advice, and where to find it

Seek free debt advice if you cannot meet minimum payments. The same applies if you borrow to repay other borrowing, or face debt collection contact. Three free debt advice charities offer impartial help:

- StepChange provides free debt management plans and budgeting support

- Citizens Advice offers free, confidential debt guidance across the UK

- National Debtline gives free telephone and online debt advice

Avoid paid "credit repair" companies. They cannot do anything you cannot do yourself for free. The Financial Conduct Authority regulates the firms that genuinely matter.

Frequently asked questions

We've collected the most popular questions about car loans from our customers

What is the best strategy to increase my credit score?

Pay every bill on time and keep credit utilisation below 30%. Payment history and utilisation are the two strongest factors. Add electoral roll registration and regular credit report checks for steady, lasting improvement.

How long does it take to improve your credit score?

Quick wins like error correction and lower utilisation show in 30 to 60 days. Building credit history takes 3 to 12 months. Recovering from a default or CCJ can take up to six years, as agencies update data monthly.

Why is a good credit score important?

A good credit score widens access to credit cards, loans, and mortgages, and secures lower rates. With Car-Finance.co.uk, the Representative APR is 23.9% and rates start from 9.9% APR. A higher score can move your personal rate toward the lower end.

What are the most common reasons for a credit score to drop suddenly?

A missed payment, a utilisation spike, a new hard search, or a fresh default can all cause a sudden drop. A missed payment is the most common trigger. Check your credit report to find the exact cause.

How do credit scores work?

Credit reference agencies calculate scores from your credit report to predict repayment behaviour. Experian, Equifax, and TransUnion use different scales and formulas, so your three scores differ. Lenders combine your score with their own criteria to decide.

Important information

Car-Finance.co.uk is a trading name of Moneyrepublic Ltd (Company No. 12141408). Moneyrepublic Ltd (FRN: 967024) is an Appointed Representative of F&I Online Ltd (FCA No. 731217), which is authorised and regulated by the Financial Conduct Authority. Car-Finance.co.uk acts as a credit broker, not a lender, and may receive a commission. Representative 23.9% APR. Rates from 9.9% APR.

Representative example: borrowing £7,500 over 48 months at 23.9% APR representative gives a monthly repayment of approximately £234.77 and a total amount payable of approximately £11,269. Finance is subject to status and affordability. Checking your eligibility uses a soft credit search and does not affect your credit score. A full credit check is carried out by the lender if your application proceeds.

Check your eligibility — no impact on your credit score

Leave a request and our experts will contact you shortly to discuss the details.

Author

Roman Danaev is a UK car finance specialist with over a decade in the motor finance industry. He has helped thousands of customers find the right finance deal — from standard HP and PCP agreements to bad credit and no-guarantor options. Roman writes practical, jargon-free guides to help UK drivers make informed borrowing decisions.