How to refinance a car loan in the UK: save money on your PCP or HP deal

Car loan refinancing replaces an existing car finance agreement with a new deal at a lower interest rate. UK drivers on Hire Purchase (HP) or Personal Contract Purchase (PCP) can refinance through a personal loan or a new finance deal. The Bank of England cut the base rate from 4.75% to 3.75% across 2025 and held at 3.75% through April 2026, reducing new lending costs. Borrowers paying 15% to 20% Annual Percentage Rate (APR) on dealer finance can now qualify for 5% to 7% APR with good credit, saving £500 to £2,000 over the remaining term.

What is car refinancing?

Car refinancing replaces an existing car finance agreement with a new loan at a lower interest rate. Two routes exist for UK drivers: an unsecured personal loan, or a new HP or PCP deal with a different lender. Personal Contract Hire (PCH) does not qualify because the customer never owns the vehicle. Realistic savings of £500 to £2,000 are achievable when the new APR is materially lower.

How does car refinancing work?

Car refinancing follows five sequential steps that take two to four weeks. First, you request a written settlement figure from the current lender. Next, check your credit score with Experian, Equifax, or TransUnion. Then compare personal loan and car finance options on total cost. Once approved, the new lender pays off the old agreement. From that point you begin a new repayment plan at the lower interest rate.

The difference between refinancing a PCP vs HP agreement

PCP refinancing involves a balloon payment, also called the Guaranteed Minimum Future Value (GMFV), due at the end of the agreement. HP refinancing involves only the outstanding capital balance, which makes the settlement figure simpler to calculate. PCH (leasing) is ineligible because the customer never owns the car. PCP requires including the balloon in any refinancing calculation. With HP, the settlement quote is straightforward, based on the remaining capital balance alone. For a full product-level comparison, see the HP vs PCP guide.

| Feature | PCP refinancing | HP refinancing |

|---|---|---|

| Balloon payment | Included in settlement | Not applicable |

| Ownership | At balloon, not before | At final payment |

| Settlement complexity | Higher | Lower |

| Best refinancing option | Personal loan or new HP | Personal loan or new HP |

| PCH eligibility | Not eligible | Not eligible |

Should you refinance your car?

Refinancing benefits drivers whose financial profile has improved since the original deal was signed. You will not save money in every case. The decision depends on your current interest rate, your credit score, the remaining term, and whether negative equity complicates the switch.

Will refinancing actually save money? A quick estimation framework

Consider a worked example. An £8,000 balance outstanding at 15% APR over 24 months costs approximately £1,300 in interest. Refinancing the same balance at 7% APR over the same term costs approximately £590 in interest. The gross saving equals £710, minus the early settlement fee and any arrangement fees.

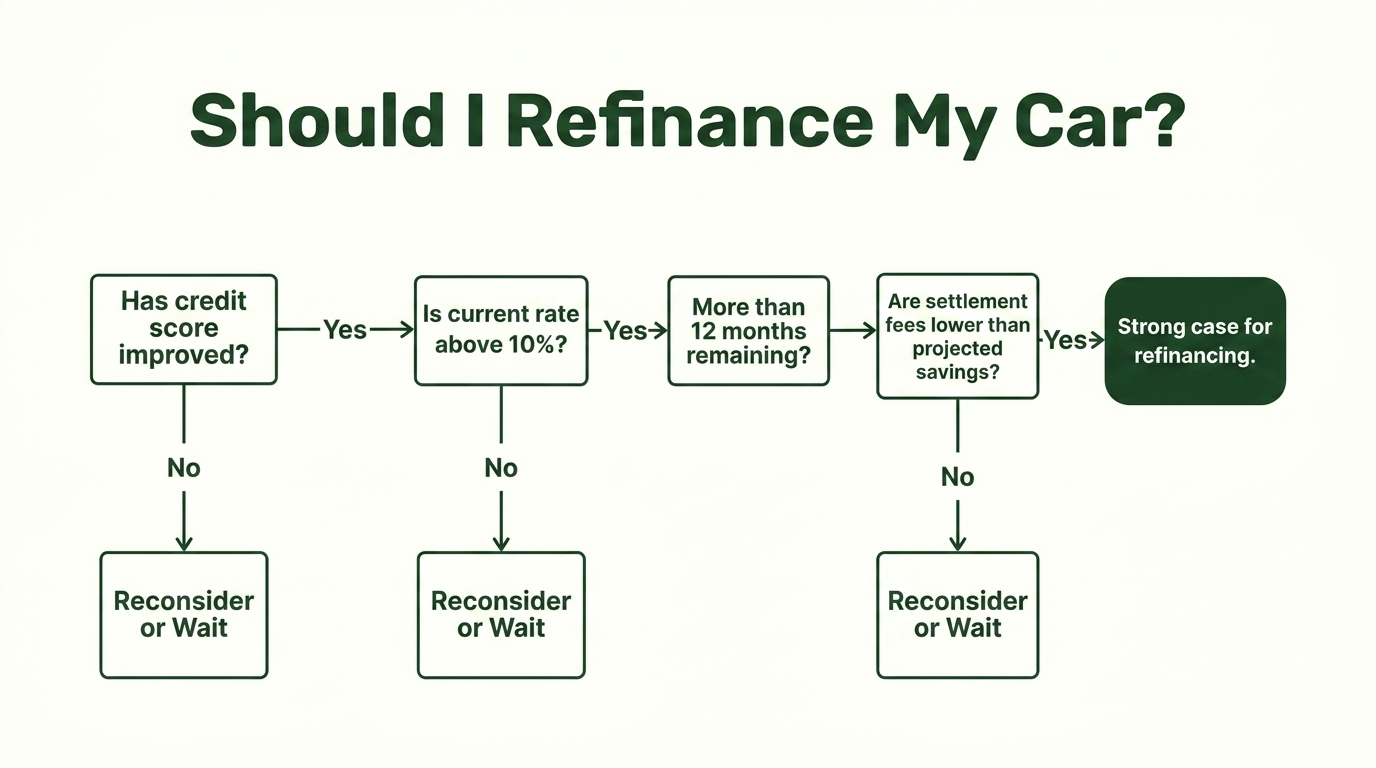

A quick self-check confirms whether refinancing is worth investigating:

- Is your current APR above 10%?

- Do more than 12 months remain on your agreement?

- Has your credit score improved since the original deal?

Two or more "yes" answers mean refinancing is worth investigating.

Signs refinancing makes sense

Five clear indicators point to a productive refinance:

- Your credit score has improved since the original deal was signed

- The current APR exceeds 10% while personal loan rates sit at 5% to 7% APR for good-credit borrowers

- More than 12 months remain on the agreement

- Market rates have dropped (the Bank of England base rate fell from 4.75% to 3.75% across 2025)

- Monthly payments are financially stretched

Drivers paying 15% to 20% APR on a 2023 or 2024 deal can often qualify for 5% to 7% APR today.

When refinancing might cost more

Refinancing increases total cost in several scenarios. Five warning signs indicate the numbers will not work:

- Fewer than 12 months remain on the agreement

- The new rate offers less than a 3-percentage-point improvement

- The new deal extends the loan term, increasing total interest paid

- Your credit score has deteriorated, resulting in a higher APR offer

- Early settlement fees exceed projected interest savings

Compare total cost of credit on the new repayment plan against the existing deal before committing.

How long must a finance agreement be held before refinancing?

No legal minimum exists in the UK. Most lenders prefer six to 12 months of on-time payment history before approving a new repayment plan. Consistent on-time payments raise your credit score with Experian, Equifax, and TransUnion, which in turn determines approval likelihood and the APR offered on the new agreement. If you find the deal unaffordable within weeks of signing, contact the existing lender about hardship options rather than refinance.

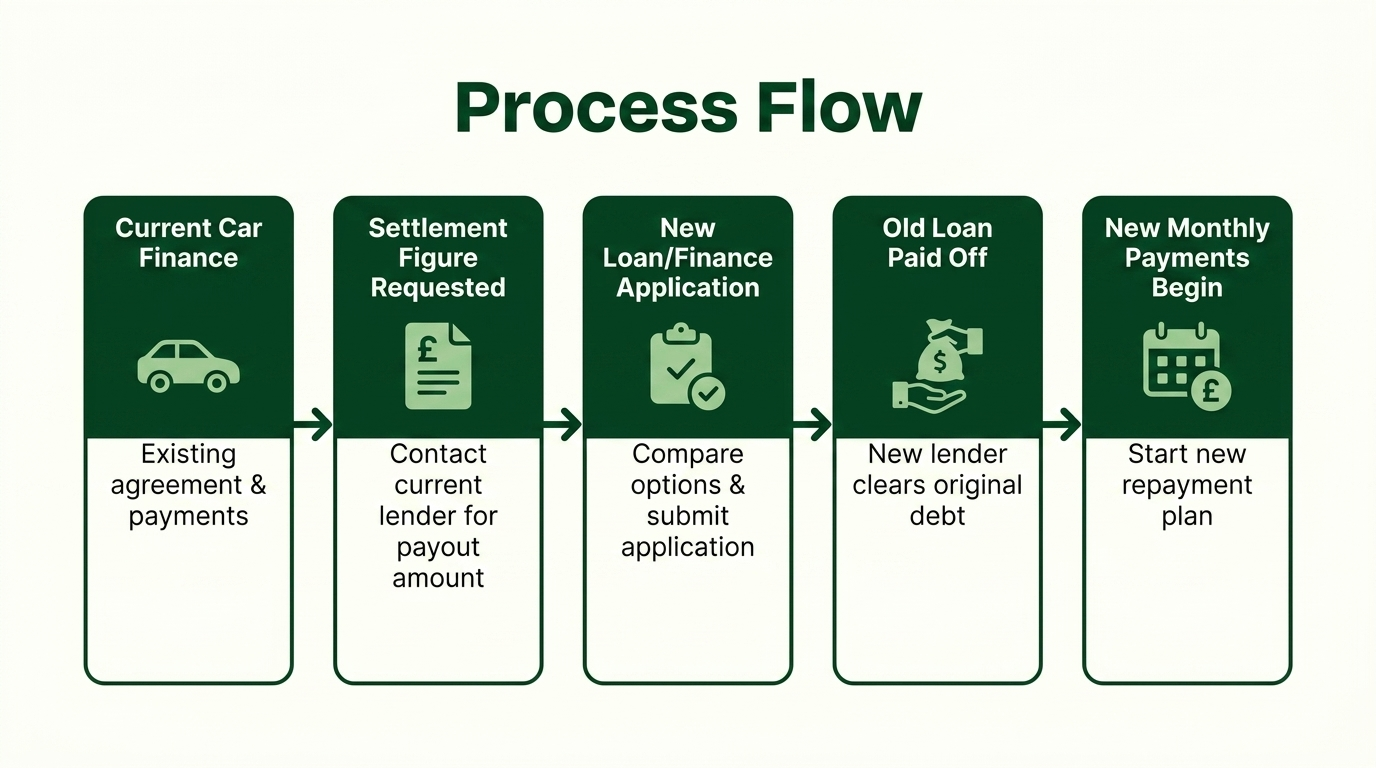

How to refinance a car loan: step-by-step

Car refinancing follows five clear steps once the numbers support a switch. The process takes two to four weeks from settlement quote to first new payment under the new lender.

Step 1: check the current agreement and get a settlement figure

The settlement figure is the exact amount required today to close the existing car finance agreement, not the remaining balance shown on a statement. Contact your current lender and request a formal written quote. Under the Consumer Credit (Early Settlement) Regulations 2004, made under the Consumer Credit Act 1974, the lender may charge a maximum of 58 days' interest on agreements over 12 months (28 days for shorter agreements). On an £8,000 balance at 15% APR, that ceiling works out at approximately £191. Use an early settlement calculator to model the exact cost. Most settlement figures remain valid for 28 days, so your application timeline must allow for the expiry window.

Step 2: check your credit score

Your credit score directly determines the interest rate offered by lenders. Check your score for free through Experian, Equifax, or TransUnion before applying anywhere. Checking your own score is a soft credit search and does not affect your credit file. Review your credit report for errors. For score thresholds by lender, see the guide on what credit score is needed. Correcting incorrect default markers or accounts before applying can result in a materially lower rate offer.

Step 3: compare options: personal loan vs new car finance deal

Two refinancing routes are available, each suited to different credit profiles.

Unsecured personal loan:

- Not secured against the vehicle

- Lower interest rates for good-credit borrowers (5% to 7% APR)

- Available via banks, building societies, and comparison platforms such as MoneySuperMarket

New car finance deal (HP or PCP):

- Secured against the vehicle

- More accessible for lower credit scores

- Available through lenders including Moneybarn, Close Brothers, and Zopa

Use soft-search eligibility checkers on platforms such as MoneySuperMarket before submitting a formal application. Compare like-for-like: same outstanding amount, same remaining term.

Step 4: submit the application and provide required documents

The application process is straightforward once research is complete. Lenders typically request six documents:

- UK driving licence or passport

- V5C logbook for the vehicle

- Proof of income (payslips, bank statements, or tax returns)

- Proof of address dated within three months

- Settlement figure from the current lender

- Current finance agreement details, including original APR and term

Read the full loan agreement before signing. Confirm the total amount repayable and the early settlement terms of the new deal.

Step 5: pay off the old agreement and begin the new one

Specialist car finance lenders typically transfer funds directly to the old lender on the settlement date. With a personal loan, the funds usually arrive in your bank account, so you must transfer the settlement amount before the quote expires.

Cancel the old Direct Debit only after written confirmation that the old agreement is fully closed. Keep the final settlement letter showing a zero balance as protection against administrative errors at either lender.

Can you refinance a car loan with bad credit?

Bad credit makes car finance refinancing more challenging but not impossible. If you have CCJs, IVAs, or missed payments on the existing loan, specialist lenders can still approve an application, although the interest rate offered will be higher than standard. Negative equity, where the car's value has fallen below the outstanding loan balance, can also complicate approval independently of credit history. For a fuller view of options open to lower credit profiles, see the bad credit car finance pillar guide.

What lenders look for when assessing an application

Lenders assess multiple factors beyond credit score alone. Six criteria typically determine the approval decision:

- Credit score and payment history over the past 12 to 24 months

- Debt-to-income ratio (total monthly debt as a percentage of gross income)

- Employment length and income stability

- Electoral roll registration status

- Vehicle age and value relative to the outstanding loan balance

- Equity position (negative equity complicates approval)

Specialist lenders such as Moneybarn (FCA No. 702780) accept lower credit profiles at APRs from 18.5% to 47.5%, with a representative 30.7% APR (Source: Moneybarn.com, accessed 22 May 2026).

How to improve approval chances before applying

Six concrete steps strengthen your application:

- Register on the electoral roll at your current address

- Check your credit file for errors with Experian, Equifax, or TransUnion

- Pay down outstanding debts to lower the debt-to-income ratio

- Use only soft-search eligibility checkers

- Wait three to six months if rate offers are not competitive

- Consider a guarantor loan if your credit score is very low

Six months of active credit improvement can shift a rate offer from 18% APR to 8% APR.

Refinancing a car loan: costs, fees, and risks to know first

Refinancing saves money when the interest rate reduction outweighs the fees and lost protections. Credit score impact, lost Consumer Credit Act rights, and settlement costs can erode savings if not assessed in advance.

Early settlement fees explained

The Consumer Credit (Early Settlement) Regulations 2004, issued under the Consumer Credit Act 1974, cap the early settlement charge on a regulated car finance agreement over 12 months at 58 days' interest on the outstanding balance (28 days for shorter agreements), so you can predict the maximum exit cost on the existing car finance deal before committing to refinance. On an £8,000 outstanding balance at 15% APR, the daily interest rate is around £3.29, so 58 days equals roughly £191. Add the early settlement charge plus any new arrangement fees, then compare the total against projected interest savings over the remaining term. Refinancing only makes sense when total savings exceed total fees by a meaningful margin.

What if the original car finance was mis-sold? (discretionary commission arrangements)

The FCA confirmed a Motor Finance Consumer Redress Scheme on 30 March 2026 in Policy Statement PS26/3. PCP and HP agreements taken out between 6 April 2007 and 1 November 2024 qualify where the lender paid undisclosed commission. Discretionary commission arrangements (DCAs) gave brokers a direct incentive to inflate the interest rate on the loan, so affected drivers paid above-market APRs. The FCA banned DCAs in January 2021.

The FCA estimates the scheme will return £7.5 billion to consumers, averaging £830 per eligible agreement. If your lender has not contacted you, complain directly by 31 August 2027 (Source: FCA press release, 30 March 2026, accessed 22 May 2026). As of May 2026, the scheme faces four legal challenges at the Upper Tribunal (Source: FCA statement, 1 May 2026), which may affect timing or scope. Redress may still reduce the outstanding balance and change the refinancing calculation. For a full walkthrough of the claims process, see the mis-sold car finance guide.

Important: If you took out a PCP or HP agreement between 6 April 2007 and 1 November 2024, you may be eligible for redress under the FCA's Motor Finance Consumer Redress Scheme. Check with the original lender or the Financial Ombudsman Service before refinancing.

FCA mis-selling disclosure: This information is for guidance only. If you believe you have been mis-sold car finance, contact your lender directly or seek independent legal advice. Car-Finance.co.uk is not a claims management company. Claims management firms may charge over 30% of any compensation received.

How refinancing affects your credit score

Refinancing affects your credit score (also called credit rating) in two phases. Short-term: a hard credit search, the closure of the old account, and the opening of a new account typically reduce the score by 5 to 15 points, with recovery in three to six months. Long-term: consistent on-time payments improve the credit rating over time. Monitor changes through Experian, Equifax, or TransUnion. If you plan a mortgage application within six months, delay refinancing to protect the mortgage assessment.

Losing Consumer Credit Act protections: what this means

Two key Consumer Credit Act protections apply to HP and some PCP agreements. The one-third rule prevents repossession without a court order once one-third of the total HP price has been paid. Voluntary termination under Section 99 allows you to return the car after paying 50% of the total amount payable.

Refinancing resets both thresholds to zero on the new agreement. Unsecured personal loans carry neither protection because they are not secured against the vehicle. You trade statutory protection for a lower interest rate.

What happens if payments are missed on a refinanced car loan?

Missed payments carry different consequences by agreement type. New secured car finance (HP or PCP): the lender holds security over the vehicle and can pursue repossession. The one-third rule applies only to the new balance, which starts from zero.

Unsecured personal loan: the lender has no direct claim on the car. Non-payment leads to default notices, potential County Court Judgements, and damage to your credit score and credit rating that remains on your credit file for six years. Contact your lender immediately if payments are at risk, because lenders typically prefer restructuring to legal action.

Can you refinance a balloon payment?

A balloon payment is the Guaranteed Minimum Future Value (GMFV) due at the end of a PCP agreement, per FCA motor finance guidance. PCP drivers can refinance the balloon through an unsecured personal loan or a new HP agreement. Interest rates on personal loans for prime borrowers currently sit at 5% to 7% APR, while new HP rates typically start from 9.9% APR depending on lender and vehicle age. If the car's value exceeds the balloon, selling privately can deliver a higher return than the dealer's part-exchange offer. Start exploring options three to four months before the balloon falls due to allow time for comparison.

Can a car be refinanced with the same lender?

Same-lender refinancing is possible but rarely delivers the most competitive interest rate. Lenders reserve the lowest rates for new customers and the strongest credit profiles. Obtain quotes from at least two external lenders first, then approach the current provider for a rate match. A competitive external offer provides bargaining power in the negotiation. The one scenario where same-lender refinancing can be advantageous is a long, clean payment history. A consistent 12-to-24-month track record raises your credit score and supports a loyalty rate request.

Alternatives to refinancing a car loan

Three alternatives exist when car finance refinancing is not the right move.

Pay off the balance with savings. If the loan APR exceeds your savings rate, clearing the balance saves more than the savings earn. Keep a three-month emergency fund first.

Trade in the car. Trade-in works when positive equity exists (the car's value exceeds the loan balance). Negative equity complicates trade-in. Selling privately often delivers more than the dealer's part-exchange figure.

Exercise voluntary termination. Section 99 of the Consumer Credit Act applies to HP and some PCP agreements. If you have paid 50% of the total payable, you can return the car with nothing further owed.

Conclusion: is refinancing a car loan worth it?

Car finance refinancing saves £500 to £2,000 when conditions align. The pre-application checklist has five steps:

- Get a written settlement figure

- Check your credit score with Experian, Equifax, or TransUnion

- Compare personal loan and car finance options on total cost

- Use soft-search eligibility tools to test approval odds

- Calculate total cost of credit on both options

Check eligibility with Car-Finance.co.uk in 2 minutes. The initial check is a soft credit search and does not affect your credit score. A full credit search will be carried out by the lender if you proceed to a formal application.

Representative example: Representative 23.9% APR. Borrowing £8,000 over 48 months with a representative APR of 23.9% (fixed) and a deposit of £0, the monthly repayment is £250.50. Total amount repayable: £12,024.00. Total cost of credit: £4,024.00.

Regulatory disclosure: Car-Finance.co.uk is a trading name of Moneyrepublic Ltd (Company No. 12141408, FRN 967024). Moneyrepublic Ltd is an Appointed Representative of F&I Online Ltd (FCA No. 731217), which is authorised and regulated by the Financial Conduct Authority. Car-Finance.co.uk is a credit broker, not a lender. We receive a commission from lenders when we arrange finance on your behalf. This does not affect the rate you are offered. Learn more about how we make money. Checking your eligibility uses a soft credit search and does not affect your credit score. A full credit search will be carried out by the lender if you proceed to a formal application.

Frequently asked questions

We've collected the most popular questions about car loans from our customers

What is car refinancing and how does it work?

Car refinancing replaces an HP or PCP agreement with a new deal at a lower interest rate. The new lender pays off the outstanding balance, and a new repayment plan begins. Savings of £500 to £2,000 are typical when the APR drops by three or more percentage points.

Is it a good idea to refinance a car loan?

Refinancing makes sense when the current APR exceeds 10%, the credit score has improved, and more than 12 months remain on the agreement. A driver moving from 15% APR to 7% APR on £8,000 over 24 months saves approximately £710 before fees. Refinancing does not save money when early settlement fees exceed projected savings.

How does car refinancing work step by step?

Five steps complete a car refinance: a settlement figure is requested from the current lender; the credit score is checked with Experian, Equifax, or TransUnion; loan options are compared on total cost; the application is submitted with documents; and the old agreement is paid off.

Can a PCP or HP car finance agreement be refinanced?

HP agreements can be refinanced through a personal loan or a new car finance deal. PCP agreements can also be refinanced, including the balloon payment at the end of the term, though the calculation is more complex. PCH (leasing) cannot be refinanced because the customer never owns the vehicle.

What are the main benefits and disadvantages of refinancing a car loan?

Refinancing reduces monthly payments and lowers total interest when the new APR is materially lower. Disadvantages include early settlement fees (capped at 58 days' interest), a temporary credit score drop of 5 to 15 points, and the reset of one-third rule and voluntary termination rights on a new HP deal.

Check your eligibility — no impact on your credit score

Leave a request and our experts will contact you shortly to discuss the details.

Author

Roman Danaev is a UK car finance specialist with over a decade in the motor finance industry. He has helped thousands of customers find the right finance deal — from standard HP and PCP agreements to bad credit and no-guarantor options. Roman writes practical, jargon-free guides to help UK drivers make informed borrowing decisions.