Mis-sold car finance: expert guide to reclaiming thousands in undisclosed commissions

Millions of UK car finance customers could receive compensation for mis-sold agreements. The Financial Conduct Authority (FCA) confirmed a motor finance redress scheme on 30 March 2026. The scheme covers agreements from 6 April 2007 to 1 November 2024. Around 12.1 million agreements qualify for compensation (FCA, 2026).

The FCA estimates an average payout around £830 per eligible agreement, with total payouts of £7.5 billion (FCA, 2026). You do not need a claims management company or solicitor. Complaining directly to your lender is free and protects your full payout.

Understanding mis-sold car finance

A mis-sold car finance claim is a type of financial mis-selling complaint where a lender or broker failed to disclose material information about a car finance agreement, including Personal Contract Purchase (PCP) and Hire Purchase (HP) deals.

Mis-selling in car finance falls into four categories:

- Undisclosed commission: the dealer received lender payment without informing you

- Discretionary commission arrangements (DCAs): the dealer could raise your interest rate to earn higher commission

- Pressure selling: the dealer pushed you into a product without time to compare

- Unaffordable lending: the lender approved finance without proper affordability checks

The FCA redress scheme covers three qualifying triggers: undisclosed DCAs, high commission (at least 39% of credit charge and 10% of loan), and undisclosed contractual ties between lender and broker.

Under the Consumer Credit Act 1974, the UK law governing consumer credit, the FCA regulates car finance complaints. If your lender rejects your complaint or misses the scheme deadline, you can escalate to the Financial Ombudsman Service (FOS), a free and independent service whose decisions bind firms.

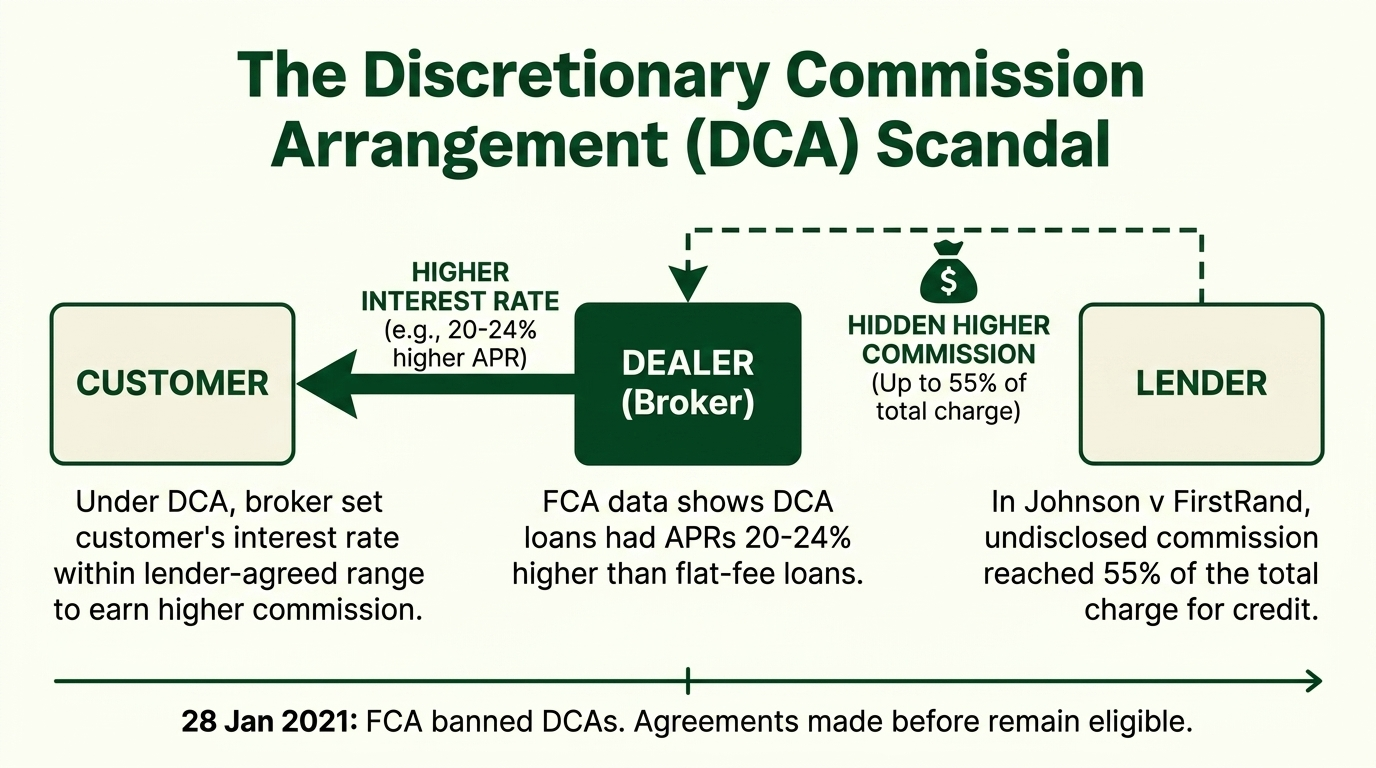

The discretionary commission arrangement scandal

Under a Discretionary Commission Arrangement (DCA), the broker set the customer's interest rate within a lender-agreed range to earn higher commission. FCA data shows DCA loans using reducing and scaled commission models carried annual percentage rates (APRs) 20 to 24% higher than flat-fee loans (FCA, March 2026).

On 28 January 2021, the FCA banned DCAs. Agreements made before that date remain eligible. In the Supreme Court case Johnson v FirstRand (2025 UKSC 33), the undisclosed commission reached 55% of the total charge for credit.

Types of car finance agreements affected

Personal Contract Purchase (PCP) and Hire Purchase (HP) are the two main finance types covered by the FCA redress scheme, both regulated under the Consumer Credit Act 1974.

| Finance type | How it works | Mis-selling risk |

|---|---|---|

| Personal Contract Purchase (PCP) | Lower monthly payments, balloon payment at end | High. DCA commissions inflated interest rates on the majority of new car finance deals |

| Hire Purchase (HP) | Fixed monthly payments, full ownership at end of term | High. Undisclosed commissions increased total cost of credit |

| Conditional sale | Similar to HP, ownership transfers after final payment | Moderate. Covered if commission went undisclosed |

Personal Contract Hire (PCH) and leasing are not covered, as PCH is a rental agreement, not a credit product.

Signs you may have been mis-sold car finance

You have grounds for a mis-sold car finance claim if the dealer or lender withheld key information at the point of sale. FCA research found no DCA casefile customer received commission disclosure (FCA, 2025).

Review your car finance agreement with these questions:

- Did the dealership explain that a commission would be paid by the lender?

- Did the dealer show you finance options from more than one lender?

- Did the dealer explain how the interest rate on your agreement was set?

- Did you receive time to compare the dealer's finance offer with other products?

- Did the lender check that the monthly payments were affordable for your income?

Any "no" answer may indicate mis-selling. The dealer's commission depended on your interest rate, not on finding you the best deal.

Proof includes your finance agreement, dealer correspondence, and interest rate records. Your lender must also check their records under the scheme (FCA, 2026). If you cannot remember your lender, free tools can help.

Check if you're eligible for compensation, free and with no obligation.

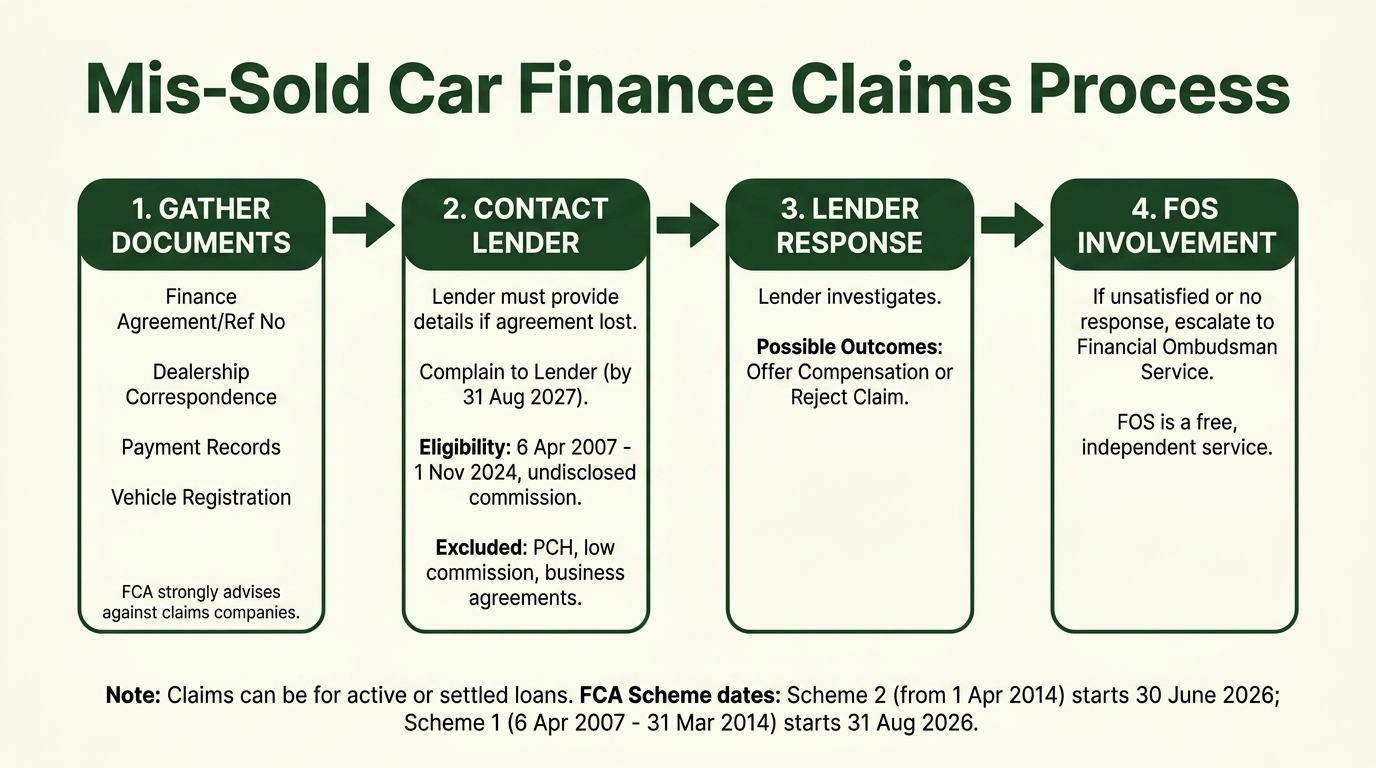

How to check if you can make a claim

Checking your financial mis-selling eligibility takes a few steps. The FCA strongly advises against using claims management companies, which may charge over 30% of any compensation (FCA, 2026).

Gather these documents before contacting your lender:

- Your original finance agreement or reference number

- Dealership correspondence from the time of sale

- Monthly payment records or bank statements showing the lender

- Your vehicle registration or details of the car

If you cannot find your agreement, your lender must provide details on request.

Eligibility criteria for car finance claims

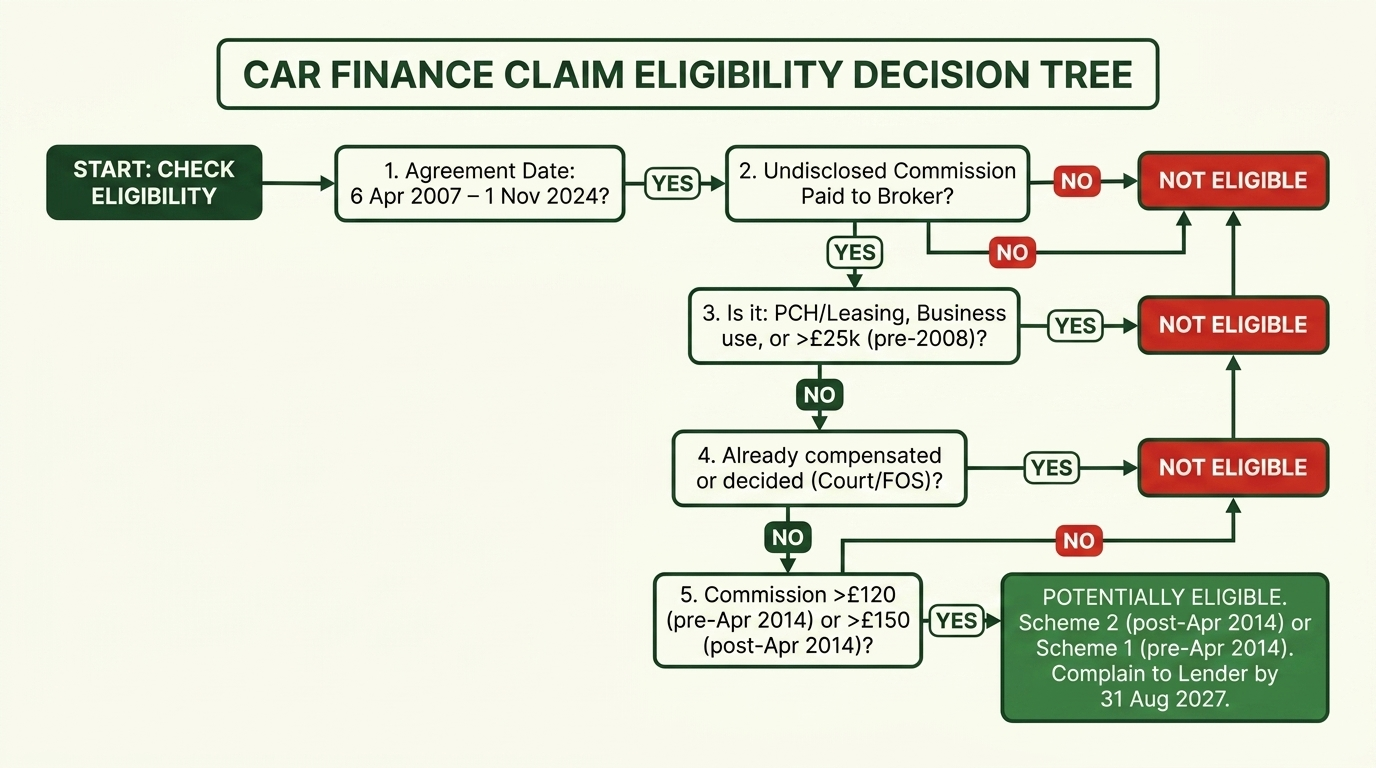

The FCA redress scheme covers regulated motor finance agreements from 6 April 2007 to 1 November 2024. Your agreement qualifies if the lender paid commission to the broker without proper disclosure.

Under the Limitation Act 1980: 6 years from the agreement end, or 3 years from discovery. The FCA does not expect lenders to routinely exclude claims, given poor disclosure during this period (FCA, 2026).

The scheme excludes certain agreements:

- Commission under £120 (pre-April 2014) or under £150 (post-April 2014)

- Personal Contract Hire or leasing arrangements

- Agreements already decided by a court or the Financial Ombudsman

- Cases where you already accepted lender compensation

- Agreements over £25,000 entered into before 6 April 2008

- All business-purpose agreements

Your loan can be active or settled. The FCA split the scheme into two parts. Scheme 2 covers agreements from 1 April 2014 onwards, starting 30 June 2026. Scheme 1 covers agreements from 6 April 2007 to 31 March 2014, starting 31 August 2026.

If your lender has not contacted you, you can still complain until 31 August 2027.

Expected compensation and timelines

The FCA's financial mis-selling redress scheme estimates average payouts of approximately £830 per agreement (FCA, 2026).

| Compensation scenario | How redress is calculated (FCA, 2026) |

|---|---|

| Standard case (post-April 2014) | Average of estimated loss (17% APR adjustment) and commission paid, plus interest |

| Standard case (pre-April 2014) | Average of estimated loss (21% APR adjustment) and commission paid, plus interest |

| High commission (50%+ of credit charge, 22.5%+ of loan, with undisclosed DCA or tie) | Full commission refund plus interest |

| Capped cases (approx. 1 in 3) | Lowest of: 90% of commission, adjusted cost of credit, or actual cost of credit |

FCA scheme compensation includes:

- Refund of excess interest caused by inflated commission arrangements

- Compensatory interest at Bank of England base rate plus 1% (minimum 3% per year)

- Removal of negative credit marks where the mis-selling led to missed payments or defaults

FOS escalation may also yield compensation for distress or inconvenience.

| Timeline | What happens |

|---|---|

| 30 June 2026 | Scheme 2 implementation begins (post-April 2014 agreements) |

| 31 August 2026 | Scheme 1 implementation begins (pre-April 2014 agreements) |

| 3 months after implementation | Lenders must inform existing complainants of their compensation decision |

| 6 months after implementation | Lenders must contact eligible customers who have not yet complained |

| 31 August 2027 | Final deadline to submit a complaint |

If you complained before implementation, you will receive a decision first. The FCA expects to settle millions of claims in 2026, with most resolved by end of 2027.

Legal challenges from Consumer Voice, Volkswagen Financial Services, Mercedes-Benz Financial Services, and CA Auto Finance may delay payouts. The FCA will defend the scheme and advises you to submit complaints now.

Most popular questions

We've collected the most popular questions about car loans from our customers

How do I know if I've been mis-sold car finance?

You were likely mis-sold if the dealership did not disclose lender commission. The FCA found most DCA customers received no disclosure.

How much compensation could I get for mis-sold car finance?

The FCA estimates average compensation at £830 per agreement. Payouts depend on loan size and commission amount. Some claims produce higher amounts where the undisclosed commission exceeded 39% of the total credit charge (FCA, 2026).

Is there a time limit for making a mis-sold car finance claim?

Yes. Under the Limitation Act 1980, the standard period is 6 years from the agreement or 3 years from discovery. If your lender has not contacted you, complain by 31 August 2027.

Can I claim for PCP finance that I've already paid off?

Yes. The FCA scheme covers active and settled PCP agreements from 6 April 2007 to 1 November 2024, if the lender did not disclose commission.

What documents do I need to make a mis-sold car finance claim?

You need your finance agreement number or lender's name. Your lender must provide details on request. Bank statements can also help.

How long does a car finance claim take?

Lenders have three months after implementation to respond. If you complain before 30 June 2026, you will receive a decision sooner.

Can I make a claim if my dealer has gone out of business?

Yes. Your complaint targets the finance lender, not the dealership. The lender remains responsible.

What is a discretionary commission arrangement?

A DCA allowed the car dealer to set your interest rate within a range to earn higher commission. The FCA banned DCAs on 28 January 2021.

Do I need a lawyer to make a car finance claim?

No. The FCA scheme is free. Claims management companies may charge over 30% of your compensation. Complain directly to your lender using the FCA's process.

Will making a claim affect my credit score?

No. Submitting a mis-sold car finance complaint does not affect your credit score. If your claim succeeds, your lender may remove negative credit marks.

Check if you're eligible for compensation. You can complain to your lender at no cost and with no obligation.

This information is for guidance only. If you believe you have been mis-sold car finance, contact your lender directly or seek independent legal advice. Car-Finance.co.uk is not a claims management company.

Car-Finance.co.uk is a trading name of Moneyrepublic Ltd (Company No. 12141408). We are an Appointed Representative of F&I Online Ltd (FCA No. 731217), which is authorised and regulated by the Financial Conduct Authority.

Check your eligibility — no impact on your credit score

Leave a request and our experts will contact you shortly to discuss the details.

Author

Roman Danaev is a UK car finance specialist with over a decade in the motor finance industry. He has helped thousands of customers find the right finance deal — from standard HP and PCP agreements to bad credit and no-guarantor options. Roman writes practical, jargon-free guides to help UK drivers make informed borrowing decisions.