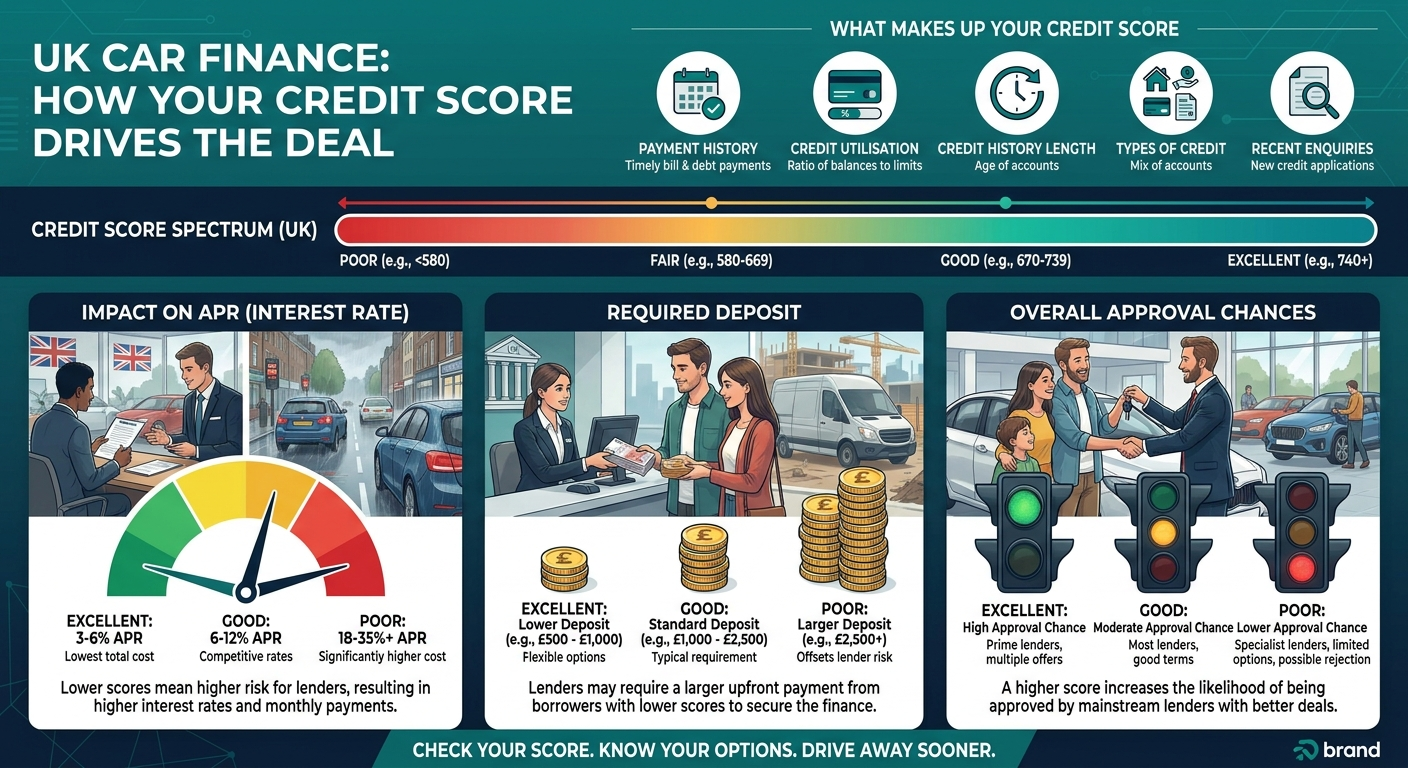

What credit score do I need for car finance?

Experian, Equifax, and TransUnion each use a different numerical scale, so no single target number applies across all UK lenders. Each bureau assigns a rating band, and the band — not the raw number — determines what terms a lender offers. Most credit ratings can access car finance in some form. A lower credit score produces a higher interest rate, expressed as APR, which materially increases the total cost over the full agreement term.

Why there is no single "magic number" for car finance

No universal credit score threshold exists for car finance in the UK. A credit score is a numerical rating produced by a credit bureau from an individual's credit history, and lenders use it to assess borrowing risk.

Three credit reference agencies operate in the UK: Experian, Equifax, and TransUnion. Each bureau maintains independent records on different numerical scales, so the same applicant typically holds three different scores simultaneously.

How Experian, Equifax, and TransUnion score applicants differently

Experian scores UK consumers on a scale of 0 to 999. Equifax applies a range of 0 to 700. TransUnion uses a scale of 0 to 710, accessible free through Credit Karma UK.

ClearScore provides free Equifax data. Not all lenders report payment data to all three bureaus, so a default visible on one file may not appear on another.

| Rating | Experian (0–999) | Equifax (0–700) | TransUnion (0–710) | Typical car finance outcome |

|---|---|---|---|---|

| Excellent | 881–999 | 466–700 | 628–710 | Best available APRs; no deposit usually required |

| Good | 721–880 | 420–465 | 604–627 | Competitive rates; deposit may improve terms |

| Fair | 561–720 | 380–419 | 566–603 | Finance available; APR above market average |

| Poor | 281–560 | 280–379 | 551–565 | Specialist lenders required; higher APR expected |

| Very Poor | 0–280 | 0–279 | 0–550 | Subprime lenders only; deposit strongly recommended |

Does it matter which bureau a car finance lender uses?

The bureau a lender queries determines which version of the applicant's credit history informs the decision. Mainstream UK car finance providers most commonly query Experian or Equifax. Specialist and subprime lenders may query TransUnion or use proprietary risk models.

The same applicant can present materially different credit profiles depending on which bureau is used. Reviewing all three reports before applying gives a complete picture of what each lender may see.

"Most applicants check their score on one platform and assume that's what every lender will see — but it isn't. If your Experian file carries a satisfied default that hasn't reached your Equifax record yet, the lender querying Equifax will see a meaningfully different picture. That single variable can be the difference between an approval and a decline."

Roman Danaev, Car Finance Expert

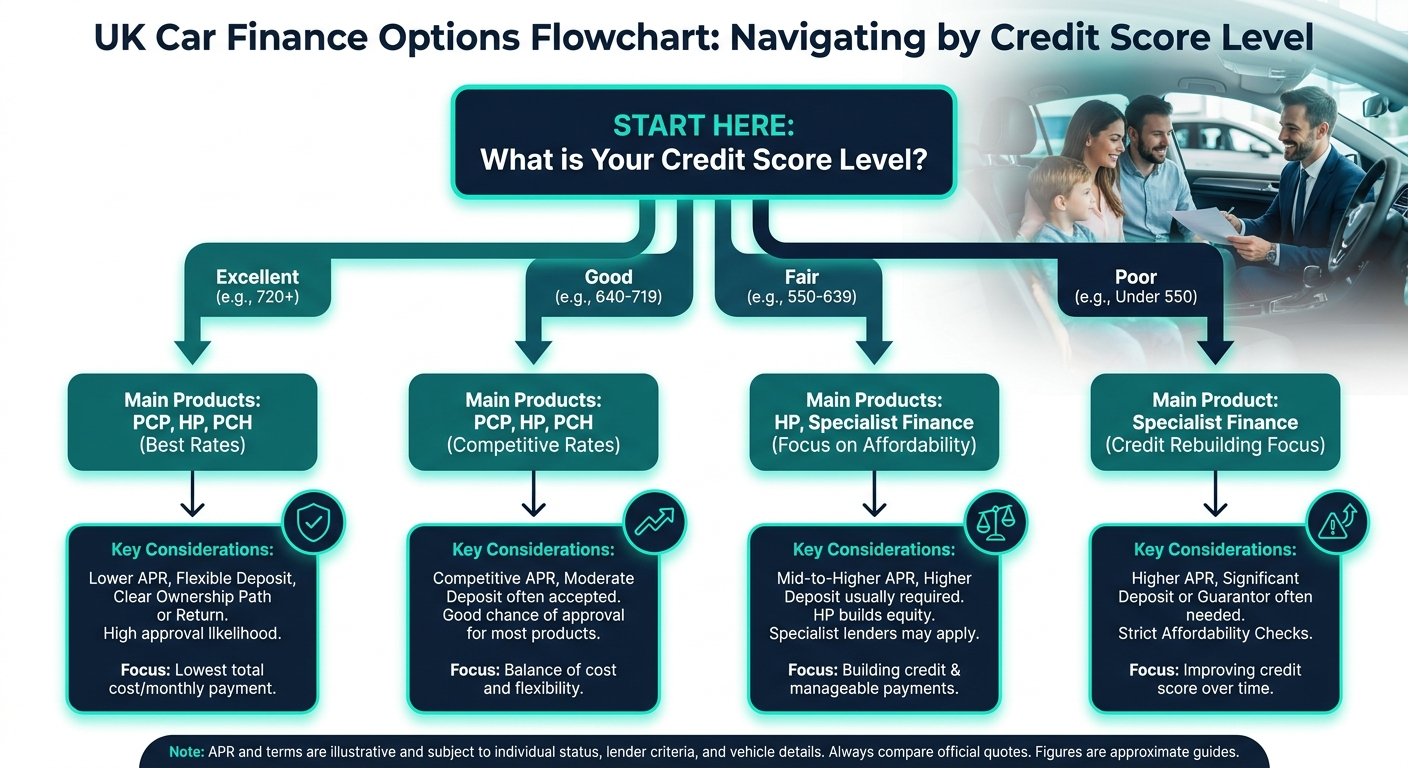

Credit score ranges and what they mean for car finance approval

Credit rating bands determine realistic finance outcomes. Excellent and Good ratings access the widest lender panel and the lowest APRs. A Fair credit rating allows access to hire purchase (HP) and personal contract purchase (PCP), though rates sit above the market average.

Poor and Very Poor ratings are served by specialist subprime lenders. Subprime lending is a regulated market segment that prices for elevated credit risk through higher APRs. HP and PCP remain available across most rating bands; the terms differ, not the product access itself.

What is a credit score and why does it matter for car finance?

A credit score is a numerical rating produced by a credit bureau from an individual's credit history. A credit report is the detailed underlying record from which the score is produced. Lenders assess both: the score as a fast risk signal, and the full report for the underlying detail.

Credit history includes payment records, debt levels, account age, credit mix, and public records such as County Court Judgements (CCJs). Electoral roll registration and residential stability also affect bureau scores.

How a credit score affects the terms of a car finance deal

Credit score determines more than approval status. Many applicants ask whether they will be approved, but the more significant question is what the agreement will cost over the full term. Credit score influences the interest rate charged on a car finance agreement. The interest rate, expressed as APR, directly determines the total amount repayable over the term.

How a credit score affects APR on car finance

Higher credit risk produces a higher interest rate. Lenders express this interest rate as APR and set it higher for lower-rated applications to offset elevated default probability.

An illustrative example based on market data patterns: a £10,000 loan over 48 months at 6.9% APR produces a total repayable of approximately £11,400. The same loan at 29.9% APR produces a total repayable of approximately £16,300. The difference between the two scenarios is more than £4,900.

Applicants should calculate the total amount repayable, not only the monthly figure, before signing any finance agreement.

| Credit rating | Indicative APR range | Notes |

|---|---|---|

| Excellent | 9.9%–14.9% | Best panel rates; low risk pricing |

| Good | 15%–22% | Competitive rates; some lender variation |

| Fair | 22%–30% | Above-average rates |

| Poor | 30%–49% | Subprime pricing; specialist lenders |

| Very Poor | 40%+ | Highest risk tier; deposit strongly advised |

How a credit score affects deposit requirements

Deposit size reduces lender exposure on a car finance agreement. A higher deposit lowers the loan-to-value ratio, which reduces credit risk. Applicants with lower credit scores often face deposit requirements that higher-rated applicants avoid.

An additional deposit of £500 to £1,000 can shift a borderline application from decline to approval at a workable rate. No-deposit car finance exists, but it is most accessible to applicants with Good or Excellent ratings. Applicants with Poor scores should expect no-deposit products to carry notably higher APRs when available at all.

"The deposit is the most underused lever I see borderline applicants overlook. An extra £750 on the table doesn't just reduce the loan amount — it directly reduces the lender's exposure on a higher-risk file. In practice, that shift can move an application from a soft decline into an approval at a workable rate."

Roman Danaev, Car Finance Expert

Car finance routes at a glance

Five main car finance product types are available in the UK, each with different credit score expectations:

- Hire purchase (HP): Fixed payments repay the full vehicle value with no balloon; ownership transfers at term end. More accessible for lower credit scores.

- Personal contract purchase (PCP): Lower monthly payments with a balloon at term end. At conclusion, the borrower returns the vehicle, part-exchanges it, or purchases it at the Guaranteed Minimum Future Value (GMFV). Typically requires a Good or better credit rating.

- Personal loan: Unsecured borrowing used to purchase the vehicle outright.

- Specialist bad credit finance: Regulated subprime products for Poor or Very Poor ratings.

- Guarantor or joint application: A co-applicant with a stronger profile shares liability.

Credit score requirements across these five products are covered in the sections below.

Can car finance be obtained with a bad or low credit score?

Car finance can be obtained with a bad or low credit score. Specialist lenders in the subprime segment serve applicants with Poor and Very Poor ratings, pricing for elevated risk through higher APRs. Credit score determines the lender pool and available terms, not a binary approval or rejection.

CCJ and Default (Finance) records narrow the accessible lender panel but do not prevent approval. A Default (Finance) event on a car finance agreement increases Credit Risk and can lead to vehicle repossession by the lender, so affordability must be assessed honestly before any application is submitted.

PCP finance with a poor credit score: what to expect

Personal Contract Purchase includes a Guaranteed Minimum Future Value (GMFV) component, meaning the lender carries residual vehicle value risk alongside repayment risk. The additional exposure increases Credit Risk for the lender, producing stricter credit score requirements than HP.

Applicants with a Fair or Poor rating (Experian below 720, Equifax below 380, TransUnion below 566) are advised to start with HP and revisit PCP after 12 to 24 months of clean repayment behaviour. Reviewing bad credit car finance options first gives a clearer picture of what is currently accessible.

Hire purchase with a poor credit score: a more accessible route

Hire purchase repays the full vehicle value in fixed monthly installments with no balloon payment. The simpler structure reduces Credit Risk exposure for the lender, producing more accessible eligibility criteria for lower-rated applicants. Using a specialist broker to run a soft credit search identifies eligible lenders without triggering hard search footprints.

Each on-time HP payment is recorded as a positive event on the applicant's credit history, building the foundation for improved terms in future finance agreements. HP monthly payments are typically higher than PCP because the full vehicle value is repaid across the term.

Can car finance improve a credit score?

Car finance improves a credit score when all monthly payments are made on time. Each on-time payment is recorded as a positive credit event on the credit history by the relevant Credit Bureau, and 12 to 24 months of consistent repayments produce a measurable improvement.

The initial application triggers a hard search on the credit file, causing a short-term dip, but this recovers quickly when no further applications follow. A Default (Finance) event produces the opposite effect, registering as negative data on the credit history record. Finance should only be taken on when the monthly cost is genuinely affordable.

What else do lenders consider beyond a credit score?

Credit score is one input in a multi-factor lender assessment. Applicants in the Fair or Poor bands can tip a borderline outcome through non-score factors. Lenders assess seven factors alongside credit score:

- Income and affordability (Debt-to-Income Ratio): Net monthly income versus existing debt commitments. Many lenders require a minimum net monthly income of £1,000 to £1,500.

- Employment stability: Length of current employment and contract type.

- Residential stability: Length of time at current address (three or more years preferred by most lenders).

- Electoral roll registration: Confirmed address on the electoral roll improves bureau scoring.

- Existing debt: Outstanding balances reduce assessed affordability.

- Deposit size: A larger deposit lowers loan-to-value and reduces lender credit risk exposure.

- Vehicle age and type: Most PCP lenders apply vehicle age and mileage criteria at the point of application; thresholds vary by lender.

Key eligibility criteria for car finance in 2026

Most UK lenders apply these baseline entry criteria before any credit assessment begins:

- Age 18 or over

- UK resident with a verifiable address history

- Active UK bank account

- Valid UK driving licence

- Minimum net monthly income of £1,000 to £1,500 (lender-dependent)

- Proof of income (payslips, bank statements, or SA302 for self-employed applicants)

Meeting these criteria confirms entry-level eligibility. Approval depends on the subsequent credit and affordability assessment.

How to improve a credit score before applying for car finance

"The single most overlooked step before a car finance application is checking all three bureau reports — not one, all three. Errors on a file that the applicant never knew existed are far more common than people expect, and correcting a single inaccuracy can produce a 20–40 point improvement in two to four weeks without changing any financial behaviour at all."

Roman Danaev, Car Finance Expert

No shortcuts exist for credit score improvement, but these seven steps produce measurable results, ordered by impact speed:

- Register on the electoral roll at gov.uk/register-to-vote.

- Check all three bureau reports for errors: free via Experian, ClearScore for Equifax data, and Credit Karma for TransUnion data. Dispute any inaccurate entries.

- Reduce credit card utilisation below 30% of the available limit.

- Make all existing payments on time.

- Avoid new credit applications in the three months before applying.

- Keep older credit accounts open.

- Consider a credit-builder card used responsibly for three to six months.

For applicants with recent CCJs or defaults, specialist lenders are the more practical near-term route while credit improvement takes place.

How long does it take to improve a credit score for car finance?

Electoral roll corrections and error disputes produce results within two to four weeks. Credit utilisation reduction and consistent payments improve scores within three to six months.

Recovery from a missed payment requires 12 to 18 months of clean behaviour. CCJ and default records persist for six years but their impact diminishes after two to three years of clean, satisfied behaviour. A 20 to 40 point improvement can open additional lender options.

How to apply for car finance without damaging a credit score

Applying to multiple lenders in quick succession is a common and damaging error. Each full application triggers a hard search, recorded on the credit file and visible to all subsequent lenders. Soft-search eligibility tools identify likely-approve lenders with no credit file footprint.

Car-Finance.co.uk's initial eligibility check uses a soft credit search and does not affect the credit score. A full credit check is carried out by the lender if the application proceeds to a formal agreement.

Step 1: Check all three credit reports for accuracy.

Step 2: Use a soft-search tool to identify likely-approve lenders.

Step 3: Submit one formal application.

Step 4: Receive the lender's decision based on a full credit and affordability assessment.

What to do if refused car finance

A single lender's refusal reflects that lender's specific criteria, not a universal verdict on creditworthiness. Different lenders apply different underwriting models, and an applicant declined by one may be approved by another.

Post-refusal steps:

- Wait 30 days before any new application to avoid clustering hard searches.

- Ask the lender which bureau was queried and the reason for the decline.

- Check the relevant bureau report for errors or unexpected entries.

- Confirm electoral roll registration at the current address.

- Consider specialist lenders such as Moneybarn or GoCarCredit, or a guarantor application.

A refusal is diagnostic information. It identifies what requires attention before the next application, and the bureau queried and the reason given are the starting points for that assessment.

Final thoughts: a credit score is a starting point, not a verdict

A credit score is a snapshot of credit history, not a permanent verdict. No universal minimum applies for car finance. Affordability and deposit size matter as much as the score in borderline cases. Free credit report tools at Experian, ClearScore, and Credit Karma give every applicant a complete picture before approaching any lender.

Check your eligibility in minutes. The initial check uses a soft credit search and does not affect your credit score. A full credit check will be carried out by the lender if you proceed to a formal application.

Most popular questions

We've collected the most popular questions about car loans from our customers

What's the minimum credit score to finance a car?

No minimum credit score applies across all UK lenders. Specialist subprime lenders accept Very Poor applications (Experian below 280, Equifax below 280, TransUnion below 550). Credit score determines the lender pool and the APR offered, not a binary approval outcome. Experian, Equifax, and TransUnion each use a different numerical scale, so no single number applies.

How can I apply for car finance without hurting my credit score?

Soft-search eligibility tools allow applicants to check likely-approve lenders with no footprint on the credit file. Car-Finance.co.uk's initial check is a soft search and does not affect the credit score. A full credit check is carried out by the lender only if the application proceeds to a formal agreement.

How does credit score affect APR?

A lower credit score signals higher credit risk, which lenders offset through a higher APR. On a £10,000 loan over 48 months, the difference between 6.9% APR and 29.9% APR is more than £4,900 in total repayable cost. Car-Finance.co.uk's representative APR is 23.9%. Monthly payment at 23.9% APR on a £10,000 loan over 48 months is approximately £313.

What kinds of car finance are available in the UK (PCP, HP, or loan)?

The main types are hire purchase (HP), personal contract purchase (PCP), personal loan, specialist bad credit finance, and guarantor finance. HP is more accessible for lower credit scores as it carries no balloon payment or residual vehicle value risk. PCP typically requires a Good or higher rating and offers end-of-term flexibility (return, part-exchange, or purchase at GMFV).

Can car finance improve my credit score?

Car finance improves a credit score when all monthly payments are made on time. Each payment is recorded as a positive event by the relevant bureau, and 12 to 24 months of consistent repayments produce a measurable improvement to credit history. Missed payments produce the opposite effect, so finance should only be taken on when the monthly payments are genuinely affordable.

Car-Finance.co.uk is a trading name of Moneyrepublic Ltd (Company No. 12141408). We are an Appointed Representative of F&I Online Ltd (FCA No. 731217), which is authorised and regulated by the Financial Conduct Authority. We are a credit broker, not a lender. All finance is subject to status. Representative 23.9% APR. Based on a loan of £10,000 over 48 months at 23.9% APR: monthly payment approximately £313; total amount repayable approximately £15,024.

Check your eligibility — no impact on your credit score

Leave a request and our experts will contact you shortly to discuss the details.

Author

Roman Danaev is a UK car finance specialist with over a decade in the motor finance industry. He has helped thousands of customers find the right finance deal — from standard HP and PCP agreements to bad credit and no-guarantor options. Roman writes practical, jargon-free guides to help UK drivers make informed borrowing decisions.