Voluntary termination car finance: what your lender isn't telling you about your right to walk away

Voluntary termination is a statutory right under Section 99 of the Consumer Credit Act 1974. The right lets you end a Hire Purchase (HP) or Personal Contract Purchase (PCP) car finance agreement once you have paid 50% of the total amount payable. The finance company cannot legally refuse a valid voluntary termination request. You return the car in reasonable condition, walk away from the remaining payments, and your credit file records the agreement as "voluntarily terminated" rather than as a default.

Most lenders do not advertise this right because exercising it cuts their interest income short. Around 1.6 million UK consumers signed new car finance agreements in 2024 according to the Finance & Leasing Association, yet voluntary termination remains one of the least understood consumer protections in UK credit law. This guide explains the calculation, the process, the timing, and the routes available if the 50% threshold has not yet been reached.

What is voluntary termination on car finance?

Voluntary termination (VT) is a statutory consumer right that allows a borrower to end a regulated Hire Purchase or Personal Contract Purchase agreement early. The borrower returns the vehicle and pays any shortfall up to 50% of the total amount payable. Section 99 of the Consumer Credit Act 1974 grants the right and no contractual clause can override it.

Finance companies process VT requests routinely but rarely raise the option. The default lender response to a struggling customer is restructured payments or settlement quotes. Voluntary termination is customer-initiated and must be requested in writing citing the statute.

The legal basis: Section 99 of the Consumer Credit Act 1974

Section 99 of the Consumer Credit Act 1974 grants the borrower the right to terminate a regulated hire purchase or conditional sale agreement at any point before the final payment falls due. Section 100 caps the liability: the borrower must bring total payments up to one half of the total price, plus any installments already accrued and any reasonable sum for damage. The lender cannot demand future interest or the balloon payment as a condition of termination.

Which finance agreements qualify for voluntary termination?

Both Hire Purchase and Personal Contract Purchase agreements qualify for voluntary termination under the Consumer Credit Act 1974. Personal Contract Hire and operating leases do not qualify because they are rental contracts with no credit element.

Eligible agreements include:

- Hire Purchase (HP), with fixed monthly payments and ownership transferring after the final payment

- Personal Contract Purchase (PCP), with monthly payments plus an optional final balloon payment

- Conditional sale agreements, which mirror HP structure with ownership at term end

Ineligible agreements include:

- Personal Contract Hire (PCH), a pure rental arrangement with no ownership option

- Operating leases for business or consumer use

- Subscription car services billed monthly with no credit agreement

The front page of the finance document names the product. The phrase "regulated by the Consumer Credit Act 1974" confirms statutory VT rights apply.

What is the voluntary termination clause in a finance agreement?

The voluntary termination clause is the section of a car finance agreement that mirrors the statutory VT right granted by Section 99. The clause typically appears under headings such as "Your Right to Terminate" or "Ending the Agreement Early." A contractual clause cannot reduce the statutory right; if the clause is narrower than the Act, the statute prevails.

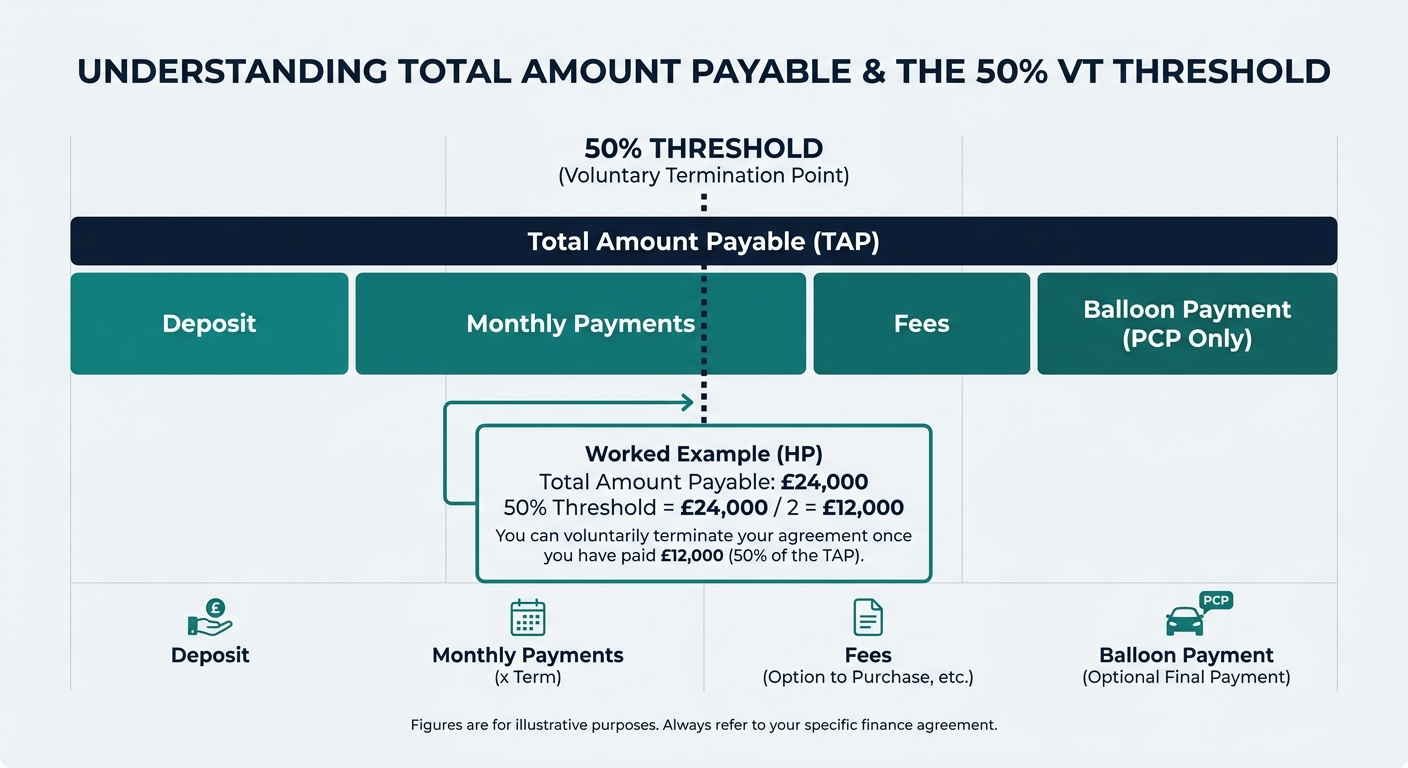

How does the 50% threshold work? Understanding the qualifying calculation

The 50% threshold is calculated against the Total Amount Payable (TAP) on the finance agreement, not against the vehicle's purchase price. The Total Amount Payable is the sum of the deposit, all monthly payments over the full term, all fees, and (for PCP) the balloon payment. Half of that figure is the threshold the customer must reach before walking away.

This is the single most misunderstood number in car finance. A customer who calculates 50% of the car's sticker price will usually conclude they qualify earlier than they actually do. The lender's documentation states the TAP on page one of the agreement; that is the figure that matters.

Worked example for HP: a vehicle priced at £20,000 with £4,000 interest over four years gives a Total Amount Payable of £24,000. The 50% threshold is £12,000. The customer must have paid £12,000 in total (deposit plus monthly payments) before VT becomes available.

What counts towards the 50% threshold?

Every payment made under the agreement counts towards the 50% threshold. The Total Amount Payable is the denominator; everything you have paid is the numerator.

Payments included in the 50% calculation:

- The deposit paid at the start of the agreement

- All monthly payments made to date

- Any upfront fees added to the credit amount, such as documentation or option-to-purchase fees

- Any voluntary overpayments credited against the balance

The deposit is the most commonly overlooked component. A customer who put down £3,000 and has paid £8,000 in monthly installments has paid £11,000 toward the threshold, not £8,000.

What does not count towards the 50% threshold for PCP agreements?

For PCP agreements, the balloon payment is included in the Total Amount Payable for threshold calculation but does not need to be paid to exercise VT. The balloon inflates the denominator, which raises the absolute 50% figure, yet the customer is not required to pay the balloon to walk away.

Worked example for PCP: a £15,000 vehicle with £3,000 interest and a £6,000 Guaranteed Future Value (GFV / balloon payment) gives a Total Amount Payable of £24,000. The 50% threshold is £12,000. If you have paid £12,000 in deposit plus monthly payments, you can exercise VT and return the car. You do not pay the £6,000 balloon.

The balloon mathematically reduces monthly payments during the term, which is the main appeal of PCP. Reaching the 50% threshold on a PCP therefore takes longer in calendar time than on an equivalent HP.

How to calculate whether the halfway point has been reached

A four-step calculation confirms whether the 50% threshold has been reached on any HP or PCP agreement:

- Locate the Total Amount Payable on the front page of the finance agreement. Request it in writing from the lender if you cannot find it.

- Divide the Total Amount Payable by two. This figure is your threshold.

- Add the deposit you paid at the start to the total of all monthly payments made to date.

- Compare the total paid against the threshold. If the total paid equals or exceeds the threshold, you can exercise VT now.

If the total paid is below the threshold, you can continue making payments until the threshold is met or pay the shortfall in a single sum at the point of termination. Lenders typically require any arrears to be cleared before VT processing begins.

Voluntary termination vs. voluntary surrender: a distinction that could cost thousands

Voluntary termination and voluntary surrender are not interchangeable. Voluntary termination is a statutory right that caps your liability at 50% of the Total Amount Payable. Voluntary surrender is an informal return of the vehicle that leaves you liable for the entire outstanding balance minus the sale proceeds. Confusing the two is one of the most expensive mistakes in UK car finance.

The two outcomes diverge sharply on credit consequences. Voluntary termination is recorded as "voluntarily terminated" on your credit file, which is a visible marker but not a default. Voluntary surrender often results in a default registration once the lender writes off the shortfall, which damages your credit score for six years.

| Feature | Voluntary termination | Voluntary surrender |

|---|---|---|

| Legal basis | Section 99, Consumer Credit Act 1974 | No statutory right; informal lender process |

| Eligibility | 50% of Total Amount Payable paid | Available at any time |

| Outstanding debt after return | None, beyond reasonable damage | Full shortfall after vehicle sale |

| Credit file marker | "Voluntarily terminated" | Often recorded as default |

| Recommended for | Customers at or beyond the 50% threshold | Rarely the best option; consider VT first |

What is voluntary surrender?

Voluntary surrender is the informal return of a financed vehicle to the lender without meeting the 50% threshold. The lender sells the car, deducts the sale proceeds from the outstanding balance, and pursues the shortfall as a debt. The customer remains contractually liable for the full balance until the shortfall is paid.

The shortfall is often substantial. If it remains unpaid, the lender or a debt collection agency may register a default on the customer's credit file, which can stay visible for six years under Information Commissioner's Office guidance on credit reference reporting.

Why the wrong choice can cost thousands

The financial gap between voluntary termination and voluntary surrender is large in any case where both options are open. Consider a customer with £15,000 Total Amount Payable who has paid £5,000.

Under voluntary surrender, the customer returns the car. The lender sells it at auction for £6,000. The outstanding balance after the sale is £10,000 minus £6,000, which is £4,000. The customer owes that £4,000 immediately and faces collections action and a likely default if it goes unpaid.

Under voluntary termination, the same customer would need to pay the shortfall to £7,500 (half of £15,000) at the point of termination. The cost is £2,500 paid once, after which the customer walks away cleanly with no default. Always check VT eligibility before considering voluntary surrender.

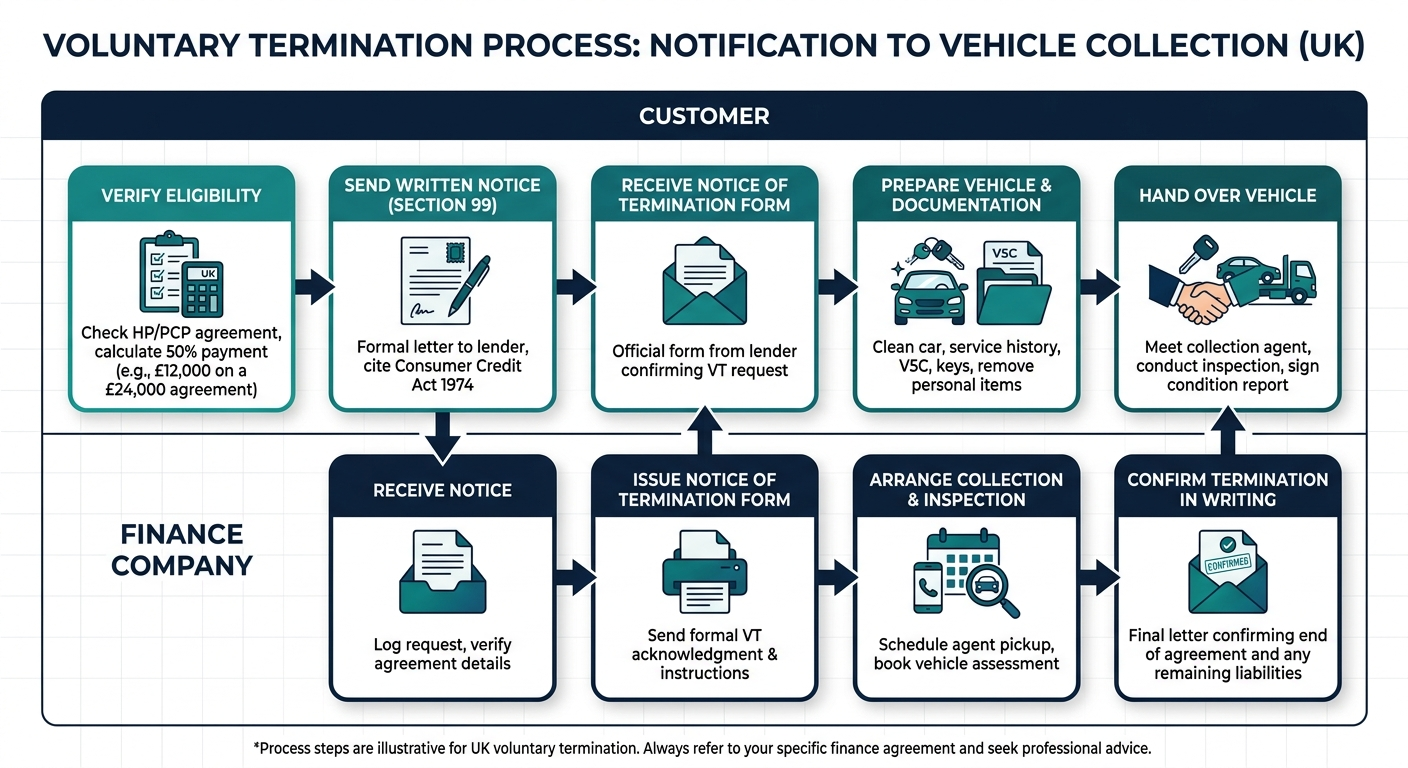

How to get out of a car finance agreement using voluntary termination: step by step

The voluntary termination process is straightforward when followed methodically. The Consumer Credit Act 1974 requires the lender to accept a valid VT notice. Every step must be documented in writing because verbal conversations carry no legal weight in dispute.

Step 1: Verify eligibility before doing anything else

Three checks confirm eligibility before contacting the finance company. The agreement must be Hire Purchase or Personal Contract Purchase, the 50% threshold must be reached, and the account must be up to date with no outstanding arrears. Request the Total Amount Payable figure in writing from the lender before relying on your own calculation.

A note on joint finance agreements and VT eligibility

Joint car finance agreements require all named parties to consent to and co-sign the voluntary termination notice. A notice signed by only one party is procedurally defective and the lender can reject it. If one party refuses to co-sign, seek legal advice from Citizens Advice before issuing the notice.

Step 2: Notify the finance provider in writing

A written notice is the legal trigger for voluntary termination. Send it by recorded delivery or by email with a sent-records screenshot. The notice period is typically one month, and the date of the written notice is the date the VT process legally begins.

The notice should contain:

- Your full name and account or agreement number

- The vehicle registration and make/model

- The date of the notice

- The phrase: "I am exercising my right to voluntarily terminate this agreement under Section 99 of the Consumer Credit Act 1974"

- A request for written confirmation of receipt and next steps

Telephone calls are not a substitute for written notice. The agreement is not legally terminated until written notice is received.

Step 3: Complete the notice of termination form

The finance company will issue a formal Notice of Termination form confirming the agreement details, any outstanding balance needed to reach the 50% threshold, and the vehicle return process. Verify every figure on the form against your own records before signing. Challenge discrepancies in writing; lenders routinely amend figures when challenged with documented evidence.

Step 4: Arrange the vehicle return and inspection

The finance company uses a third-party collection agent who arrives at an agreed location to inspect and collect the car. Document the vehicle's condition exhaustively before the inspector arrives. Take a full video walkthrough, photograph every panel from multiple angles in good light, note the mileage and fuel level, and retain the signed inspection report.

Check your eligibility - no impact on your credit score

Leave a request and our experts will contact you shortly to discuss the details.

Vehicle condition, fair wear and tear, and how to avoid hidden charges

The vehicle inspection is the stage at which most voluntary termination disputes arise. Finance companies can charge for damage beyond fair wear and tear, for excess mileage above the agreed limit, and for missing items such as the second key or service book. The industry benchmark for assessing condition is the British Vehicle Rental and Leasing Association (BVRLA) Fair Wear and Tear Guide, which most major finance companies apply.

What counts as "fair wear and tear"?

Fair wear and tear covers the normal deterioration of a vehicle through everyday use. Light scuffs, small stone chips, and minor interior wear are acceptable. Damage from neglect, abuse, or accident is not.

Acceptable fair wear and tear (BVRLA standard) includes:

- Small stone chips on the bonnet up to defined size limits

- Light scuffs and scratches that do not break the paint surface

- Minor wear to seat upholstery in high-contact areas

- Light wear on the steering wheel and gear knob

Not acceptable wear and damage includes:

- Dents larger than 25mm in diameter or multiple dents on one panel

- Scratches that have broken the paint to bare metal or primer

- Tears, burns, or stains on upholstery

- Cracked windscreens or chips in the driver's line of sight

- Kerbed or damaged alloy wheels beyond defined limits

The BVRLA guide includes photo examples and is the same standard the inspector will use.

Can a lender reject a VT request based on vehicle condition?

A lender cannot legally reject a voluntary termination request on the grounds of vehicle condition. Section 99 of the Consumer Credit Act 1974 grants the right to terminate; poor condition affects the cost of termination, not the right itself. Dispute inflated charges in writing with photographic evidence, and escalate to the Financial Ombudsman Service if the lender refuses to amend them.

Excess mileage charges and how to calculate exposure

Excess mileage charges apply when the vehicle is returned with mileage above the agreed limit. The per-mile charge is stated in the finance agreement itself; check the rate against your specific document.

Worked example: a four-year agreement with a 30,000-mile limit, returned at 38,000 miles, generates 8,000 excess miles. At a 10p per-mile rate stated in the agreement, the charge is £800.

How to protect against unfair charges before handing the car back

Contemporaneous photographic evidence is the strongest defence against inflated charges that emerge after collection.

Pre-handover protection checklist:

- Take a continuous video walkthrough of every panel, the interior, the boot, and the engine bay

- Photograph each panel from multiple angles in natural daylight

- Photograph the odometer, fuel gauge, and any warning lights

- Photograph the second key, locking wheel nut, service book, and any items being returned

- Request a signed handover receipt listing the items and the vehicle's stated condition

- Retain all documentation and records for at least six months after handover

Send copies of the documentation to the finance company by email immediately after handover.

How long does voluntary termination take?

Voluntary termination typically takes two to six weeks from written notice to vehicle collection. The Consumer Credit Act 1974 sets no fixed statutory timeframe. Monthly payments remain due until the lender issues written confirmation of termination.

If the lender has not responded within four weeks, send a written reminder citing Section 99 of the Consumer Credit Act 1974. Unreasonable delay can constitute obstruction of a statutory right. Delays beyond eight weeks without explanation can be escalated to the Financial Ombudsman Service, which is free and whose decisions bind the lender.

Does voluntary termination affect a credit score?

Voluntary termination does not register as a default on your credit file when exercised correctly. The agreement is recorded as "voluntarily terminated" or "settled," which is a visible marker but not the same as a missed payment, default, or charge-off. Credit damage from VT typically comes from arrears that preceded the termination or from unpaid damage and mileage charges left outstanding.

The three UK credit reference agencies (Experian, Equifax, and TransUnion) all record VT as a closed account with the relevant status code. Mainstream lenders applying standard scoring models distinguish between a voluntary termination and a default. Specialist subprime lenders sometimes apply tighter rules and treat any non-standard closure as a risk indicator.

What appears on a credit file after VT

A correctly processed voluntary termination appears on your credit file as a closed account marked "voluntarily terminated" or "settled" with the date of closure. The marker is visible to lenders for six years from the closure date, in line with Information Commissioner's Office guidance on credit reference reporting.

Check your credit file 30 to 60 days after the VT completes to confirm the agreement is recorded correctly. Free credit file checks are available through Experian, ClearScore, and Credit Karma. For background on how lenders interpret credit data, see what credit score is needed for car finance.

How future lenders may view a voluntary termination

Future lenders treat a voluntary termination differently depending on their underwriting approach. Mainstream lenders generally accept a single VT without significant penalty, particularly once 12 months or more have passed since the closure date. Specialist subprime lenders sometimes apply automatic decline rules for recent voluntary terminations.

Time elapsed reduces the impact substantially. Multiple VTs on a single credit file are treated more seriously than a single occurrence. Transparency on future finance applications produces better outcomes than concealment.

Voluntary termination for PCP vs. hire purchase: key differences

Voluntary termination applies to both Personal Contract Purchase and Hire Purchase under the same statutory framework. Section 99 of the Consumer Credit Act 1974 covers both. The practical mechanics differ in one area: how the balloon payment on PCP affects the 50% threshold calculation.

PCP voluntary termination: the balloon payment explained

The balloon payment on a Personal Contract Purchase agreement is the optional final lump-sum payment that buys the car outright at the end of the term. The balloon is also called the Guaranteed Future Value (GFV) and typically represents 30 to 50% of the vehicle's original price.

The balloon is included in the Total Amount Payable for calculating the 50% threshold, but the balloon itself is not part of what the customer pays to exercise VT.

Worked example: a £20,000 vehicle on PCP with £4,000 interest and an £8,000 balloon gives a Total Amount Payable of £32,000. The 50% threshold is £16,000. Once you have paid £16,000 in deposit plus monthly payments, you can voluntarily terminate, return the car, and walk away. You do not pay the £8,000 balloon.

Because PCP monthly payments are lower than HP equivalents, reaching the 50% threshold on a PCP takes more calendar months than on an equivalent HP.

Hire purchase voluntary termination: a simpler calculation

Hire Purchase agreements involve fixed monthly payments throughout the term and no balloon payment. The Total Amount Payable is the deposit plus interest plus the sum of all fixed monthly payments. The 50% threshold is half that figure.

Worked example: a £20,000 vehicle on HP with £4,000 interest over four years gives a Total Amount Payable of £24,000. The 50% threshold is £12,000. Roughly halfway through the agreement (typically month 24 of 48), the threshold is reached and VT becomes available.

HP ordinarily ends with ownership transferring to the customer after the final payment. Exercising VT means giving up that ownership option. The trade-off between the two products is covered in the HP vs PCP comparison guide.

Other ways to get out of a car finance contract

Voluntary termination is one of four common routes for ending a car finance agreement early. The others are early settlement, part exchange, and private sale with settlement.

| Option | Eligibility requirement | Credit impact | Best for | Key risk |

|---|---|---|---|---|

| Voluntary termination | 50% of TAP paid | "Voluntarily terminated" marker | Customers at or past the halfway point | Damage and mileage charges |

| Early settlement | Available anytime | None if settlement paid in full | Customers with savings or positive equity | Settlement figure may exceed market value |

| Part exchange | Available anytime | None if settled fully | Customers buying a replacement vehicle | Negative equity rolled into new agreement |

| Private sale + settlement | Available anytime | None if settled fully | Customers wanting maximum vehicle value | Selling above settlement figure required |

Early settlement: paying off the finance in full

Early settlement is the right to pay off the outstanding balance of a regulated credit agreement in a single lump sum at any point during the term. Under the Consumer Credit Act 1974, the lender must provide a settlement figure on request, and the customer is entitled to a statutory rebate of future interest under the Consumer Credit (Early Settlement) Regulations 2004.

Settlement figures are typically valid for 28 days from the date of issue. Compare the settlement figure to the vehicle's current market value before deciding. If the market value exceeds the settlement figure, paying off the finance and selling the car privately can release the surplus to the customer.

Part exchange: using the car's value against a new deal

Part exchange is the practice of trading in a financed car against a new finance agreement. The dealer obtains a settlement figure from the existing lender, settles the existing agreement, and applies any positive equity as a deposit on the new vehicle. Negative equity (where the car is worth less than the settlement figure) is typically added to the new agreement.

MoneyHelper, the government-backed money guidance service, recommends avoiding rolled-over negative equity wherever possible. Financing the depreciation gap on a vehicle you no longer own compounds the cost.

Selling the car privately to clear the finance

Private sale of a financed vehicle is permitted but requires the finance company's involvement, because the lender holds title to the car until the agreement is settled. The customer cannot legally transfer ownership without clearing the finance first.

The correct process: obtain a settlement figure from the lender, advertise and sell the car for at least the settlement amount, use the sale proceeds to settle the finance, and retain any surplus. Private sale routinely achieves more than dealer part exchange for owners who have the time to manage the process.

What if the 50% threshold cannot yet be reached?

If the 50% threshold has not been reached, four alternatives exist before considering voluntary surrender. The lender may offer a payment holiday, the agreement can sometimes be restructured to lower monthly payments, free debt advice is available from charitable services, and voluntary termination can be deferred until the threshold is reached.

Approaching the lender proactively produces better outcomes than waiting for arrears to accumulate. The Financial Conduct Authority (FCA) requires regulated lenders to treat customers in financial difficulty fairly, which often includes hardship policies that are not advertised on public-facing pages.

Voluntary surrender remains a last resort. A surrendering customer below the 50% threshold remains liable for the entire shortfall after the vehicle is sold, with a likely default registration if the shortfall goes unpaid. Customers in this position often qualify for VT within three to six months if they continue making payments and explore hardship options in the interim.

Other ways to reduce car finance costs before considering voluntary termination

Reducing the monthly cost of car finance can sometimes resolve the affordability problem that drives a VT inquiry in the first place. The Consumer Credit Act 1974 grants several rights that customers in difficulty often do not use.

Cost-reduction options to explore before VT:

- Request a payment holiday from the lender, typically one to three months with interest still accruing

- Request a term extension to lower the monthly payment by spreading the balance over more months

- Cancel optional add-on products such as GAP insurance, payment protection, or extended warranties bought with the finance

- Refinance the agreement at a lower rate if your credit score has improved since the original application

- Apply for a Breathing Space moratorium under the Debt Respite Scheme for short-term protection

A voluntary termination leaves a visible marker on the credit file for six years. For customers who can manage through alternatives, avoiding the VT marker can be the better long-term decision.

Frequently asked questions

We've collected the most popular questions about car loans from our customers

How does voluntary termination appear on a credit file to future lenders?

Voluntary termination appears on your credit file as a closed account marked "voluntarily terminated" or "settled" with the closure date. The marker is visible for six years. Mainstream lenders distinguish it from a default. Specialist subprime lenders sometimes treat any non-standard closure as a risk signal.

How does voluntary termination work with joint finance agreements?

Both named parties on a joint finance agreement must consent to and co-sign the voluntary termination notice. Unilateral VT by one party is procedurally defective and the finance company can reject it. If one party refuses to co-sign, seek legal advice from Citizens Advice before issuing the notice.

What if the 50% threshold cannot be afforded due to excess mileage or damage?

Excess mileage and damage charges are separate from the 50% threshold calculation. They are pursued as a civil debt after termination. Voluntarily terminating despite these charges is still better than voluntary surrender for most customers, because the underlying agreement closes as terminated rather than defaulted.

What are the consequences of not meeting the voluntary termination conditions?

Failing to pay the 50% threshold or returning the vehicle in poor condition triggers additional liability. The lender can pursue the shortfall as a civil debt and may register a default if unpaid. Returning the car early without meeting Section 99 conditions converts the process into voluntary surrender.

How long does voluntary termination take?

Voluntary termination typically completes within two to six weeks of the written notice. The Consumer Credit Act 1974 sets no fixed timeframe. Continue paying monthly installments until written confirmation of termination is received. Delays beyond eight weeks without explanation can be escalated to the Financial Ombudsman Service.

What is a notice of termination for car finance?

A Notice of Termination is the formal document a finance company issues confirming that a voluntary termination request has been accepted. The notice states the outstanding balance to reach the 50% threshold and the vehicle return process. Verify all figures against your own records before signing.

What documentation should be kept during the voluntary termination process?

Retain the written VT notice, the lender's Notice of Termination, all payment records, the signed handover receipt, and the pre-handover video and photographs of the vehicle. Keep all records for at least six months. Disputes about damage and mileage charges sometimes arise weeks after collection.

What is the legal basis for voluntary termination in the UK?

Section 99 of the Consumer Credit Act 1974 grants the statutory right to voluntarily terminate a regulated Hire Purchase or Personal Contract Purchase agreement. Section 100 of the same Act caps the customer's liability at 50% of the total price plus any installments already accrued and reasonable damage costs.

Can a hire purchase agreement be voluntarily terminated?

Yes. Hire Purchase agreements are regulated by the Consumer Credit Act 1974 and qualify for voluntary termination under Section 99. The customer must have paid 50% of the Total Amount Payable, return the vehicle in reasonable condition, and submit written notice citing the relevant statute.

Can a personal contract purchase agreement be voluntarily terminated?

Yes. Personal Contract Purchase agreements qualify for voluntary termination under Section 99 of the Consumer Credit Act 1974. The balloon payment is included in the Total Amount Payable for threshold calculation but does not need to be paid to exercise VT.

What is the voluntary termination clause?

The voluntary termination clause is the section of a car finance agreement that mirrors the statutory VT right granted by Section 99 of the Consumer Credit Act 1974. The clause restates the 50% threshold and the customer's right to end the agreement. A contractual clause cannot reduce the statutory right.

Does voluntary termination include the deposit in the 50% calculation?

Yes. The deposit paid at the start of the agreement counts towards the 50% threshold. Adding the deposit to total monthly payments gives the figure that is compared against half of the Total Amount Payable. Many customers underestimate eligibility by overlooking the deposit.

How much does voluntary termination cost overall?

The cost of voluntary termination is the gap between payments made and 50% of the Total Amount Payable, plus any reasonable damage charges and excess mileage. Customers already at the threshold pay only damage and mileage. Customers below the threshold pay the shortfall plus any charges.

What are the alternatives to voluntary termination near the end of a finance agreement?

Near term end, early settlement or completing remaining payments often produces a better outcome than VT. Settlement preserves the option of keeping or privately selling the car. Voluntary termination surrenders the vehicle and the equity it represents. Compare settlement figure to market value before deciding.

Does voluntary termination affect a car insurance policy?

Voluntary termination ends the lender's interest in the vehicle, which means the lender is removed from the insurance policy as an interested party. Inform the insurer in writing on the date the vehicle is returned. The policy can then be transferred to a replacement vehicle or cancelled, with any pro-rata premium refunded.

How does voluntary termination compare to other ways to end car finance?

Voluntary termination is the only statutory right that caps liability at 50% of the Total Amount Payable. Early settlement requires paying the full balance. Part exchange typically rolls negative equity into a new agreement. Private sale releases maximum value but requires the sale price to exceed the settlement figure.

This information is for guidance only and does not constitute legal or financial advice. For advice specific to your circumstances, contact your lender directly, Citizens Advice, or seek independent legal advice. Car-Finance.co.uk is not a claims management company or a debt advice service.

Car-Finance.co.uk is a trading name of Moneyrepublic Ltd (Company No. 12141408). Moneyrepublic Ltd is an Appointed Representative of F&I Online Ltd (FCA No. 731217), which is authorised and regulated by the Financial Conduct Authority. Car-Finance.co.uk acts as a credit broker, not a lender. Representative 23.9% APR.

Check your eligibility — no impact on your credit score

Leave a request and our experts will contact you shortly to discuss the details.

Author

Roman Danaev is a UK car finance specialist with over a decade in the motor finance industry. He has helped thousands of customers find the right finance deal — from standard HP and PCP agreements to bad credit and no-guarantor options. Roman writes practical, jargon-free guides to help UK drivers make informed borrowing decisions.