PCP vs HP Car Finance: Which Deal Actually Saves You Money?

At the dealership, two finance products decide your costs: Personal Contract Purchase (PCP) and Hire Purchase (HP). The Finance & Leasing Association reports that approximately 80% of new cars in the UK are bought on finance as of 2026. Сhoosing wrong between PCP and HP can cost a driver thousands of pounds. This guide compares both car finance options so you pick the cheaper deal.

What Is PCP Finance? (Personal Contract Purchase Explained)

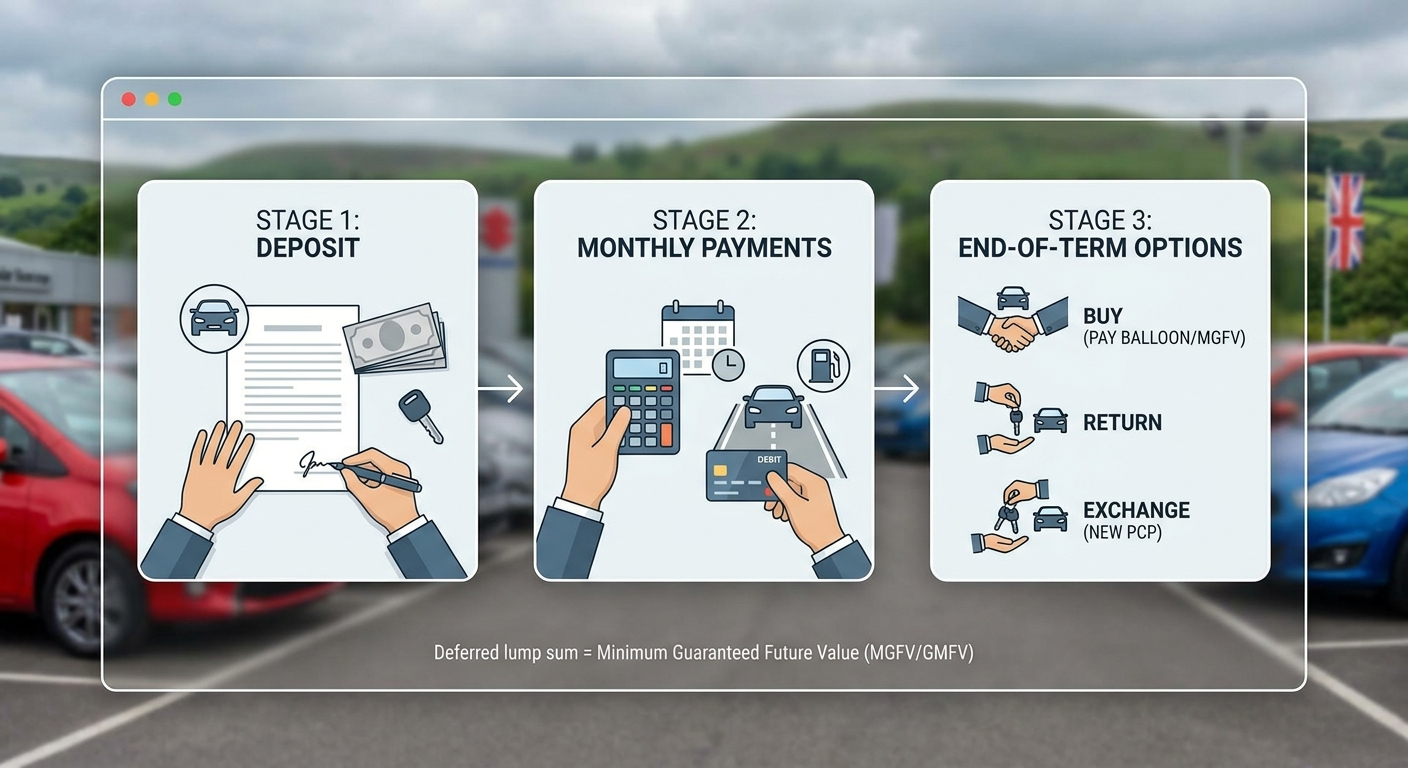

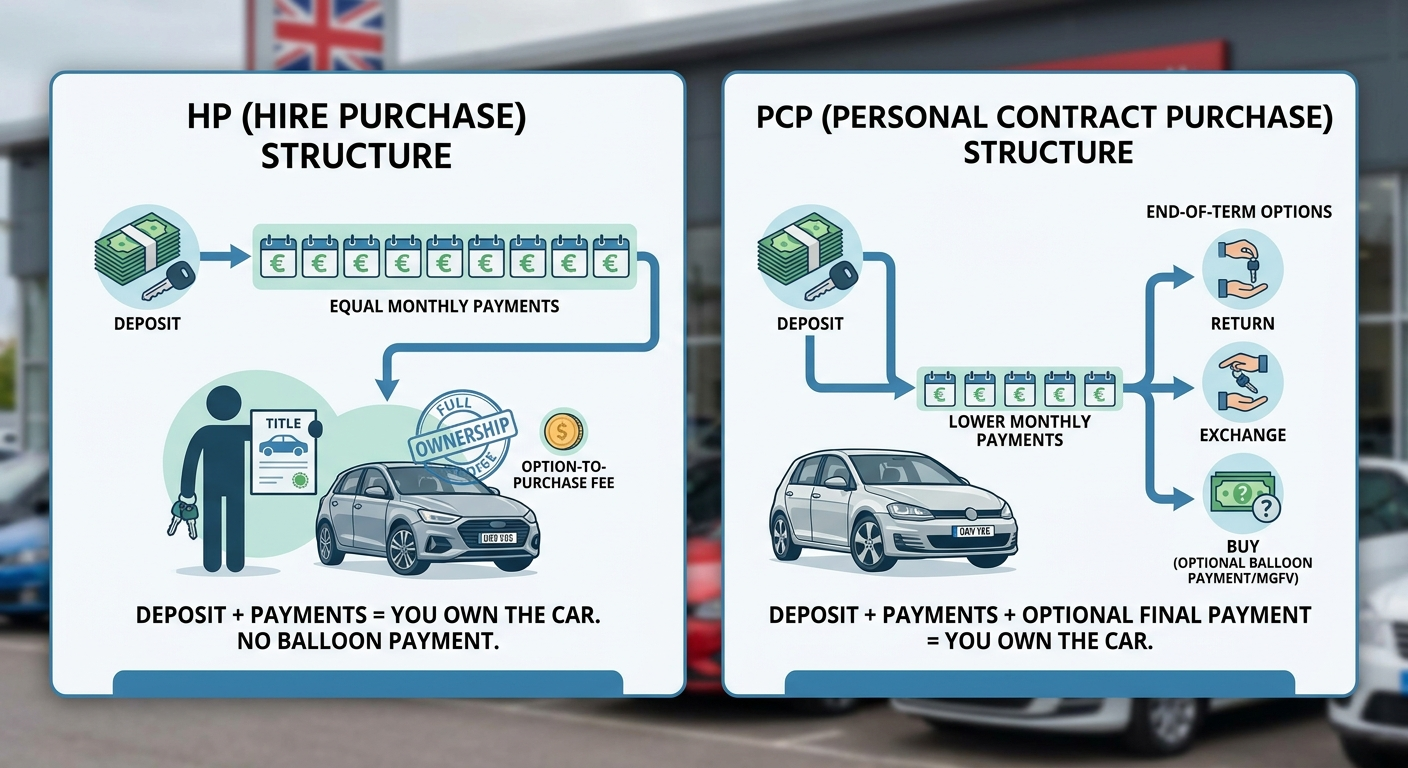

Personal Contract Purchase (PCP) is a car finance agreement where the driver pays for a car's depreciation, not its full price. PCP has three parts: a deposit, monthly payments, and an end-of-term choice. The deferred lump sum is the Minimum Guaranteed Future Value (MGFV). PCP works like renting a flat, then deciding whether to buy at the end.

How Does the Balloon Payment Work in PCP?

The balloon payment equals the lender's forecast of the car's value at contract end, the MGFV. Monthly payments cover only the gap between today's price and that future value. On a £30,000 car with a £22,000 MGFV, payments cover the £8,000 depreciation. The £22,000 balloon falls due only if the driver chooses to keep the car.

Three factors set the size of a PCP balloon payment:

- Agreed annual mileage shapes the forecast residual value.

- Contract length changes how much value the car loses.

- Trim and specification affect the car's resale demand.

How Does MGFV Protect and Expose the Buyer?

The MGFV acts as a financial floor for the PCP driver. If the car's market value falls below the MGFV at handback, the lender absorbs that loss, not the driver. The MGFV also caps any upside equity the driver could otherwise access. Drivers who took PCP on electric vehicles in 2021 to 2022 learned a hard lesson: MGFV protection applies only on handback, not on purchase.

What Are the Options at the End of a PCP Contract?

A PCP contract ends with three core choices, plus refinancing as a fourth path:

- Pay the balloon payment — equal to the MGFV, the lender's pre-agreed minimum value for the car's return — and own the car outright.

- Hand the car back and walk away with no further payment.

- Use any positive equity as a deposit toward a new PCP deal.

Refinancing the balloon spreads it as a separate loan, which avoids a single lump sum. Voluntary termination is a statutory right at 50% repayment under Section 99 of the Consumer Credit Act 1974. Drivers who took PCP on electric vehicles at 2021 to 2022 prices may find zero equity today.

To explore how PCP monthly payments could work, check your eligibility via PCP car finance. The soft check leaves no impact on your credit score.

What Is Hire Purchase (HP) Finance? (HP Explained Simply)

Hire Purchase (HP) is a car finance agreement covering the full car price minus deposit. The driver repays in fixed monthly instalments, and legal ownership transfers automatically once the final payment clears. HP carries no balloon payment, no mileage limits, and no end-of-term condition check. HP repays like a mortgage, with each instalment building toward full ownership.

How Are HP Monthly Payments Calculated?

HP monthly payments equal the car price minus deposit, divided across the term, plus interest at the agreed APR. A £20,000 car with a £4,000 deposit over four years at an illustrative 5% APR costs about £368 per month. HP APR typically ranges from 4% to 13% depending on lender, credit profile, and vehicle. A driver's credit score directly shapes the APR offered. Checking a credit report before applying helps secure a lower rate. Car-Finance.co.uk rates start from 9.9% APR (representative 23.9% APR).

What Fees Apply to HP Agreements?

HP agreements can carry three fees beyond payments and interest. An arrangement fee at signing is often added to the financed amount, where it accrues interest across the full term. The option-to-purchase fee of £1 to £10 falls due at the end. Early repayment fees can apply. Lenders must provide a full written fee breakdown before signing under the Consumer Credit Act 1974.

To see how HP monthly payments fit your budget, check eligibility via HP car finance. The check uses a soft credit search only.

PCP vs HP Finance: The Core Differences Compared

PCP and HP both offer manageable monthly payments, yet they create very different financial commitments. The table below shows the core differences before the detailed analysis.

| Feature | PCP | HP |

|---|---|---|

| Monthly payments | Lower | Higher |

| Balloon payment | Yes (large) | No |

| Automatic ownership | No | Yes |

| Mileage limits | Yes | No |

| Condition penalties | Yes | No |

| Equity building | Slower, less predictable | Faster, predictable |

| Early Exit Flexibility | Moderate | Moderate |

| Best for | Frequent car changers | Long-term and high-mileage drivers |

Monthly Cost and Total Cost of Finance (Car Finance PCP vs HP)

PCP shows a lower monthly payment than HP, because the MGFV defers a portion of the car's value to contract end, reducing the amount covered in monthly installments. Yet a lower monthly cost rarely means a lower total cost. The lower PCP payment is its main marketing advantage, not the full financial picture. Once the balloon payment joins the total amount repayable, PCP often costs more than HP for the same car. On a £25,000 car with the same deposit, term, and APR, HP usually wins on the total amount repayable. Manufacturer 0% APR PCP deals exist, yet each one deserves close scrutiny.

Can Buyers Access a 0% Finance Deal on PCP or HP?

A 0% APR deal exists on both PCP and HP, though it depends on strict conditions. A 0% deal typically requires a strong credit profile, a larger deposit, or a shorter term. Each condition raises the monthly payment. The car's list price may also stay less negotiable on a 0% offer. Manufacturer-backed PCP carries 0% more often than HP does. A negotiated cash discount plus a low arranged APR can beat a headline 0% deal on total cost.

Car Ownership: Who Legally Owns the Vehicle?

Under HP, the driver builds equity from the first payment and owns the car outright after the final payment. Under PCP, the finance company legally owns the car throughout the contract, so the driver is a hirer. A PCP driver cannot sell the car during the contract without first settling the finance. Modification rights, private sale rights, and use as collateral all differ between the two products.

Mileage Limits and Excess Charges on PCP

HP sets no mileage restrictions. PCP sets a fixed mileage allowance, typically 6,000 to 12,000 miles per year. The cap protects the MGFV's residual value forecast. Exceeding the limit triggers charges, typically in the range of 7p to 15p per mile.

Three steps help a driver manage mileage on a PCP agreement:

- Track mileage quarterly against the agreed annual allowance.

- Negotiate a realistic, slightly generous allowance before signing.

- Buy extra miles at contract start rather than paying excess at the end.

Condition Requirements and End-of-Term Charges

PCP lenders require the car returned within fair wear and tear, because its residual value underpins the MGFV. Damage beyond that standard is charged at handback, assessed against the BVRLA fair wear and tear guide. The BVRLA reports that approximately 1 in 5 PCP returns in the UK incurs a condition-related fee.

HP carries no such clause, because the car's condition is the owner's own concern. Some PCP contracts also require servicing within an authorised dealer network to protect the MGFV. A driver should check the maintenance terms in the small print before signing.

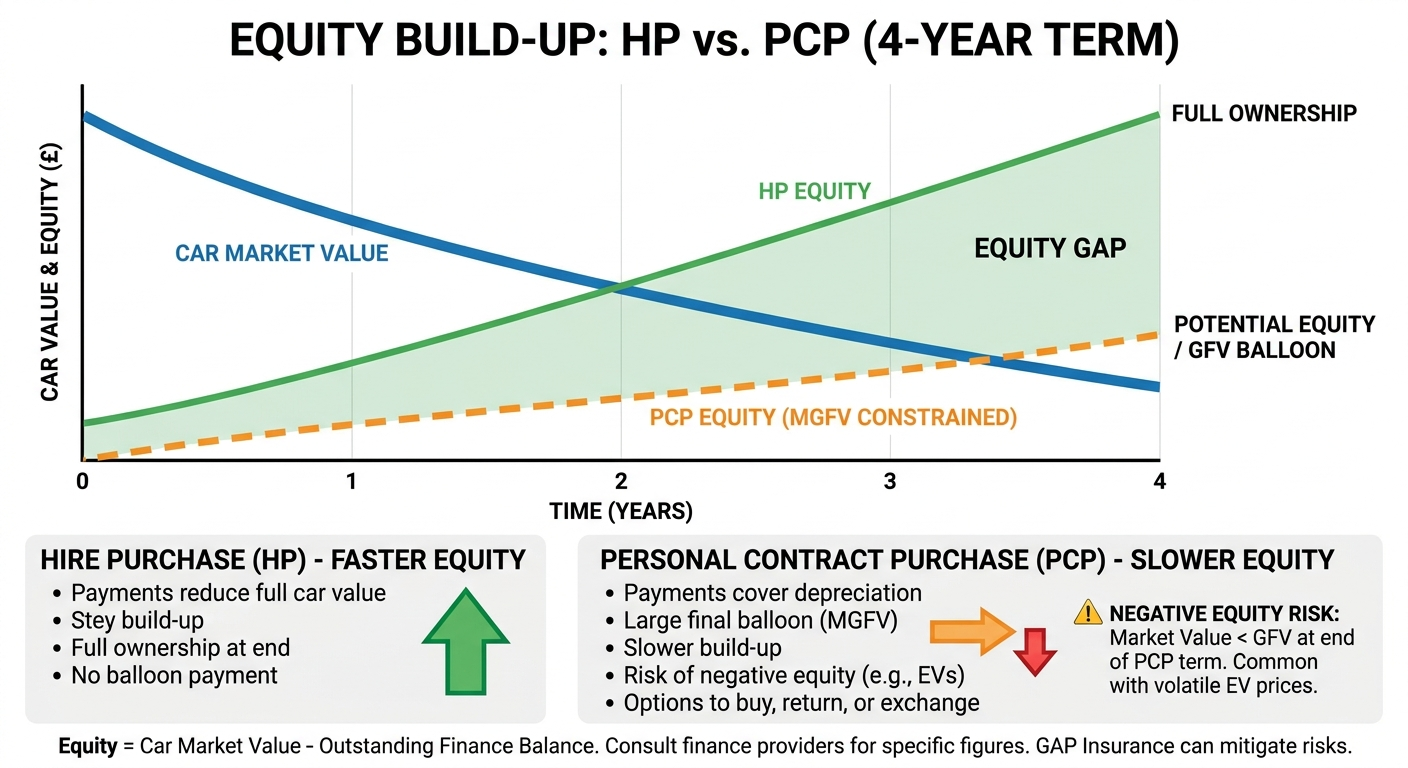

Equity, Negative Equity and Implications for Changing Cars

Equity is the difference between the car's current market value and the outstanding finance balance. HP builds equity steadily, because every payment reduces the full car value. PCP builds equity slowly, because the MGFV constrains equity build-up by deferring a fixed portion of the car's value to the balloon; equity cannot exceed the gap between market value and MGFV until the balloon is paid, so negative equity can result.

Drivers on PCP electric vehicles at 2021 to 2022 prices face negative equity in 2026 as values corrected sharply. GAP insurance can mitigate this risk. Request a settlement letter and a market valuation through a free tool such as Autotrader's valuation service.

GAP Insurance and Why It Matters for PCP and HP Buyers

GAP (Guaranteed Asset Protection) insurance covers a shortfall after a write-off or theft. The shortfall is the gap between a standard insurer's payout and the finance balance. A standard car insurance policy pays only the car's current market value. That value can sit below the amount still owed, including any balloon. A £20,000 car worth £15,000 after 12 months, but with £17,000 owed, leaves a £2,000 shortfall that GAP insurance covers. GAP cover matters most in the early stages of a PCP contract, when the balloon is fully outstanding. UK first-year depreciation runs around 15% to 35%.

PCP vs HP Real-World Examples with Numbers

The figures below compare PCP and HP on the same car using identical assumptions. Both examples assume a £28,000 car, a £2,800 deposit, a four-year term, and an illustrative 7% APR. In the PCP column, the balloon payment represents the MGFV — the lender's pre-agreed guaranteed future value for the car at contract end.

| Item | PCP | HP |

|---|---|---|

| Car price | £28,000 | £28,000 |

| Deposit (10%) | £2,800 | £2,800 |

| Monthly payment | approx. £330 | approx. £605 |

| Balloon payment | approx. £15,000 | None |

| Total amount repayable | approx. £33,700 | approx. £31,800 |

| Own the car at end? | Optional, after the balloon | Yes, after the final payment |

| Mileage limit? | Yes, 10,000 per year | No |

HP costs around £2,000 less than PCP for a driver who keeps the car. The same pattern holds on a smaller £20,000 car. Figures are illustrative, and actual rates start from 9.9% APR with Car-Finance.co.uk.

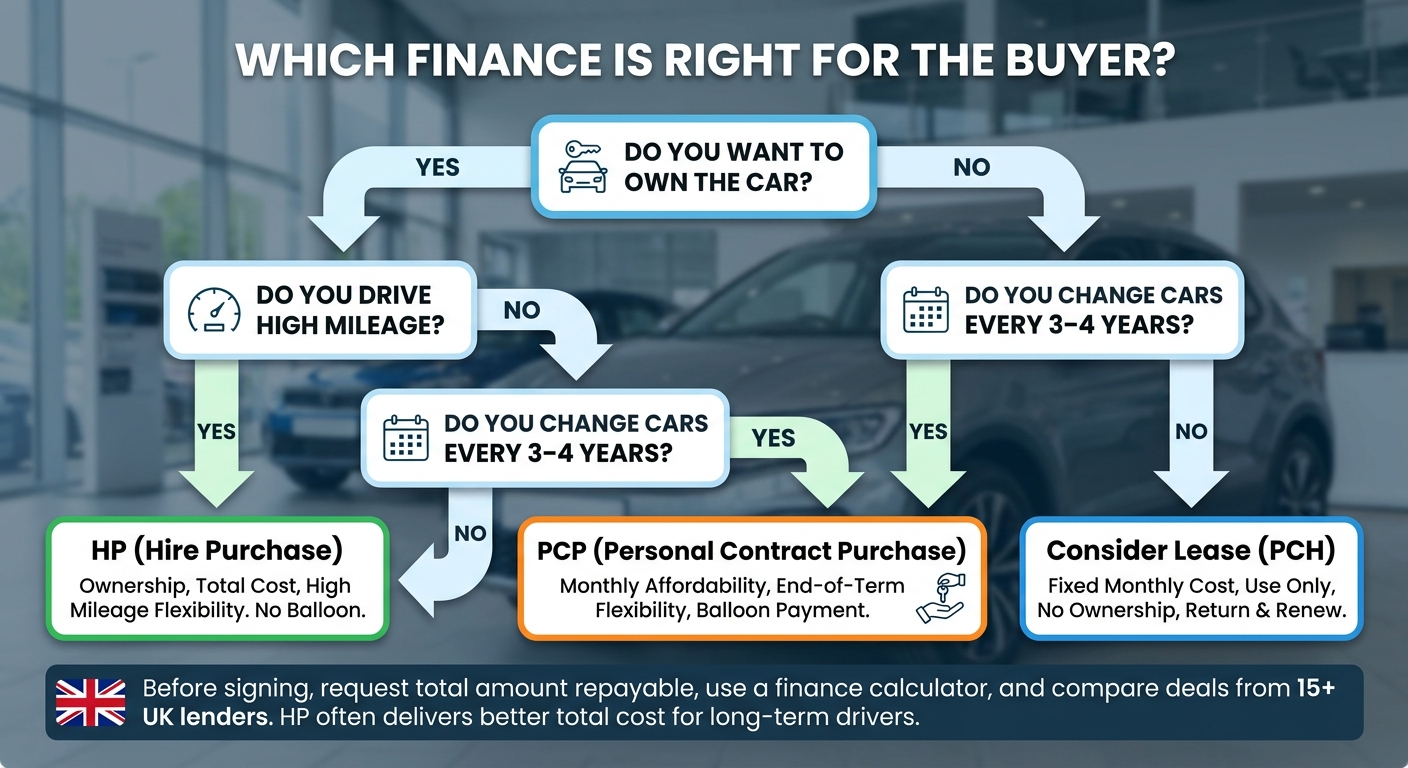

Should Buyers Choose PCP or HP? A Decision Framework

The right product depends on driving habits, ownership goals, budget, and risk tolerance. Use the two lists below to match your priorities to the cheaper structure.

Choose PCP if:

- You change cars every two to four years.

- You want the lowest monthly payment.

- You drive predictable, moderate mileage.

- You can budget for or walk away from the balloon.

- You want manufacturer-backed flexibility.

Choose HP if:

- You want to own your car outright.

- You drive high mileage each year.

- You plan to keep the car five years or more.

- You want no end-of-contract surprises.

- You want to build equity predictably.

Leasing, also called Personal Contract Hire (PCH), suits drivers who never intend to own a car. Many UK drivers now keep a car for six to nine years. For that group, HP often beats a rolling PCP strategy on total cost.

Final Verdict: PCP vs HP, Which Is Right for the Buyer?

HP wins on total cost, ownership clarity, and flexibility for high-mileage or long-term drivers. PCP wins on monthly affordability and end-of-term flexibility for frequent car changers who can manage the balloon. Car leasing (PCH) remains an alternative to PCP for drivers who never intend to own the car. Before signing, request the total amount repayable, not just the monthly figure. Use a car finance calculator, request a full settlement breakdown, or compare deals from 15+ UK lenders. With UK drivers keeping cars for six to nine years, HP often delivers the stronger total-cost outcome.

Frequently asked questions

We've collected the most popular questions about car loans from our customers

Is PCP cheaper than HP?

PCP shows a lower monthly payment than HP, yet it is rarely cheaper overall. Once the balloon payment is added, PCP often costs more to own the same car. On a £28,000 car, HP can save around £1,900 for a driver who keeps the vehicle.

Does PCP mean the buyer owns the car?

PCP does not give ownership during the contract. The finance company holds legal title until the driver pays the balloon payment, the MGFV. Only after paying that lump sum does the PCP driver own the car. Handing the car back instead leaves the driver with no vehicle and no equity.

What happens if mileage is exceeded on PCP?

Exceeding the agreed PCP mileage triggers an excess charge, commonly around 10p per mile and ranging from 3p to 30p. A driver covering 15,000 miles per year on a 10,000-mile limit over three years pays for 15,000 excess miles. At 10p per mile, that adds £1,500 at handback.

Can a buyer exit a PCP or HP agreement early?

Voluntary termination lets a driver end PCP or HP early under Section 99 of the Consumer Credit Act 1974. The driver must have paid 50% of the total amount payable. For PCP, that total includes the balloon payment, so the halfway point arrives later than expected.

Is HP better for high-mileage drivers?

HP suits high-mileage drivers, because it sets no mileage limits. The driver owns the car after the final payment, so extra miles bring no excess charges. PCP instead caps mileage near 8,000 to 12,000 miles per year, with charges of 3p to 30p per excess mile.

What is the difference between PCP, HP and a personal loan?

PCP defers balloon payment and limits mileage. HP spreads the full price and delivers ownership after the final payment. A personal loan gives immediate ownership, because the driver buys the car outright with borrowed cash. The driver repays the lender separately, with no mileage limits or balloon.

Can a buyer change their car before a PCP contract ends?

A PCP driver can change car early, but the finance must be settled first. Positive equity, where the car's value beats the MGFV, can fund a new deposit. Voluntary termination at 50% repayment is another route under the Consumer Credit Act 1974.

Important information

Car-Finance.co.uk is a trading name of Moneyrepublic Ltd (Company No. 12141408). Moneyrepublic Ltd (FRN: 967024) is an Appointed Representative of F&I Online Ltd (FCA No. 731217), which is authorised and regulated by the Financial Conduct Authority. Car-Finance.co.uk acts as a credit broker, not a lender, and may receive a commission. Representative 23.9% APR. Rates from 9.9% APR. Finance is subject to status and affordability. Checking your eligibility uses a soft credit search and does not affect your credit score. A full credit check is carried out by the lender if your application proceeds.

Representative example: Borrowing £7,500 over 48 months at 23.9% APR representative gives a monthly repayment of approximately £234.77 and a total amount payable of approximately £11,269. Rates from 9.9% APR.

Check your eligibility — no impact on your credit score

Leave a request and our experts will contact you shortly to discuss the details.

Author

Roman Danaev is a UK car finance specialist with over a decade in the motor finance industry. He has helped thousands of customers find the right finance deal — from standard HP and PCP agreements to bad credit and no-guarantor options. Roman writes practical, jargon-free guides to help UK drivers make informed borrowing decisions.