Car finance vs personal loan: which option actually saves you more money?

Car finance and a personal loan both get you into a car, but they differ on ownership. With car finance, the lender owns the car until you finish paying. With a personal loan, you own the car from day one and borrow the cash unsecured.

The cheaper option depends on your credit score. Excellent credit often beats car finance with a sub-7% personal loan. Poor or thin credit usually finds car finance more accessible, and car finance can offer 0% manufacturer deals. This guide compares both products on cost, ownership, credit, and consumer protection, using verified 2026 UK market data.

Key takeaways

- Car finance lets the lender hold the car as collateral, so approval is easier on poor credit than an unsecured personal loan.

- A personal loan gives you full ownership from day one, with no mileage limits or repossession risk.

- Your credit score sets the interest rate on both products.

- Car finance usually needs about a 10% deposit; a personal loan needs none.

- A personal loan often wins on cost for excellent credit; car finance wins for average credit or 0% deals.

What is car finance?

Car finance is a secured lending category covering several vehicle-specific products, where the lender holds the car as collateral until the agreement ends. The two most common products are hire purchase (HP) and personal contract purchase (PCP).

A car dealership or a credit broker arranges most agreements. Everyday use of the phrase "car finance" is loose, which causes genuine confusion. In this guide it means a secured agreement where the vehicle acts as collateral.

Hire purchase (HP)

Hire purchase ends in guaranteed ownership once you make the final payment. You pay a deposit, then fixed monthly payments across the term. Most HP terms run 12 to 60 months, with deposits commonly around 10% of the car value. The car stays the lender's collateral until you clear the balance. The interest rate applies to the full amount financed, so a larger deposit or lower rate cuts the total you repay. A small option-to-purchase fee, often around £10, transfers ownership at the end.

Personal contract purchase (PCP)

Personal contract purchase lowers monthly payments by financing the car's depreciation rather than its full value. PCP monthly payments cover the gap between the car's price and its predicted end value. That final figure is the balloon payment, or Guaranteed Minimum Future Value (GMFV).

The car acts as the lender's collateral until you settle the balloon. The interest rate applies to the depreciation you finance, not the full car value, so a low monthly payment still carries cost. At the end of the term, you choose one of three options:

- Return the car to the lender and walk away, subject to mileage and condition limits.

- Pay the balloon payment (the GMFV) to own the car outright.

- Part-exchange any equity in the car toward a new PCP agreement.

Excess mileage charges on PCP often run to around 30p per mile, set out in your agreement. PCP suits drivers who change cars every 2 to 4 years and plan for the balloon.

Personal contract hire (PCH) and car leasing

Personal contract hire is the "never own" option, where you pay fixed monthly amounts to use the car and return it at the end. The leasing company holds the car as collateral throughout, so ownership never passes to you.

PCH carries strict mileage limits, condition requirements, and a ban on modifications. Leasing is not automatically the cheapest route, because deposits and excess mileage charges add to the total. PCH suits drivers who want a new car every few years and accept that they will never own it.

What is a personal loan for a car?

A personal loan for a car is an unsecured lump sum from a bank or building society that you use to buy the vehicle outright. You own the car from day one, and the car never secures the debt. The interest rate reflects the lender's risk without collateral, so rates run from around 6% for excellent credit to 30% or more for poor credit.

Most UK personal loans run from £1,000 to £25,000 over 1 to 7 years, regulated under the Consumer Credit Act 1974. A personal loan also turns you into a cash buyer, so you can buy from any seller, including a private seller, and negotiate on price.

How do repayments work for car finance and personal loans?

Both products use fixed monthly payments over a set term, but what each payment covers differs. A personal loan and a hire purchase agreement reduce the full capital balance each month. By the end, you have cleared the entire purchase value plus interest.

Personal contract purchase works differently. PCP monthly payments cover only the car's depreciation, and the balloon payment stays outstanding until you settle it. This is why a lower PCP monthly payment does not mean a cheaper deal. Here is what your monthly payment covers:

- Personal loan: a slice of the full price, plus interest, until the balance reaches zero.

- Hire purchase: a slice of the full car value, plus interest, ending in ownership.

- Personal contract purchase: depreciation only, plus interest, with the balloon left to settle.

Car finance vs personal loan: the core differences at a glance

Car finance and a personal loan both put you behind the wheel, but their structural differences carry real, lasting consequences. Ownership, deposit, mileage rules, and the freedom to sell early all change depending on which product you choose.

A personal loan opens access to private sellers and makes you a cash buyer. Car finance is usually arranged through a car dealership or a credit broker, and the lender holds the car as collateral. The table below sets out the decision-critical factors side by side, so you can match each one to your situation.

| Factor | Car finance (HP / PCP) | Personal loan |

|---|---|---|

| Car ownership during repayment | Lender owns until final payment | You own from day one |

| Deposit | Usually around 10% | None required |

| Monthly payment structure | Capital plus interest (HP); depreciation plus interest (PCP) | Capital plus interest |

| Mileage restrictions | Yes on PCP and PCH | None |

| Sell the car early | Only after settling the finance | Anytime, you own it |

| End-of-term outcome | Own (HP), or return, buy or swap (PCP) | Loan ends, you keep the car |

| Credit score needed | Accessible with poor or thin credit | Best rates need good to excellent credit |

| Secured or unsecured | Secured on the car | Unsecured |

| Typical APR range (2026) | From 9.9% APR, Representative 23.9% APR | From around 5.4% to 30%+ by credit tier |

| Who you can buy from | Dealers, plus brokers' lender panels | Any seller, including private |

| Insurance | Highest cover tier usually required | Your choice, highest tier advised |

See which lenders may accept you, soft search only. Compare your personalised car finance and personal loan rates. Checking your eligibility uses a soft credit search and does not affect your credit score. If you proceed to a formal application, a full credit search will be carried out by the lender.

We receive a commission from lenders when we arrange finance on your behalf. This does not affect the rate you are offered. Learn more about how we make money.

Do you need a deposit for car finance or a personal loan?

A personal loan requires no deposit, while car finance usually requires an upfront deposit of around 10% of the car value. The personal loan funds the full purchase price as one lump sum, so you hand no money to a dealer at the point of purchase. Deposit size directly affects what you pay on car finance.

A larger deposit cuts the amount financed, which lowers both the monthly payment and the total interest. Zero-deposit car finance exists, but lenders attach a higher interest rate to offset the larger balance. Many buyers overlook the deposit requirement and feel caught out at the dealership, so plan it before you start.

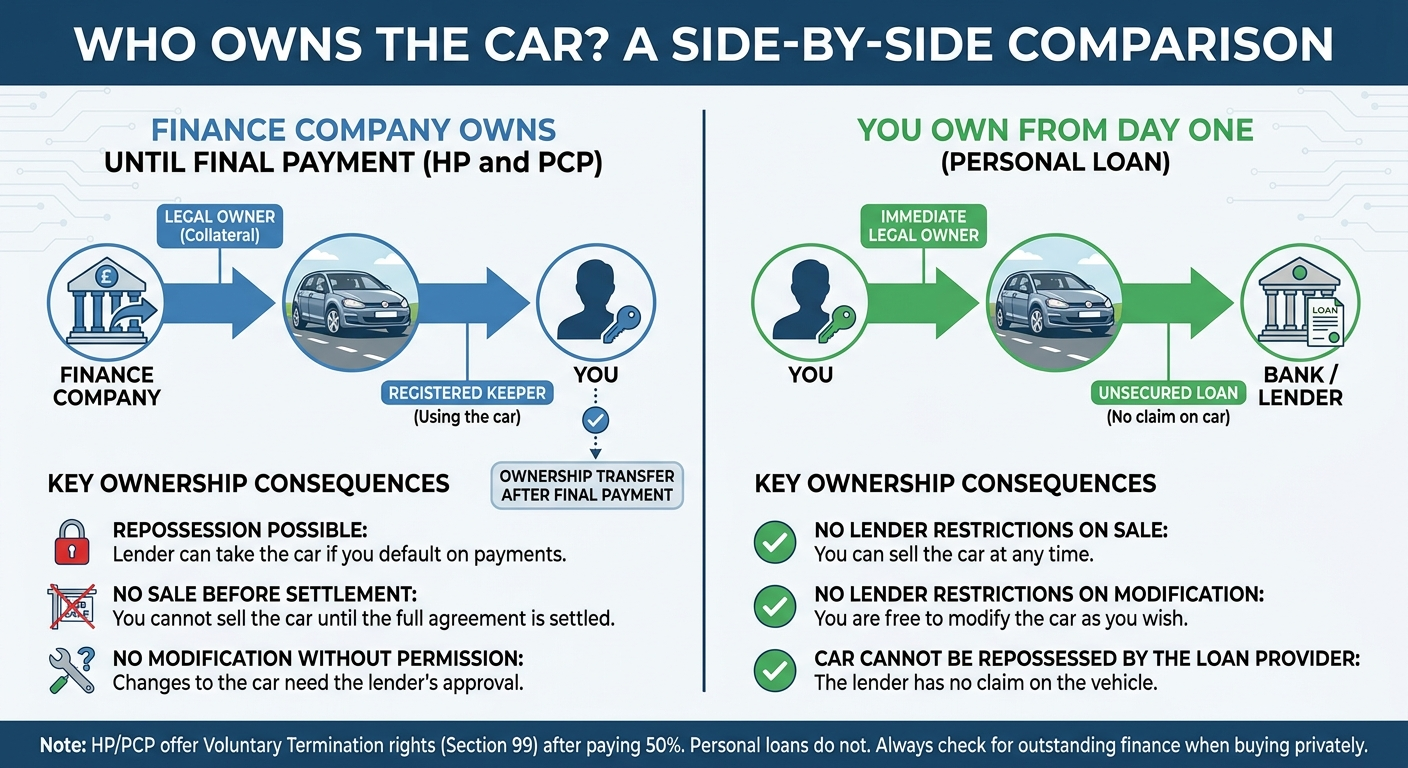

Who actually owns the car, and why it matters more than you think

With hire purchase and personal contract purchase, the finance company legally owns the car until the final payment clears. The car is the lender's collateral, which is why ownership stays with the lender. With a personal loan, you own the car from day one and the lender has no claim on it.

Lender ownership during car finance carries three consequences. The finance company can repossess the car if you default. You cannot sell the car until you settle the agreement. Modifying the car also needs the lender's permission.

On a regulated HP or PCP agreement, Section 99 of the Consumer Credit Act 1974 grants a voluntary termination right. You can return the car and end the deal once you have paid at least 50% of the total amount payable. The Financial Conduct Authority oversees this protection, and a personal loan carries no equivalent right.

When buying privately with a personal loan, run an outstanding-finance check first. A car with finance still owed against it can be repossessed. Negative equity is a real PCP risk, where the car is worth less than the balloon payment owed.

How does your credit score affect which option you can get?

Your credit score decides both your eligibility and your interest rate, and it works differently for each product. A personal loan is unsecured, so banks apply stricter criteria and reserve their best rates for good-to-excellent profiles. Car finance is secured on the car, so lenders carry less risk and can approve thinner or imperfect histories.

Applying to several lenders at once leaves multiple hard searches on your file, which can lower your score. Use a soft-search eligibility tool first, which shows your likely rate without affecting your credit score. A full credit search will be carried out if you proceed to a formal application. Specialist bad credit car finance helps borrowers banks reject, though the higher rate raises total cost.

Interest rates climb sharply as credit quality falls. The average £10,000 personal loan cost around 6.9% APR in Q1 2026, per Bank of England quoted rates. The tiers below show the spread:

- Excellent credit: personal loans from around 5.4% APR.

- Average credit: personal loans of roughly 8% to 12% APR.

- Poor or subprime credit: 15% to 30% APR or more.

- Car finance: rates from 9.9% APR, Representative 23.9% APR, across wider credit profiles.

Full eligibility requirements for car finance and personal loans

Both products share core eligibility checks, while car finance adds requirements tied to the vehicle itself. Lenders assess your age, residency, income, employment, and credit history before approving either product. Shared requirements for both car finance and a personal loan include:

- Minimum age of 18, with most lenders preferring applicants aged 21 or over.

- Proof of UK residency, usually three years of address history.

- Proof of income and stable employment or self-employment records.

Car finance adds requirements that a personal loan does not:

- Vehicle age limits, often a maximum age at the end of the term.

- Mileage limits on the car at the point of purchase.

- A condition or roadworthiness standard the car must meet.

Self-employed applicants face extra scrutiny on income, often needing two to three years of accounts. Your debt-to-income ratio matters as much as your credit score.

Understanding your debt-to-income ratio

Your debt-to-income ratio is your total monthly debt payments divided by your gross monthly income, and lenders use it to judge affordability. A lower ratio signals room in your budget for new debt, which improves both your approval odds and your interest rate on car finance and personal loans. The ratio explains why some buyers with strong credit scores still get declined. A high credit score shows you repay debt, but a high debt-to-income ratio shows little room for more. Check your existing commitments before you apply to either product.

Total cost of borrowing: which option is actually cheaper?

APR alone does not decide which product is cheaper, because the total amount repayable is what counts. A lower APR on a higher car price can cost more than a higher APR on a lower price. Car finance is secured on the car as collateral, while a personal loan is unsecured, which is why their APR profiles differ. The balloon payment in a PCP agreement conceals costs that the monthly figure never reflects. The worked example below finances a £15,000 used car over 48 months.

| Product | Deposit | Monthly payment | Total repayable | Cost of borrowing |

|---|---|---|---|---|

| Personal loan (6.9% APR) | £0 | £358.50 | £17,208 | £2,208 |

| Hire purchase (9.9% APR) | £1,500 | £341.75 | £17,914 | £2,914 |

| PCP if you buy (9.9% APR) | £1,500 | £247.89 | £18,909 | £3,909 |

These figures are illustrative. Car finance rates start from 9.9% APR, with a Representative 23.9% APR, subject to status. On these figures, the personal loan costs around £706 less than HP and £1,701 less than PCP if you buy the car. Run the numbers with a car finance calculator before you commit.

When a personal loan works out cheaper

A personal loan delivers the lowest total cost when you hold an excellent credit score and qualify for a sub-7% APR. At 6.9% APR on the £15,000 example, the personal loan saves around £706 against HP over 48 months. You also act as a cash buyer, which can cut the car price itself.

Buying from a private seller multiplies that advantage, because you skip the car dealership and negotiate directly. High-mileage drivers also benefit, because a personal loan avoids the excess mileage charges that PCP applies. This profile of excellent credit, a market-rate or private-sale car, and cash-buyer bargaining power applies to a minority of buyers.

When car finance works out cheaper

Car finance wins on total cost most clearly through a manufacturer-subsidised 0% APR deal, which no personal loan can beat. Personal contract purchase delivers this best on new cars. A 0% or low manufacturer rate, paired with the depreciation-only payment structure, can undercut any personal loan for drivers who swap cars often.

Hire purchase wins on predictable long-term ownership, where a fixed rate from 9.9% APR and no balloon can beat a higher personal loan quote over the full term. Dealer pricing can also make car finance cheaper, because a lower purchase price offsets a slightly higher APR. Buyers who cannot access competitive personal loan rates usually find car finance cheaper overall. Always get a personalized quote from both before you compare.

Are there different insurance requirements for car finance and a personal loan?

UK law requires car insurance for every driver, whatever the financing method, but car finance adds a contractual condition. Car finance agreements usually require the highest level of cover, which protects the car against accidental damage, fire and theft, because the lender owns the car as collateral. A personal loan borrower chooses their own cover, though the highest tier remains the sensible choice.

Choosing a cheaper third-party policy on a financed car risks breaching your finance terms without realising it. Finance lenders set this condition within the regulated framework the Financial Conduct Authority oversees. Bundled insurance from a finance provider can cost more than a standalone policy, so compare prices independently before you accept.

Pros and cons of car finance

Car finance offers easier approval and lower upfront cost, but the lender owns the car and restrictions apply.

Advantages of car finance:

- Wider access for lower credit scores, because the car secures the debt.

- Lower upfront cost, with deposits commonly around 10%.

- Fixed monthly payments that make budgeting predictable.

- Access to newer cars and manufacturer rates as low as 0% APR.

- Voluntary termination rights on HP and PCP after paying 50%, set out in the Consumer Credit Act 1974 and overseen by the Financial Conduct Authority.

Disadvantages of car finance:

- The lender owns the car until you make the final payment.

- Mileage limits and condition charges apply on PCP and PCH.

- Total cost can exceed a personal loan for excellent-credit borrowers.

- Negative equity is a real PCP risk when the balloon exceeds the car's value.

- The highest tier of insurance cover is usually mandatory.

Pros and cons of a personal loan for a car

Banks and building societies are the main source of personal loans for a car. A personal loan gives full ownership but demands stronger credit and higher monthly payments.

Advantages of a personal loan:

- Full ownership of the car from day one, with no lender claim.

- No mileage limits and no usage or modification restrictions.

- Freedom to buy from any seller, including private sellers a dealership cannot offer.

- Cash-buyer bargaining power that can lower the car price.

- No repossession risk from a car finance company.

Disadvantages of a personal loan:

- Stricter credit score requirements, with the best rates needing a good to excellent score.

- Higher monthly payments, since you repay the full price, not just depreciation.

- No option to hand the car back, so your only exit is selling it, while hire purchase allows voluntary termination after paying 50%.

- Full responsibility for depreciation and maintenance.

- No access to manufacturer-subsidised rates such as 0% APR.

How to decide which option is right for you

Start with your credit score reality, not the ideal scenario, because the best option means nothing if you cannot access it. Run a soft-search eligibility check first, which shows your likely rate without affecting your credit score. A full credit search will be carried out if you proceed to a formal application. Work through these six criteria in order:

- Credit score: excellent credit makes a personal loan competitive, while average or fair credit makes car finance more accessible.

- Deposit: little saved points to car finance, while a substantial deposit suits either product.

- Ownership: wanting the car immediately favours a personal loan, while deferred ownership or regular swaps favours car finance.

- Annual mileage: high mileage favours a personal loan to avoid PCP excess charges, while average mileage works with either.

- Seller type: a private seller needs a personal loan, while a dealership opens both options.

- Flexibility: changing cars every 2 to 3 years suits PCP, while keeping a car 5 years or more suits HP or a personal loan.

Check your debt-to-income ratio before you apply, because affordability decides approval as much as your credit score.

Common mistakes to avoid when choosing car finance or a personal loan

The costliest mistake is comparing APR in isolation while ignoring the total amount repayable and end-of-term costs. The six errors below catch buyers out most often.

- Comparing APR alone: the total amount repayable and the PCP balloon decide real cost, not the headline rate.

- Applying to many lenders at once: multiple hard searches damage your credit score, so use soft searches first.

- Underestimating the PCP balloon: entering a PCP without a plan for the GMFV leaves you short at the end.

- Ignoring mileage caps: excess mileage charges of around 30p per mile add up fast on PCP.

- Skipping the outstanding-finance check: buying a used car with finance still owed risks repossession.

- Chasing low monthly payments: stretching the term lowers the payment but raises the total interest.

Mistake five causes the most distress, yet an outstanding-finance check from around £10 to £20 prevents it. The Financial Conduct Authority regulates the framework these risks sit within, but the checks remain your responsibility.

Frequently asked questions

We've collected the most popular questions about car loans from our customers

Is it better to take a loan or finance a car?

A personal loan is usually cheaper if your credit score is excellent and you qualify near 6.9% APR. Car finance is usually better for average or poor credit, or for a 0% manufacturer deal. Compare personalised quotes from both before deciding.

What are the key differences between car finance and personal loans?

Car finance is secured on the car, so the lender owns it until the final payment. A personal loan is unsecured, so you own the car from day one. Car finance usually needs a deposit; a personal loan does not.

How to decide which option is best for you?

Start with your credit score, then weigh deposit, ownership, mileage, and seller type. Excellent credit and a private sale favour a personal loan. Average credit, a small deposit, or a 0% dealer deal favour car finance. Check both rates first.

What are the pros and cons of car finance?

Car finance approves wider credit profiles, needs a smaller upfront deposit, and can offer 0% manufacturer rates. The drawbacks are lender ownership until the final payment, PCP mileage limits, negative equity risk, and usually mandatory top-tier insurance cover on the financed car.

What are the pros and cons of personal loans for buying a car?

A personal loan gives day-one ownership, no mileage limits, and freedom to buy from a private seller. The drawbacks are stricter credit requirements, higher monthly payments covering the full price, no hand-back option, and no access to subsidised manufacturer rates.

Important information

Car-Finance.co.uk is a trading name of Moneyrepublic Ltd (Company No. 12141408). We are an Appointed Representative of F&I Online Ltd (FCA No. 731217), which is authorised and regulated by the Financial Conduct Authority. We are a credit broker, not a lender. Rates from 9.9% APR. Representative 23.9% APR, subject to status. We receive a commission from lenders when we arrange finance on your behalf. This does not affect the rate you are offered. Learn more about how we make money.

Check your eligibility — no impact on your credit score

Leave a request and our experts will contact you shortly to discuss the details.

Author

Roman Danaev is a UK car finance specialist with over a decade in the motor finance industry. He has helped thousands of customers find the right finance deal — from standard HP and PCP agreements to bad credit and no-guarantor options. Roman writes practical, jargon-free guides to help UK drivers make informed borrowing decisions.