Step-by-step guide: how to claim PCP/HP car finance compensation

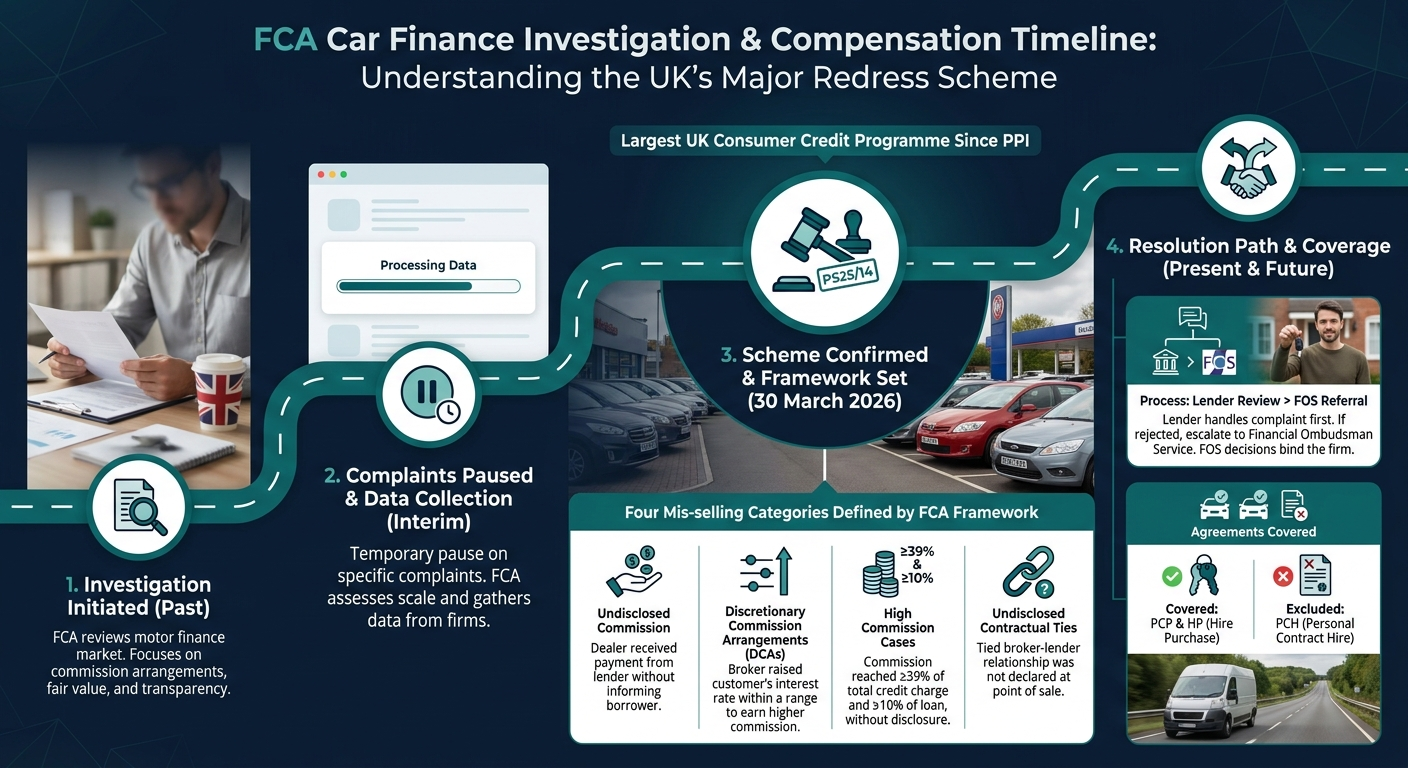

UK drivers can claim compensation for mis-sold PCP and HP car finance under the FCA motor finance redress scheme, confirmed on 30 March 2026. The scheme covers 12.1 million agreements signed between 6 April 2007 and 1 November 2024, with an £830 average payout and a £7.5 billion total redress pool (FCA, 2026). Direct complaints to lenders are free, and the final deadline is 31 August 2027.

Important: If you believe you have been mis-sold car finance, contact your lender directly or seek independent legal advice.

Car-Finance.co.uk is not a claims management company.

Understanding car finance mis-selling and the FCA car finance update

The FCA motor finance redress scheme is the largest UK consumer credit programme since Payment Protection Insurance, confirmed on 30 March 2026 (FCA Policy Statement PS25/14).

Mis-selling under the FCA framework falls into four categories:

- Undisclosed commission: the dealer received payment from the lender without informing the borrower.

- Discretionary Commission Arrangements (DCAs): the broker raised the customer's interest rate within a lender-set range to earn higher commission.

- High commission cases: commission reached at least 39% of total credit charge and 10% of the loan, without disclosure.

- Undisclosed contractual ties: a tied broker-lender relationship was not declared at point of sale.

PCP and HP agreements are covered. Personal Contract Hire is excluded. The Financial Ombudsman Service handles disputes when a lender rejects a complaint, and its decisions bind the firm.

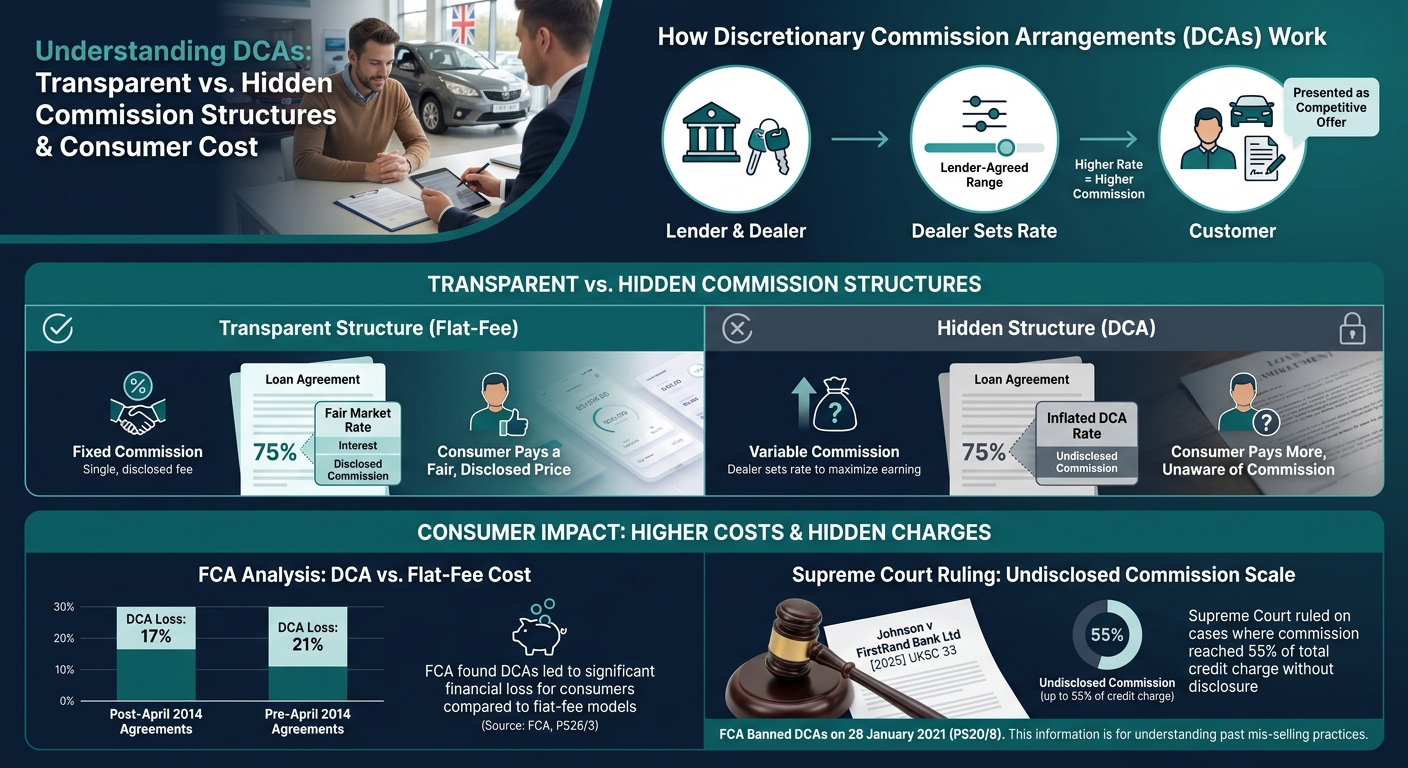

The hidden commission scandal and Discretionary Commission Arrangements (DCAs)

A Discretionary Commission Arrangement is a model where dealers set the customer's interest rate within a lender-agreed range, earning higher commission for higher rates. FCA analysis found DCA loans carried APRs equivalent to a loss of 17% (post-April 2014 agreements) and 21% (pre-April 2014 agreements) compared to flat-fee arrangements (FCA, PS26/3, March 2026).

Dealers presented DCA-inflated rates as competitive offers without disclosing the commission structure. The FCA banned DCAs on 28 January 2021 through Policy Statement PS20/8. In Johnson v FirstRand Bank Ltd UKSC 33, the Supreme Court ruled on a case where the undisclosed commission reached 55% of the credit charge (Supreme Court judgment).

The FCA's investigation and regulatory response

The Financial Conduct Authority opened its motor finance review in January 2019 after concerns that commission models inflated consumer costs. The FCA's final findings, published March 2019, identified DCAs as the highest-risk commission model. Policy Statement PS20/8 confirmed the ban from 28 January 2021 (FCA PS20/8).

In January 2024, the FCA opened a Section 166 skilled-persons review of historic complaints. The Court of Appeal's October 2024 rulings in Hopcraft, Wrench, and Johnson expanded disclosure obligations on dealers acting as credit brokers. Following the Supreme Court's August 2025 judgment, Policy Statement PS25/14 finalised the redress scheme on 30 March 2026, establishing the compensation framework across 12.1 million qualifying agreements.

How to check if you are eligible for car finance compensation

A car finance agreement qualifies if it was signed between 6 April 2007 and 1 November 2024 and the lender paid commission to the broker without proper disclosure. The agreement can be active or fully settled.

The FCA scheme excludes:

- Commission below £120 (pre-April 2014) or £150 (from April 2014).

- Personal Contract Hire and any lease or rental product.

- Agreements decided by a court or by the Financial Ombudsman Service.

- Cases where the customer accepted prior compensation.

- Business-purpose agreements of any size.

- Agreements above £25,000 entered before 6 April 2008.

Scheme 2 covers post-April 2014 agreements and starts on 30 June 2026. Scheme 1 covers earlier agreements and starts on 31 August 2026.

What qualifies for PCP and HP compensation

Personal Contract Purchase carries lower monthly payments and a final balloon payment that reflects the car's Guaranteed Minimum Future Value. The balloon is calculated against expected depreciation, so depreciation directly affects the customer's options at term end. Hire Purchase carries fixed monthly payments and full ownership transfer at term end.

PCP claims dominate the scheme because dealers used DCAs heavily on new car finance. HP claims focus on the total cost of credit raised by undisclosed commission.

| Finance type | How it works | Mis-selling risk |

|---|---|---|

| Personal Contract Purchase (PCP) | Lower monthly payments, balloon at end | High. DCA commission inflated APRs. |

| Hire Purchase (HP) | Fixed payments, ownership transfers at end | High. Undisclosed commission raised cost of credit. |

| Conditional Sale | Fixed payments, ownership transfers automatically | Moderate. Covered when commission was undisclosed. |

PCH and operating leases sit outside the scheme.

Identifying red flags in your car finance agreement

Red flags appear when contract terms specify an APR materially higher than the lender's advertised rate, when documentation lacks any disclosure of dealer commission, or when only one finance option was presented. Early repayment charges built into contract terms can signal a structure designed to deter refinancing.

Five questions help drivers identify potential mis-selling:

- Did the dealership disclose that the lender paid commission?

- Did the dealer present finance options from more than one lender?

- Did the contract terms explain how the interest rate was set?

- Did the customer have time to compare quotes from other sources?

- Did the agreement include early repayment charges that locked in the APR?

A "no" answer points to potential mis-selling. The FCA's review found no customer in its DCA casefile sample received a clear commission disclosure (FCA, 2026).

| Clause area | Legitimate | Red flag | Why it matters |

|---|---|---|---|

| Commission disclosure | Commission amount named in writing before signing | No mention of commission anywhere in the agreement | FCA found zero customers in its DCA sample received clear disclosure |

| APR setting | Rate matches lender's advertised APR; setter identified | APR materially exceeds advertised rate with no explanation | Gap between rates is the primary DCA indicator |

| Finance options | Multiple lender quotes documented | Only one lender presented; no alternatives on record | Single-lender steering violates FCA CONC 2.5 fair treatment rules |

| Early repayment | ERC capped at statutory limit; basis stated | Maximum ERC combined with inflated APR | Structure may be designed to deter refinancing at a lower rate |

| Pre-contract period | SECCI delivered; reflection time documented | Agreement signed same day; no comparison period recorded | No reflection period removes the customer's ability to compare quotes |

| Lender identity | Full legal name and FCA reference number included | Trading name only; no FCA registration number | Without an FRN the customer cannot verify the lender is authorised |

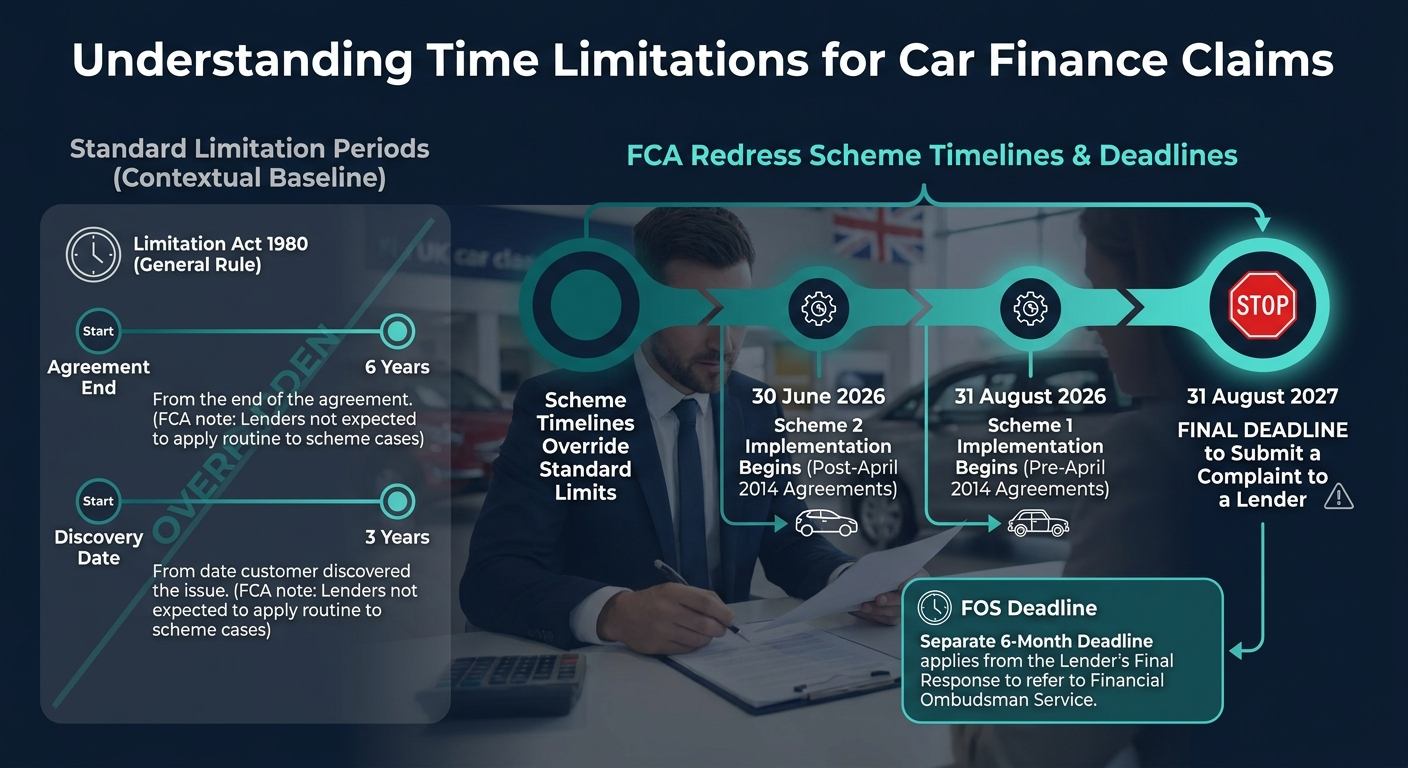

Understanding time limitations for car finance claims

The Limitation Act 1980 sets two relevant periods. Six years apply from the end of the agreement. Three years apply from the date the customer discovered the issue. The FCA does not expect lenders to apply these limits routinely to scheme-eligible cases.

The redress scheme dates override standard limitation periods:

- 30 June 2026: Scheme 2 implementation begins (post-April 2014 agreements).

- 31 August 2026: Scheme 1 implementation begins (pre-April 2014 agreements).

- 31 August 2027: Final deadline to submit a complaint to a lender.

The Financial Ombudsman Service applies a separate six-month deadline from the lender's final response.

Step-by-step guide to making a successful car finance claim

The complaint process is direct and free, running in seven steps:

- Locate the lender. The lender is responsible for redress, not the dealer.

- Gather documents: finance agreement, statements, dealer correspondence, welcome pack.

- Write a complaint letter referencing the agreement number, date, and basis of complaint.

- Submit the complaint by email or to the registered office address.

- Wait for the final response. Lenders have three months from scheme implementation.

- Review the offer or rejection, which states the outcome and right to escalate.

- Escalate to the Financial Ombudsman Service if needed. The service is free and binding.

The FCA strongly advises against engaging a claims management company, which may charge 30% or more of the eventual payout (FCA, 2026).

Documentation and evidence collection

Strong claims rely on the original finance agreement, dealer correspondence, monthly statements, the lender's welcome pack, and any settlement figure issued at term end.

A driver without the original paperwork can request a copy under the Consumer Credit Act 1974. Section 77 (Hire Purchase) and Section 78 (running-account credit) require the lender to supply the agreement on payment of a £1 statutory fee (GOV.UK consumer protection). The lender must respond within 12 working days. Bank statements and credit reports from Experian, Equifax, or TransUnion can identify the lender.

Required documents

- Original finance agreement

- Dealer correspondence

- Monthly statements

- Lender's welcome pack

- Settlement figure (if issued at term end)

If documents are missing

Request copies under the Consumer Credit Act 1974:

- S.77 (Hire Purchase) or S.78 (running-account credit)

- £1 statutory fee per request

- Lender must respond within 12 working days

To identify the lender

- Bank statements showing payment recipient

- Credit report from Experian, Equifax, or TransUnion

Approaching lenders directly versus using claims companies

Direct complaints are free and protect the full value of any award. Regulated claims companies operate as paid intermediaries authorised by the Financial Conduct Authority and charge success fees as a percentage of the award. Success fees typically reach 30% to 36%, reducing an £830 average payout to roughly £540.

| Approach | Fee | Effort | Speed |

|---|---|---|---|

| Direct complaint to lender | £0 | One letter | Up to 3 months |

| Financial Ombudsman Service escalation | £0 | Online form | 3 to 12 months |

| Regulated claims company | 30% to 36% success fee | Minimal | Same as direct |

The Financial Ombudsman Service remains accessible whether the customer complains directly or through a regulated claims company.

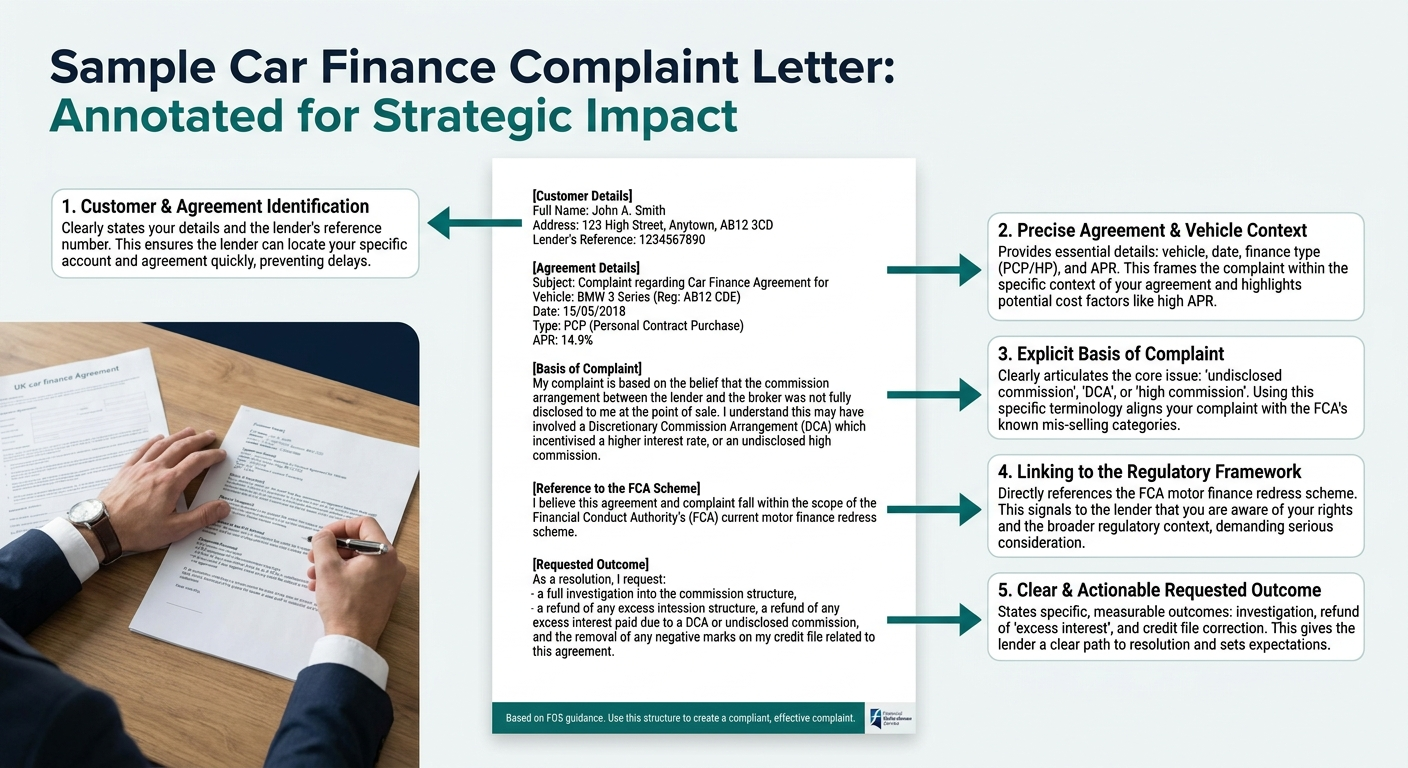

Writing an effective complaint letter

A car finance complaint letter must identify the agreement, state the basis of complaint, and request a specific outcome. A compliant complaint letter contains five elements:

- Customer details: full name, address, lender's reference number.

- Agreement details: date, vehicle, finance type (PCP or HP), and APR.

- Basis of complaint: undisclosed commission, DCA arrangement, or high commission.

- Reference to the FCA scheme: state that the complaint falls within the FCA motor finance redress scheme.

- Requested outcome: refund of excess interest, refund of commission, removal of negative credit marks.

The Financial Ombudsman Service publishes a free complaint template (FOS consumer guidance).

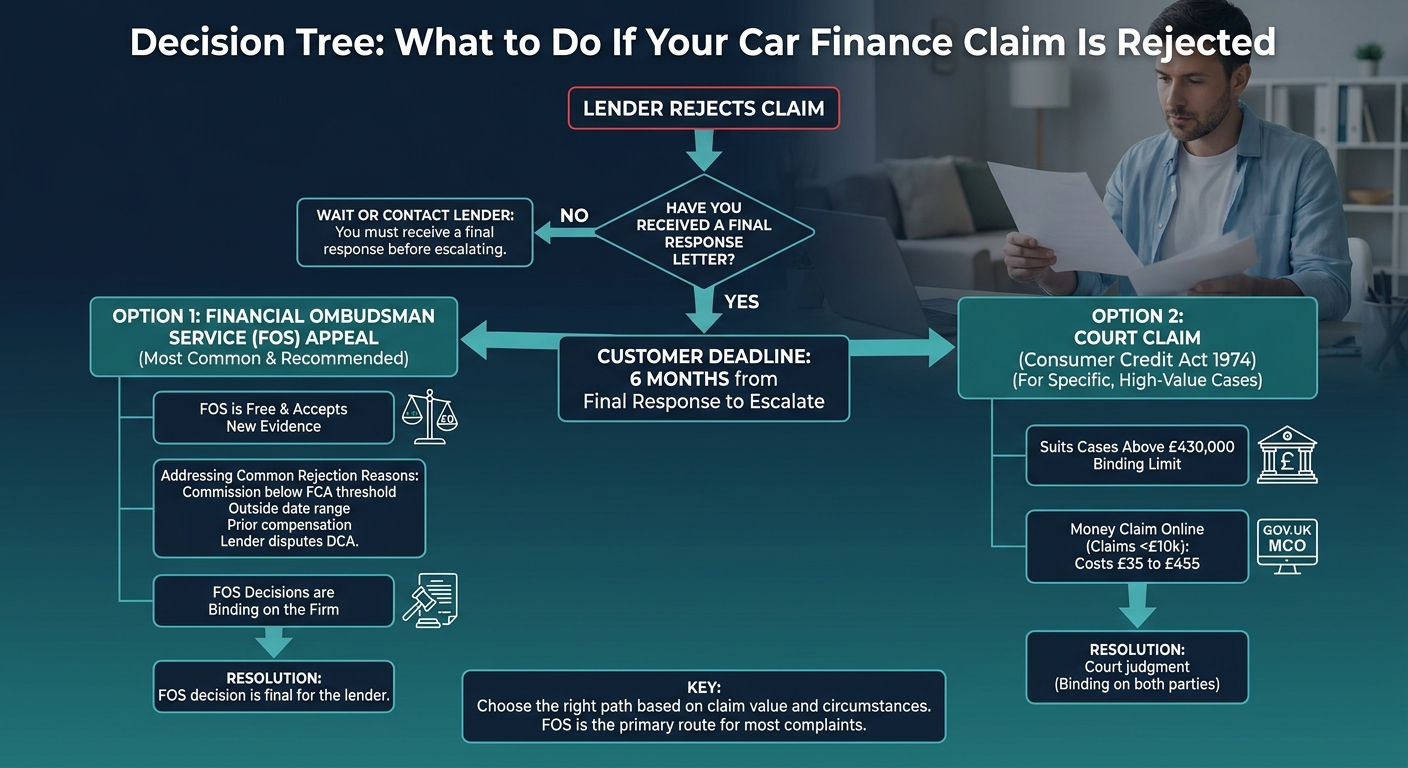

What to do if your claim is rejected

A rejected claim has two viable next steps: the appeals process through the Financial Ombudsman Service, or, in narrow circumstances, a court claim under the Consumer Credit Act 1974. The service handles the majority of rejected motor finance complaints and binds firms on its decisions (FOS, car finance complaints).

The customer must trigger the appeals process within six months of the lender's final response. The service charges nothing and accepts new evidence. Common rejection reasons addressed through the appeals process include:

- Commission claimed below the FCA threshold (£120 pre-2014, £150 post-2014).

- Agreement falling outside the qualifying date range.

- Customer accepting prior compensation.

- Lender disputing whether a DCA applied.

A court claim suits cases above the £430,000 binding limit. Money Claim Online handles claims under £10,000 for £35 to £455 (GOV.UK Money Claim Online).

Potential compensation amounts and timeframes

The FCA estimates an average payout of £830 per agreement, with a £7.5 billion total redress pool across 12.1 million agreements (FCA, 2026). Outcomes vary by loan size, commission level, and APR adjustment.

The redress scheme calculates compensation in three ways:

| Compensation scenario | How redress is calculated |

|---|---|

| Standard case (post-April 2014) | Average of APR-adjusted loss (17% cap) and commission paid, plus interest. |

| Standard case (pre-April 2014) | Average of APR-adjusted loss (21% cap) and commission paid, plus interest. |

| High commission case (50%+ of credit charge, 22.5%+ of loan) | Full commission refund plus interest. |

Around one-third of qualifying claims fall under a cap that limits payouts to the lowest of: 90% of commission, the adjusted cost of credit, or the actual cost of credit (FCA PS26/3, 2026). Compensatory interest applies at the Bank of England base rate plus 1%, minimum 3% per year.

How compensation is calculated: the expert view

The FCA redress methodology uses comparative redress as the calculation framework. The hybrid remedy settlement calculation contrasts the customer's actual cost of credit against a benchmark derived from FCA market data — the interest they would have paid at an APR 17% (or 21% for pre-2014 agreements) lower than their actual rate (FCA PS26/3, 2026). The difference plus statutory interest forms the redress figure.

The standard formula has three steps:

- The lender calculates actual interest paid based on the original APR.

- The lender calculates notional interest at a benchmark APR (17% post-April 2014, 21% pre-April 2014).

- The lender awards the difference plus compensatory interest at base rate plus 1%.

Comparative redress also captures secondary harms, including credit file damage and refinancing costs.

Lender-specific considerations and blackhorse finance claims

Black Horse Finance, a Lloyds Banking Group subsidiary, ranks among the largest UK motor finance lenders by expected claim volume. Other major lenders include MotoNovo Finance (FirstRand), Santander Consumer Finance, Barclays Partner Finance, Close Brothers Motor Finance, and BMW Financial Services. Johnson v FirstRand Bank Ltd [2025] UKSC 33 directly addressed MotoNovo's commission practices.

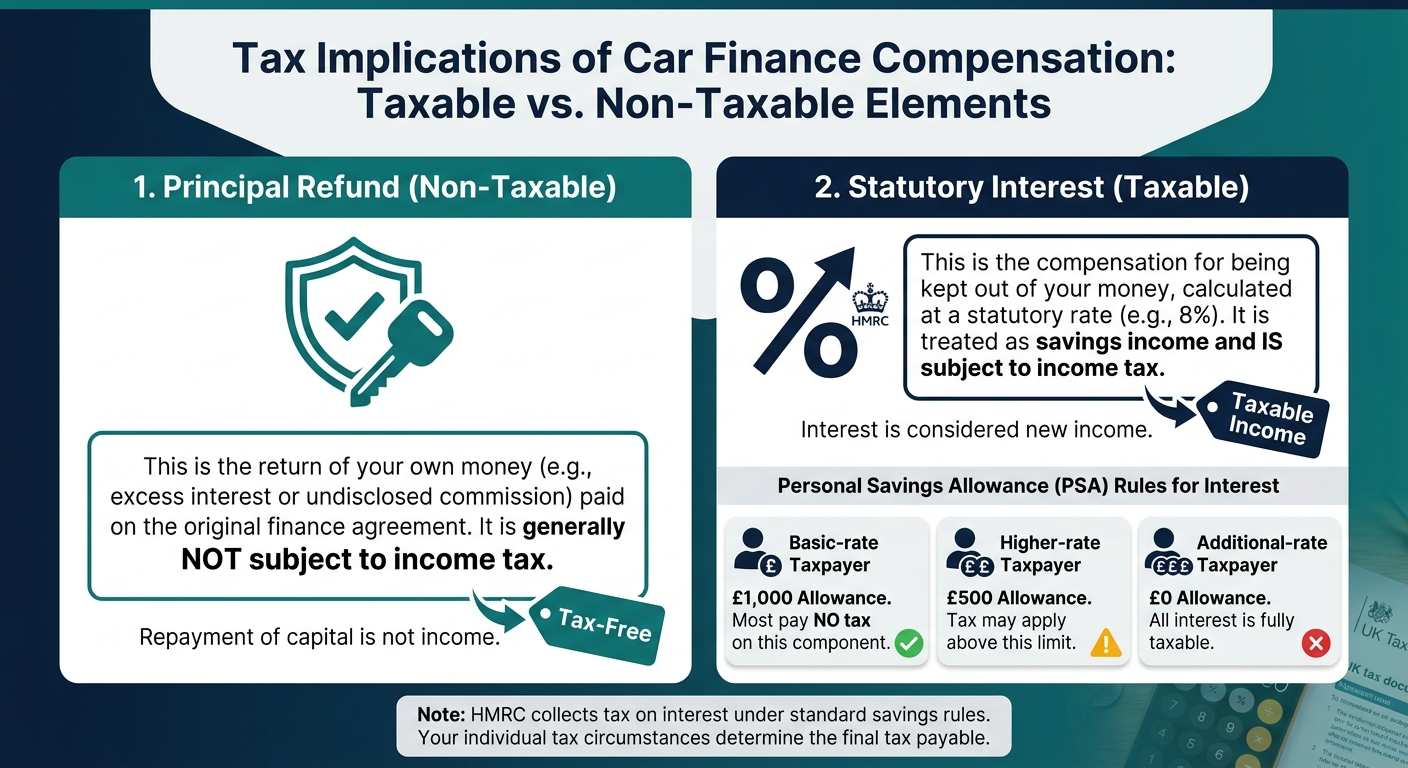

Tax implications of car finance compensation

Compensation contains two components: the principal refund and statutory interest. The principal refund is generally not taxable. Statutory interest is taxable as savings income, with HMRC collecting interest tax under standard savings rules (HMRC Personal Savings Allowance).

Most basic-rate taxpayers fall inside the £1,000 Personal Savings Allowance and pay no interest tax on the redress component. Higher-rate taxpayers have a £500 allowance, and additional-rate taxpayers receive no allowance.

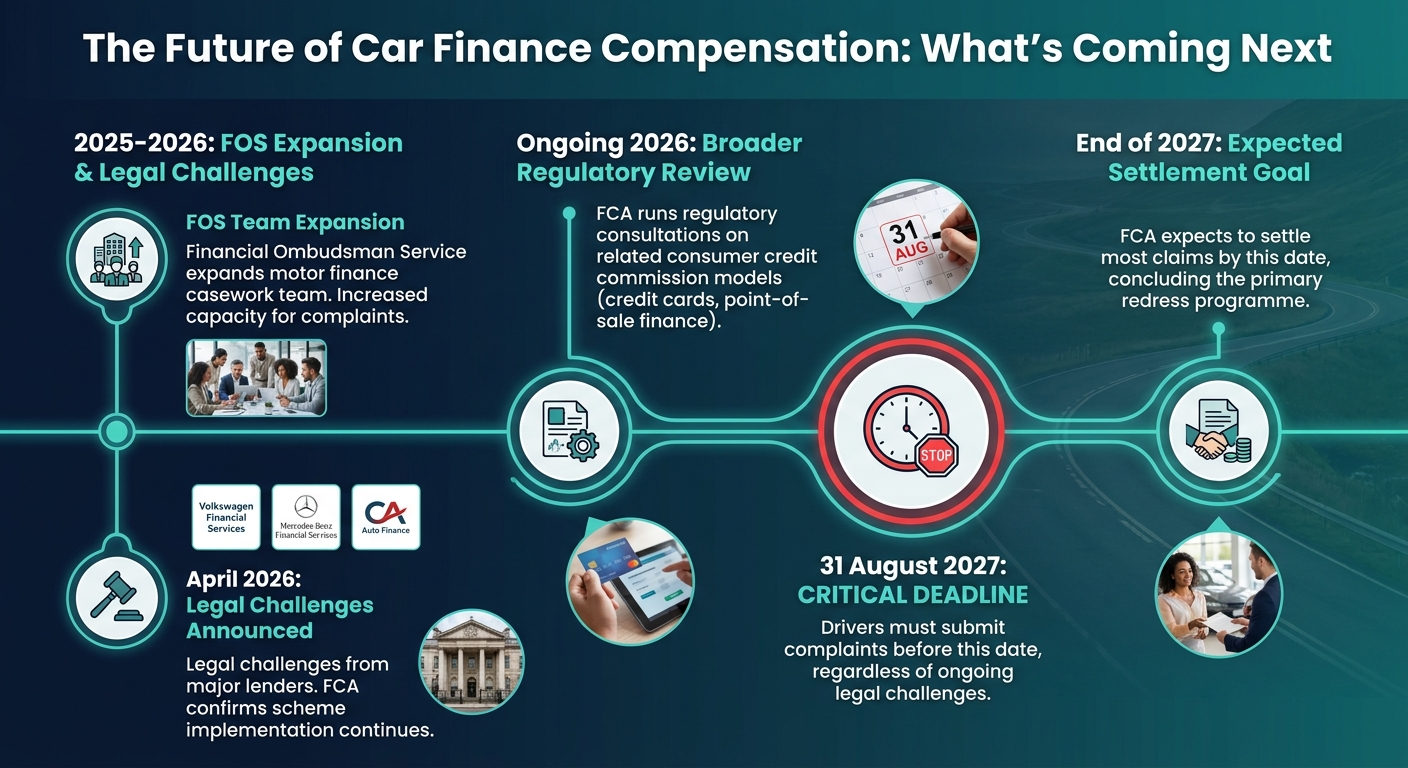

The future of car finance compensation: what's coming next

The FCA expects to settle most claims by the end of 2027. Volkswagen Financial Services, Mercedes-Benz Financial Services, and CA Auto Finance announced legal challenges in April 2026, but the FCA confirmed implementation will continue.

The FCA continues to run regulatory FCA consultations on related consumer credit commission models, including credit cards and point-of-sale finance. The Financial Ombudsman Service has expanded its motor finance casework team for 2025-2026 (FOS plan and budget). Drivers should submit complaints before the 31 August 2027 deadline regardless of legal challenges.

Conclusion: taking action on your car finance claim

A driver with a PCP or HP agreement signed between 6 April 2007 and 1 November 2024 has a clear route to compensation. The complaint process is free, escalation to the Financial Ombudsman Service is free, and the 31 August 2027 deadline leaves time to act.

Three immediate steps protect a potential claim:

- Locate the original finance agreement and identify the lender.

- Submit a written complaint directly to the lender, referencing the FCA motor finance redress scheme.

- Reject any claims management company offer that takes a percentage of the payout.

Most popular questions

We've collected the most popular questions about car loans from our customers

Am I entitled to compensation for my car finance?

A customer is entitled if the agreement falls between 6 April 2007 and 1 November 2024 and the lender paid commission without proper disclosure. The FCA's three triggers cover undisclosed DCAs, high commission cases, and undisclosed contractual ties.

How do I apply for car finance compensation?

A customer applies by sending a written complaint directly to the lender, free of charge. The complaint should reference the FCA motor finance redress scheme and include the agreement number. Lenders have three months to respond.

How much will car finance claims be paid?

The FCA estimates an average payout of £830. Standard cases use a 17% APR benchmark for post-April 2014 agreements and 21% for earlier ones. High commission cases qualify for a full commission refund plus interest.

What evidence do I need to support my claim?

A strong claim relies on the original finance agreement, monthly statements, dealer correspondence, and the welcome pack. Section 77 of the Consumer Credit Act 1974 entitles the customer to a copy of the agreement for £1.

How long does it typically take to receive compensation?

Lenders have three months from scheme implementation. Financial Ombudsman Service escalation typically adds three to twelve months.

Car-Finance.co.uk is a trading name of Moneyrepublic Ltd (Company No. 12141408). We are an Appointed Representative of F&I Online Ltd (FCA No. 731217), which is authorised and regulated by the Financial Conduct Authority.

Ready to Find Your Car Finance?

Check your eligibility in minutes — no impact on your credit score.

Rates from 9.9% APR: the exact rate you will be offered will be based on your circumstances, subject to status. Representative Hire purchase (HP) example: borrowing £7,000 over 5 years with a representative APR of 21.9%, the annual interest rate of 21.9% (Fixed) and a deposit of £0, the amount payable would be £185.33 per month, with a total cost of credit of £4,119.81 and a total amount payable of £11,119.81. We look to find the best rate from our panel of lenders and will offer you the best deal that you're eligible for. We receive a fixed fee commission per finance agreement, or we receive a commission based on a percentage of the total amount of finance taken. This will not affect the interest rate offered or the total amount repayable. Our service is free.

Check your eligibility — no impact on your credit score

Leave a request and our experts will contact you shortly to discuss the details.

Author

Roman Danaev is a UK car finance specialist with over a decade in the motor finance industry. He has helped thousands of customers find the right finance deal — from standard HP and PCP agreements to bad credit and no-guarantor options. Roman writes practical, jargon-free guides to help UK drivers make informed borrowing decisions.